- Central banks' focus remains on inflation, but growth is meant to lead the way.

- The upcoming US Donald Trump presidency will have widespread effects abroad.

- The EUR/USD pair is on its way to test parity in the first half of 2025.

The EUR/USD pair started the year changing hands at around 1.1040 and ended near its yearly low of 1.0332. By September, the pair surged to 1.1213 and the Euro (EUR) seemed on its way to conquer the world.

The financial world revolved around inflation levels and hopes central banks would drop their monetary tightening policies throughout the first half of the year. As the year comes to an end, it's clear that such hopes were far from being fulfilled.

Expectations of central banks engaging in massive easing amid inflationary pressures falling within central banks’ goals diluted. Employment and growth became more worrisome as time went by and, at some point, overshadowed inflation-related concerns.

It is worth noting that central banks’ goals revolve around inflation and employment. Policymakers’ mandate has nothing to do with economic progress, although their policies may affect it. And that’s what happened in 2024.

The European Central Bank moved on the wrong reasons

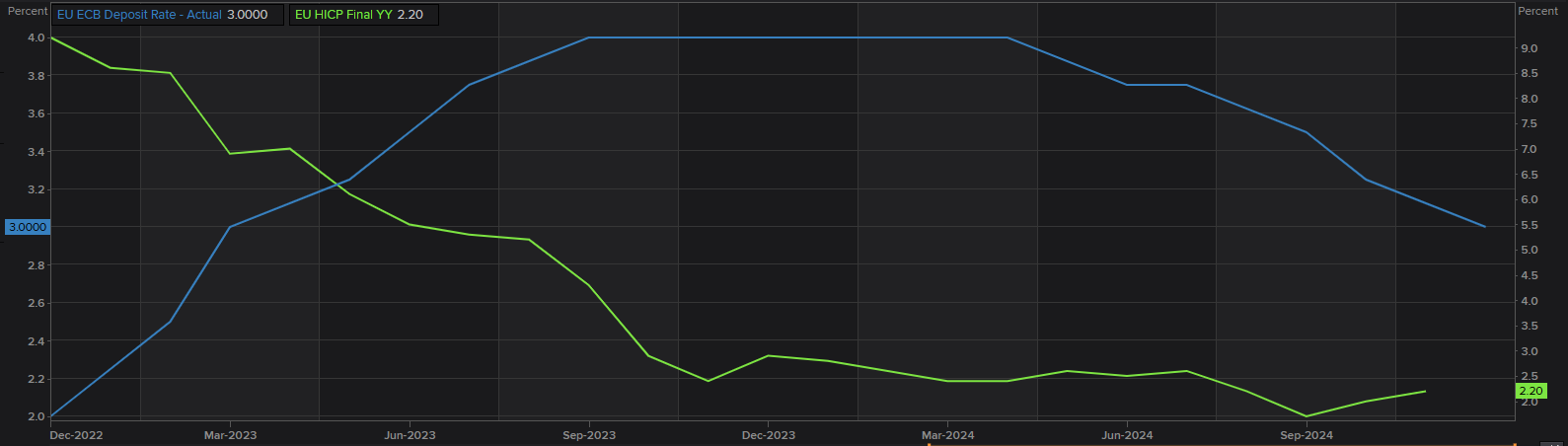

The European Central Bank (ECB) was among the first central banks to shift its monetary policy. Following a long year of a tighter monetary policy, the ECB announced in June the first interest rates trim, reducing its three benchmark rates by 25 basis points (bps) each. The central bank delivered its fourth interest rate cut in December, meaning the interest rate on the main refinancing operations, the interest rates on the marginal lending facility and the deposit facility now stand at 3.15%, 3.4% and 3%, respectively.

But what sent the ECB into kick-starting monetary loosening was not inflation but fears of an economic setback. Of course, officials initially refrained from saying it out loud but ended up acknowledging it partially in the final quarter of the year.

Indeed, inflationary pressures have receded from their 2022 record peaks. The Harmonized Index of Consumer Prices (HICP) was down to 1.7% Year-on-Year (YoY) in September 2024, far below the 10.6% posted two years earlier. The HICP ticked higher in the following two months, reaching 2.2% in November.

Growth, however, has remained sluggish throughout the year and different macroeconomic indicators suggest that a recession is not out of the picture. On an annual basis, seasonally adjusted Gross Domestic Product (GDP) rose by 0.9% in both the euro area and the European Union (EU) in the third quarter of 2024, according to Eurostat, helped by a 0.4% unexpected advance in the three months to September. The figures fell short of spooking concerns about economic progress.

