Europe: Less widespread but still meaningful labour shortages

-

The momentum of private payroll employment has recently slowed in the euro area, as evidenced by job destruction in France and Germany in Q3.

-

This destruction can be partly explained by cyclical sectors, particularly construction. It is a sign that demand constraints are increasingly impacting companies and the labour market.

-

However, labour shortages remain high in the northern countries of the euro area and in Central Europe and, in general, in sectors where demand is not falling (aeronautics and building renovation in particular).

-

Beyond an economic slowdown, which we expect to last until spring 2024, impacting employment, the low level of unemployment and historically high labour shortages should continue to characterise the European economy.

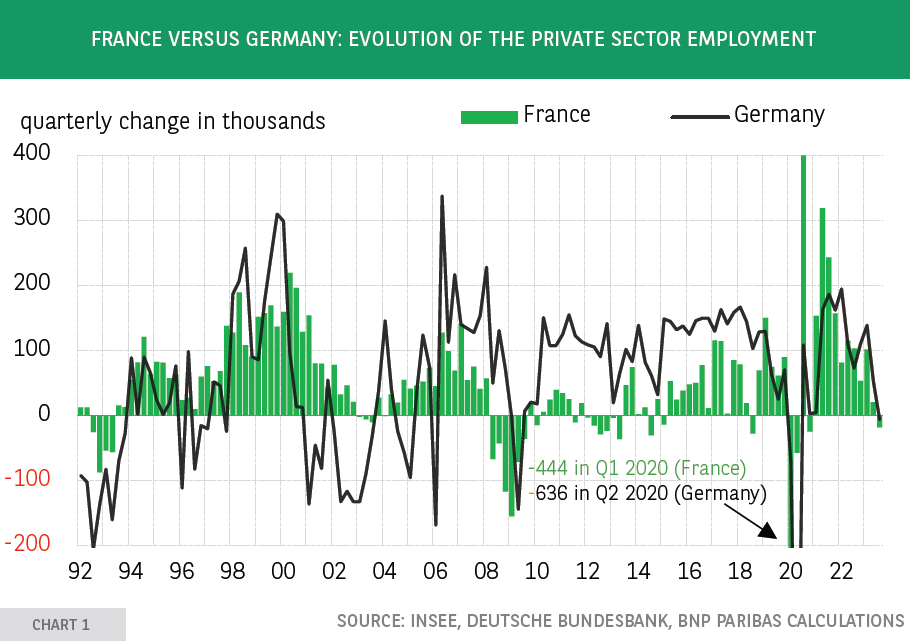

Employment contracted in France and Germany in Q3 2023 (by 18,000 and 6,000, respectively); this simultaneous decline is unprecedented (excluding the Covid period) since H1 2009 (Chart 1). This follows a period of sustained job creation in these two countries and, more broadly, in the euro area, where employment quickly wiped out the effects of Covid, momentum which has only slowed very recently (from Q2 2023 onwards).

This evolution could indicate a risk of recession, as recession is usually accompanied by a contraction in employment. In France, the most cyclical sectors are cutting jobs, such as temporary employment services or the construction industry. Industry, on the other hand, continues to benefit from job creation. In addition, there is probably a substitution effect between self-employment (still growing in Q3, much more than in 2009 notably) and certain forms of payroll employment (particularly temporary work), in favour of the increasing formalisation of self-employment (umbrella companies, a system which allows a self-employed person to obtain the social welfare advantages of employee status) And lastly, a potential decline in apprenticeships may have begun, now contributing negatively to employment trends.

The causes of this contraction of employment may have different consequences: beyond its perceived change in nature (substitution effect), is employment contracting due to the deterioration of the economy or because the drop in unemployment, until Q2 2023, makes it difficult to recruit qualified personal in businesses under pressure? Probably a bit of both. In other words, are the euro area and its two largest economies (Germany and France) running the risk of seeing their activity slow down even more due to weak economic demand, or because supply is structurally hindered by the constraints it is experiencing (labour shortage due to ageing of the population, matching issues as skills required to support the climate and digital transitions differ from available skills)?

