Euro could rally despite expected 25bp ECB cut tomorrow

Looking beyond the horizon

The first ECB interest rate cut of the cycle is nearly certain to take place this Thursday. With the move widely telegraphed and expected, market attention will focus elsewhere as investors try to assess the Governing Council's next steps.

At the last ECB meeting in April, President Lagarde reiterated that a data-dependent Governing Council will know ‘a lot more’ by June. Investors and indeed ourselves read it as a very clear confirmation that the bank intends to cut rates at this month’s meeting. If there was any doubt about it, ECB chief economist Philip Lane stated in his interview with the FT published last week that ‘barring major surprises, at this point in time there is enough in what we see to remove the top level of restriction’. Sounds like a done deal to us.

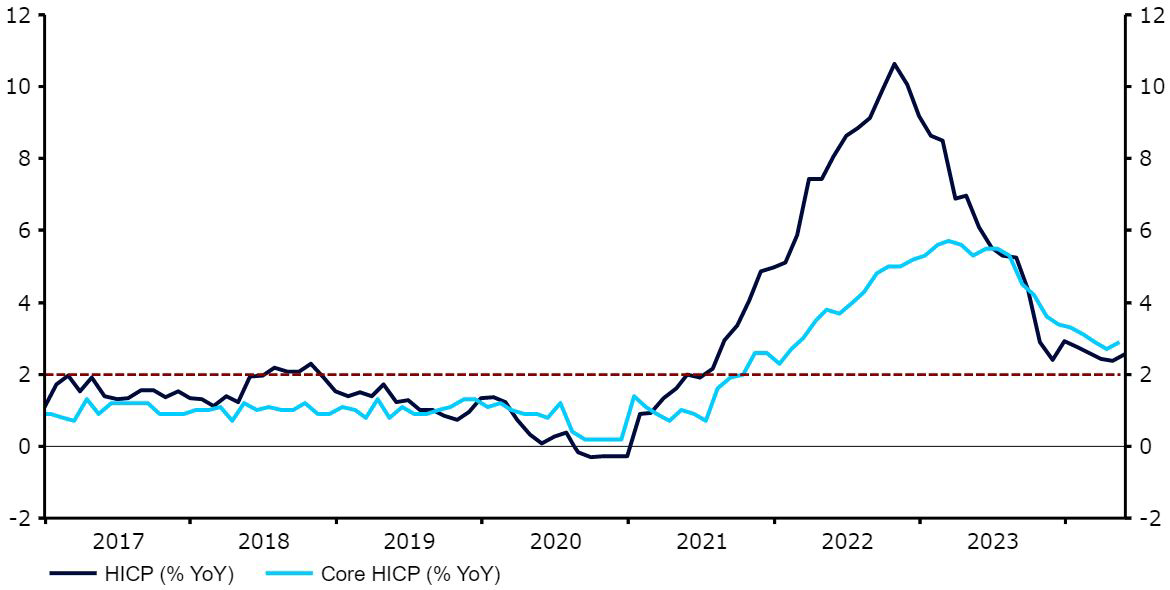

The turn towards rate cuts is not surprising considering the significant inflation progress in the Eurozone. The headline measure of price growth eased from a record high of 10.6% in October 2022 to 2.6% in May 2024. The core measure, which better reflects domestic price pressures, also fell from its highs, printing at 2.9% in May. In the face of the above, the removal of some policy restriction seems justified.

With a June rate cut nearly fully priced in by markets, the move itself will unlikely have a significant impact on asset prices. Volatility on Thursday afternoon is, however, likely to be elevated as investors will adjust their expectations regarding the future timetable of cuts based on cues from the meeting.

Euro area inflation rate [2017 - 2024]

Source: LSEG Datastream Date: 03/06/2024

With swap markets now seeing a second cut in July as relatively unlikely (≈10% priced-in), any hint of back to back moves, or that markets might be underestimating the extent of cuts, in general, would likely cause a sell-off in the common currency. Conversely, a less dovish set of communications that both flags disquiet over inflation, while hinting at no immediate rush to ease policy again, could aid the euro.

While a vague suggestion that a further removal of restriction is likely in the future would not be surprising, we think that the bank is unlikely to provide clear forward guidance regarding the timing of future cuts. Instead, President Lagarde may reiterate that the Governing Council will adopt a data-dependent approach and will make decisions on a meeting by meeting basis.