More relevantly, the Purchasing Managers Index (PMIs), which measures levels of manufacturing and services output throughout the EU, showed that the manufacturing sector spent roughly a second consecutive year in contraction territory, only saved by solid performance in the services sector. The December Composite PMI for the EU printed at 49.5, far below the 2021 peak of 60.2.

Weak consumption will likely extend into 2025, forcing the ECB to maintain its loose monetary policy even if inflation remains above the central bank’s goal.

Not only did ECB policies affect European growth, but political woes also added to the doom picture amid failed governments in France and Germany, the two leading EU economies.

The German coalition government collapsed after the Bundestag delivered a non-confidence vote on Chancellor Olaf Scholz. As a result, a snap election will take place in February.

Meanwhile, the French cabinet was forced to resign en masse after the National Assembly passed a no-confidence motion against the Cabinet of Prime Minister Michel Barnier.

More worrisome is resurgent extreme parties, with far-right forces that oppose European Union integration and leftists who call for increasing public support.

ECB Deposit Rate vs. HICP evolution.

Is the US Dollar rally over or just beginning?

Across the Atlantic, things developed quite differently, yet the US Dollar (USD) stands as the yearly winner. The Dollar Index (DXY) rally reached its climax on December 20, hitting its highest in over two years. The Dollar Index peaked at 108.55, sharply up for a third consecutive month.

President-elect Donald Trump was the main catalyst, but not the only one. The USD started its unstoppable run by the end of September, fueled by concerns about the potential outcome of the presidential election in the United States (US). Market players were concerned that a Trump victory would imply a drastic shift in foreign and fiscal policies.

Trump not only won the presidency, but the Republican party seized control of the Senate and the House. Unified control of the elected branches of government reinforces the upcoming president’s power.

Why are markets concerned about Trump’s policies?

Generally speaking, a Republican victory is seen as positive for financial markets. Wall Street rallied, with the three major indexes hitting record levels amid Trump’s pledge to cut taxes and impose tariffs on foreign goods and services. The US Dollar tends to appreciate alongside local equities, while government bonds tend to ease.

Euphoria is only being overshadowed by the increased upward risks to inflation related to Trump’s policies. Low unemployment levels, or rather high employment levels, could be seen as increased consumer demand, which can lead to higher prices.

Usually, moderated price pressures within a Republican government are not a concern, but it is all about the timing: Trump will take office a few months after the Federal Reserve (Fed) quick-started an easing monetary policy, following a tightening cycle that pushed interest rates to multi-decade highs to fight inflation.

Investors have felt the pain of skyrocketing inflation. Tariffs, if implemented, could mean higher prices for Americans in a wide spectrum of goods and services. Worth adding that his tariffs policy could also spread into other major economies. In fact, European policymakers have expressed their concerns about potential negative effects on local inflation.

Where is the Fed standing?

The US Federal Reserve (Fed) trimmed rates three times this year, delivering 50 basis points (bps) cut interest rate in September, a 25 bps cut in November, and another 25 bps in December to a target range of 4.25%-4.50%.

Fed officials have maintained the focus on inflation for most of 2024, just temporarily shifting it to employment. Growth concerns were also there but to a lesser extent than in Europe.

US inflation returned to the limelight in the final Fed meeting of the year as policymakers noted the decision to trim the benchmark interest rate was a “close call” and signalled a slower pace of rate cuts coming in 2025, as inflation holds steadily above the Fed’s goal and economic growth is fairly solid.

Officials indicated that it probably would only lower rates twice in 2025, according to the Summary of Economic Projections (SEP) or dot plot. The two cuts mean half the committee’s intentions from the previous SEP released in September.

The US Consumer Price Index (CPI) rose by 2.7% on a yearly basis in November from 2.6% in October, according to the US Bureau of Labor Statistics (BLS), while the core CPI, which excludes volatile food and energy prices, rose 3.3% in the same period, both matching the market’s expectations.

Fed Funds target rate vs CPI evolution

Concerns about a US recession eased as time went by, with the odds for a soft landing diluting by the end of the year. The economy has been in pretty good shape throughout 2024 and the latest Gross Domestic Product (GDP) release confirmed so. The economy expanded at an annual rate of 3.1% in the third quarter of the year, although there are some weak spots.

Optimism about skipping a recession and additional rate cuts pushed Wall Street to record highs, although the latest dot-plot forced speculative interest into profit-taking. Still, the three US major indexes reached unexplored territory and held nearby as the year ended.