Historic labour shortages

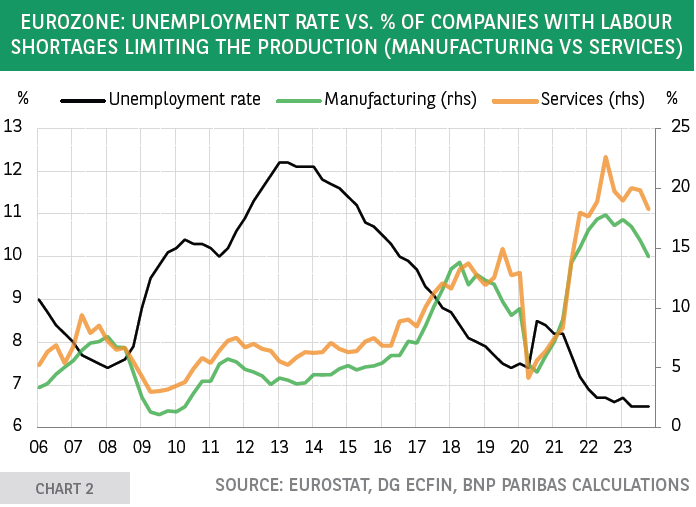

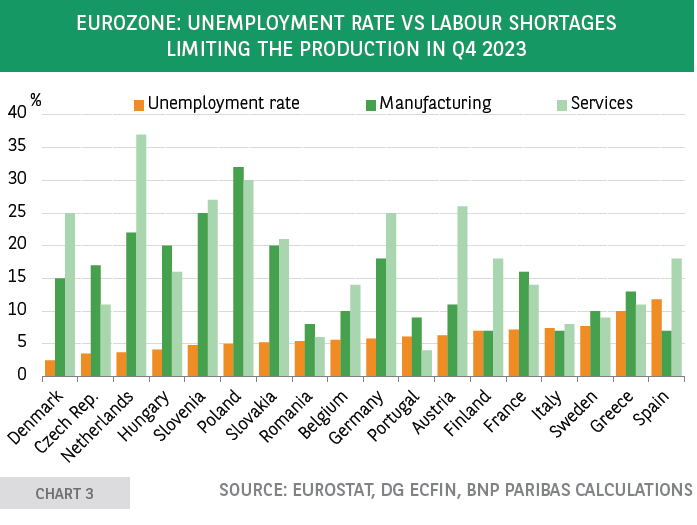

Several countries are suffering from labour shortages, such that companies stated in the European Commission survey that these shortages are limiting their production to a relatively unprecedented extent, while the economic situation is deteriorating. The last major global recession that penalised employment dates back to 2009, as mechanisms (furlough in particular) were put in place during the Covid-19 pandemic to protect jobs. The structural drop in unemployment in the euro area after 2009 has continued, until reaching 6.5% in September 2023 (Chart 2), a record low since the creation of the Monetary Union. An overview by country shows that the labour shortage is not uniform and that divergences generally go hand-in-hand with differences in unemployment rates: the lower the unemployment rate, the more labour shortages are identified as restrictive. As a result, Northern Europe (Denmark, the Netherlands, Germany) and Central Europe appear as the most affected regions (Chart 3).

Persistence or even worsen sectors where demand is not falling

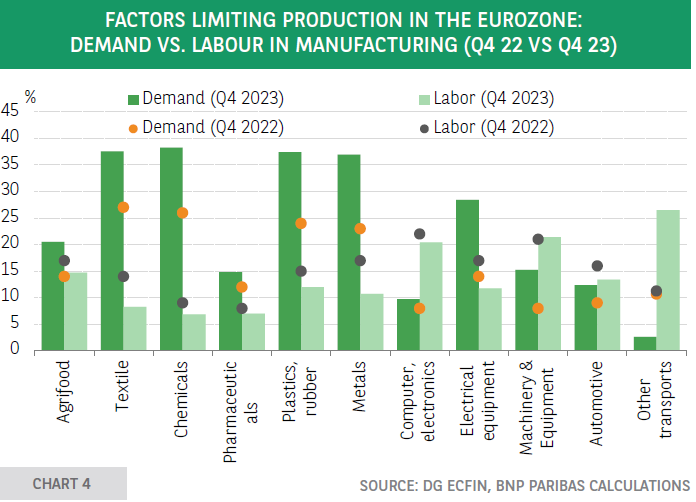

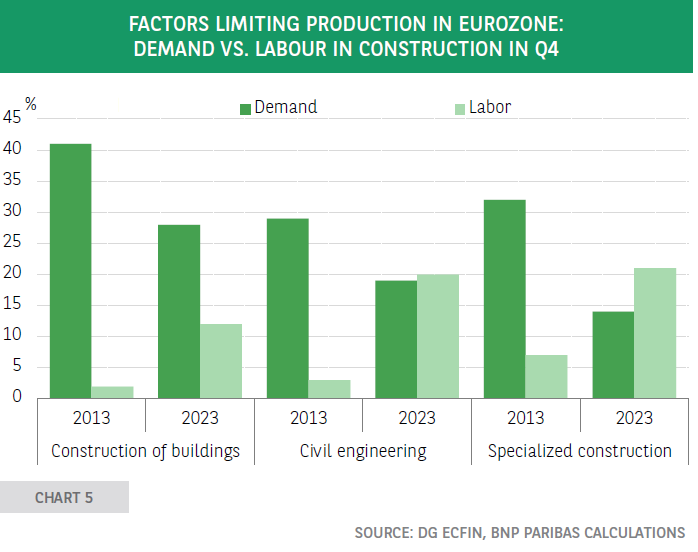

Following the pandemic, the European economy suffered from significant supply constraints. However, demand was affected by two successive shocks: inflation and then rising interest rates. The increase in demand as a factor limiting production has therefore reduced the role of labour shortages, particularly in new construction or in the agrifood sector, two sectors that have suffered a drop in household demand (Charts 4 & 5).

After the Covid-19 crisis, intermediate goods (chemicals, metallurgy, plastics, wood/paper) were both subjects and vectors of supply difficulties (lack of components, containers or packaging). Inherently, the downturn in the latter and the sharp increase in demand constraints have pushed the labour shortages in these sectors into the background.

In services, there is a reduction in the impact of labour shortages, which had limited the production of 23% of companies a year ago and which only restricted production for 18% of them in Q4 2023, i.e. the same proportion that is now experiencing demand constraints. Shortages remain particularly detrimental in the sectors most affected by a ramping up – and therefore by a lack of demand problems – and/ or by a transformation of activity that requires attracting new skills.

In particular, aeronautics (included in the “other transport” category, Chart 4) and specialised construction (including building renovation) are in this situation (Chart 5, where 2013 is taken as a benchmark period with a crisis on the real estate market).

In aeronautics, it can even be seen that labour problems are increasing while supply shortages have slowed. This shortage of staff is considered a factor limiting production for 26% of companies on average in H2 2023, compared to 11% on average in 2022. These issues constitute a sword of Damocles capable of counteracting the ramping up in production.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.