Aside from her rhetoric on monetary policy, comments about the labour market, economic and inflation outlook and the updated macroeconomic projections will be closely watched. We are probably unlikely to see major changes to the latter this time around, although modest revisions, notably an upward one to this year’s growth forecast, could take place.

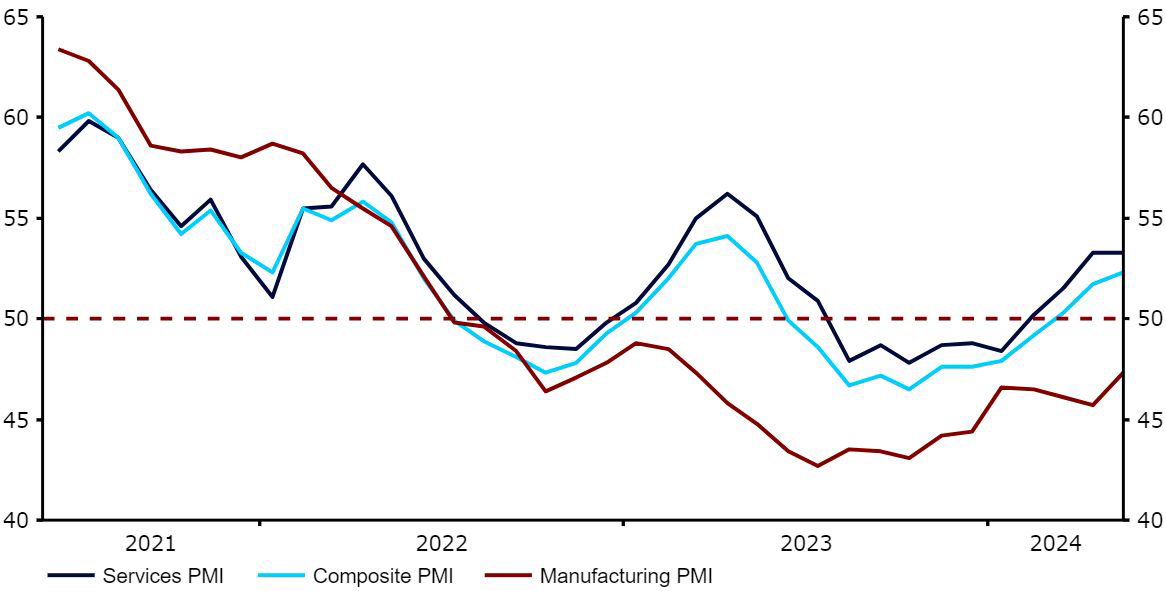

The question about what comes next is not a trivial one. On the one hand, inflation has progressed in the right direction, the economy remains weak, and some forward-looking data suggest wage growth should ease with time. On the other, the labour market is tight: unemployment recently fell to a record low and negotiated wages rose by 4.69% in Q1, just below their fastest pace on record. This will no doubt accentuate inflation concerns. HICP inflation recently surprised to the upside, notably the services inflation measure, which rose to 4.1% in May, its highest level in eight months. In addition, economic activity is picking up. GDP growth turned positive in Q1, with the economy expanding by a stronger-than-expected 0.3%. The forward-looking PMI data is also trending higher, and has largely surprised to the upside, with the composite index rising to 52.3 in May, pointing to a relatively strong growth momentum, driven by services.

Euro Area PMIs [2021 - 2024]

Source: LSEG Datastream Date: 03/06/2024

At the same time, the external environment has been supportive of a more hawkish stance. Federal Reserve cuts are uncertain and highly unlikely before at least September, and even then, the pace of US policy easing will probably be slow. There are also some concerns that the inflation pattern seen in the US may not be as idiosyncratic as previously thought.

In recent weeks, Governing Council members have been generally more dovish than their counterparts on the other side of the Atlantic. We believe that this is likely to remain the case in the near future, and think that the market might actually be slightly underpricing rate cuts in the Euro Area this year. Our base scenario is for three ECB cuts in 2024, most likely in June, September and December, while the market is only pricing in slightly more than two. Considering the above, we think that risks to the euro coming into this week’s meeting might be skewed slightly to the downside.

Author

Matthew Ryan, CFA

Ebury

Matthew is Global Head of Market Strategy at FX specialist Ebury, where he has been part of the strategy team since 2014. He provides fundamental FX analysis for a wide range of G10 and emerging market currencies.