EUR/USD in 2025: US, Eurozone economic divergence set to widen

Beyond the foretasted two rate cuts for 2025, the Fed upgraded its GDP growth forecast for 2024 to 2.5%, compared to the 2% projected in September, citing resilient economic activity. However, growth is expected to return to its long-term trend of 1.8% from 2026 onward.

Additionally, inflation estimates were revised upwards, with the 2025 forecast now at 2.5%, up from 2.1%, and core inflation projected at 2.8% for the same year.

Across the pond, the ECB is expected to cut rates further in 2025 amid persistent weak growth and cooling inflation. Market analysts started considering that rates could drop below the 2% neutral level, although that’s an unlikely scenario.

The ECB’s latest macroeconomic projections offered downward adjustments to inflation forecasts, with headline inflation expected to reach 2.1% and core inflation 2.3% before both align at 1.9% by 2026. Growth forecasts have also been revised lower, with 2025 now projected at 1.1% and 2026 at 1.4%.

Bottom line, the Fed faces upward risks on the inflationary front, while the ECB will have to deal with the economic setback, which, spiced with local political turmoil, stands as a major challenge.

EUR/USD technical outlook: Heading towards parity?

The EUR/USD pair is ending a third consecutive month in the red and technical readings in the monthly chart suggest 2025 will be a tough year for the Euro. The pair has spent most of the last two years trading above its 20 Simple Moving Average (SMA) before collapsing below it in the last November. The 100 SMA, in the meantime, has provided strong dynamic resistance, rejecting buyers in the 1.1200 area throughout the same period. Even further, technical indicators have pierced their midlines and maintain firmly bearish slopes, supporting lower lows ahead. Beyond the 1.0330 price zone, there is little in the way towards the 1.0200 threshold, while below the latter, a test of parity is on the table.

On a weekly basis, technical readings suggest the EUR/USD pair will likely post lower lows before being able to correct higher. Technical indicators head firmly south and near oversold territory, albeit without any sign of downward exhaustion. The same chart shows the 20 SMA is gaining downward momentum and about to cross below a flat 100 SMA, both far above the current level, usually a sign of prevalent selling interest.

The bearish case is the most likely but not the only one. Should the pair change course amid an EU comeback and sudden weakness in the US economy, the pair could initially target the 1.0600 price zone. A continued macroeconomic imbalance in favor of the EU could result in the EUR/USD pair reaching the 1.1000 threshold, albeit not within the first half of the year.

Conclusion

The macroeconomic picture favors the USD over the EUR, as with even inflationary pressures, the focus will be on economic developments. Trump’s upcoming presidency may imply higher inflation-related risks for the US, but even with the coronavirus in the middle, the US economy had the strongest pandemic recovery within the G7 as measured by GDP, starting with the previous Trump presidency and following under Biden’s administration.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

AUD/USD: Extra consolidation appears on the cards

AUD/USD set aside a two-day recovery past the 0.6300 hurdle and came under pressure on Wednesday, always in response to US tariff fears and the marked bounce in the Greenback.

EUR/USD: Further downside could retest the 200-day SMA

EUR/USD accelerated its losses and retested lows near the 1.0740 zone on the back of the stronger US Dollar and persistent jitters surrounding potential tariffs on EU imports as soon as next week.

Gold remains slightly offered just above $3,000

Gold price struggles to gain traction as USD recovers despite firm support above $3,000 and cautious Fed tone. The US Dollar rebounds following reports of Trump auto tariff announcement. Solid Durable Goods data, Fed comments on sticky inflation limit upside for Bullion bulls.

Ethereum sees a downtick despite successful Pectra launch on Hoodi testnet

Ethereum is down 3% on Wednesday despite positive updates of the Pectra upgrade successfully going live on the Hoodi testnet. The top altcoin could sharply decline if it validates a bearish flag pattern by falling below $1,818.

Sticky UK services inflation shows signs of tax hike impact

There are tentative signs that the forthcoming rise in employer National Insurance is having an impact on service sector inflation, which came in a tad higher than expected in February. It should still fall back in the second quarter, though, keeping the Bank of England on track for three further rate cuts this year.

The Best brokers to trade EUR/USD

SPONSORED Discover the top brokers for trading EUR/USD in 2025. Our list features brokers with competitive spreads, fast execution, and powerful platforms. Whether you're a beginner or an expert, find the right partner to navigate the dynamic Forex market.