Major US stock market indexes rallied last Wednesday as the results of the US presidential elections showed a possible clear win of Donald Trump. Even the Fed’s slightly more hawkish interest rate decision did not reverse the upward direction of major US stock market indexes on Thursday. Today we are to have a closer look at the Fed’s interest rate decision, discuss the release of the US CPI Rates for October later today and have a look also on the upcoming earnings reports of NVIDIA and Walmart’s, and yesterday’s Home Depot, linking it with the release of Octobers’ US retail sales growth rate on Friday. For a rounder view we are to conclude the report with a technical analysis of S&P 500’s daily chart.

The Fed’s 25 basis points rate cut

Last Thursday, the Fed cut rates as expected by 25 basis points, yet may have been more hawkish than expected in its forward guidance. In its accompanying statement, the bank removed the line stating that "the Committee has gained greater confidence that inflation is moving sustainably toward 2 percent“. The removal may be interpreted as a signal that we may see renewed inflationary pressures, causing the bank to slow down its rate-cutting path. Yet Fed Chairman Powell seemed to dismiss such an assumption in his press conference. Furthermore, we highlight that the bank seems determined to defend its independence from the newly elected US President, as the Fed Chairman clearly stated that he would not resign if asked for by Donald Trump. Overall we note that he despite the market expectations for the Fed to proceed with another rate cut in the December meeting easing, they are still predominant and may provide support on US stock markets on a monetary level. Yet on Friday Fed Chairman Powell is expected to speak, while other Fed Policymakers are also scheduled to speak throughout the next seven days and should the signal for an easing of the Fed’s rate-cutting path be enhanced, we may see the market being forced to reposition itself by re-adjusting its expectations, thus weighing on US stock markets.

US October CPI rates to accelerate?

Today we highlight the release of the US October CPI rates, as the next big test for US stockmarkets. The headline rate is expected to accelerate to 2.6%yoy if compared to September’s 2.4%yoy, while on a core level the rate is expected to remain unchanged at 3.3%yoy. Overall, should the rates show a relative resilience of inflationary pressures in the US economy, we may see market expectations easing for another rate cut by the Fed in December, in turn weighing on US equity markets.

Upcoming and past earnings releases

We make a start by turning our attention to the mega market cap hight tech company NVIDIA, which is to release its earnings report next Wednesday. The EPS figure is expected to rise to 0.7435 from past 0.68, while also revenues for the past quarter are expected to be increased, reaching $32.97 Billion if compared to last quarter’s $30B. Overall expectations seem to be improving the company’s economic outlook and if realised or surpass forecasts, we may see the company’s share price getting some support. On a deeper fundamental level, the recent crypto frenzy, after Donald Trump’s re-election, may provide tail winds for the company’s revenue, while in Japan, NVIDIA and SoftBank Corp. seem to be accelerating the country’s path towards becoming a global AI Powerhouse, both issues being supportive for the company’s share price. Then we turn our attention to the US retail sector. Starting with Home Depot’s earnings report release yesterday. Home Depot released its earnings report yesterday and the release seems to have an upside potential. The EPS figure despite dropping came in higher than expected as did the revenue figure, practically preventing a possible blow for the share’s price. Furthermore, the company’s forward guidance was encouraging which may provide some support for Home Depot’s share price. Then we note the release of Walmart’s earnings report next Tuesday the 19th of November. The US retailer is expected to show a contraction of the EPS figure, to 0.53 in the last quarter from 0.67 in Q2 and a drop of the revenue figure is also expected from $169.3B in Q2 to $167.61B in Q3. The release could weigh on the share’s price should the actual figures be lower than expected and vice versa. On a deeper fundamental level, on the one hand the US brick and mortar retailer is facing intense competition from e-retailers such as Amazon, yet on the other hand the holiday season is fast approaching and increased sales for the season could provide support for the US retailer. Talking about retail sales, we also note the release of the US retail sales growth rate for October, due out on Friday. The US retail sales growth rates for October are expected to slow down both at a headline and core level and if so or even worse slow down more than expected, they may imply that the average US consumer is less willing or able to spend more in the US economy and thus could weigh on retail companies of the US stock markets.

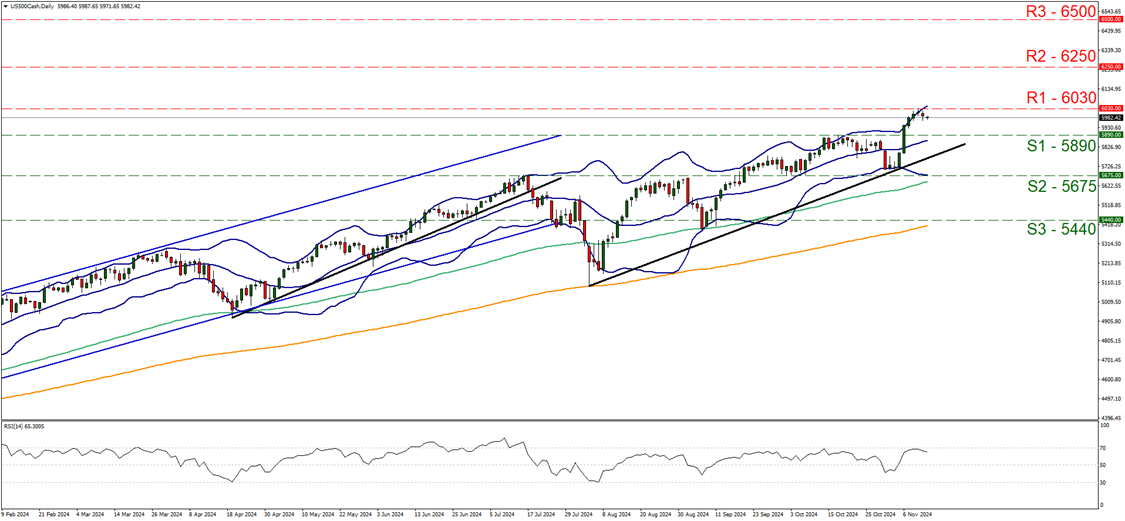

Technical analysis

US500 daily chart

-

Support: 5890 (S1), 5675 (S2), 5440 (S3).

-

Resistance: 6030 (R1), 6250 (R2), 6500 (R3).

S&P 500’s movement over the past week, forced us to recalibrate its resistance lines as the broad US equites index hit a new record high at the 6030 (R1) resistance level on Monday. Since then, the index’s price action tended to correct higher, yet the bullish tendencies seem to continue to be present as the RSI indicator correcting below the reading of 70, yet remains close by. Furthermore the upward trendline, guiding the index since the 5th of August remains intact, also implying a continuance of the bullish outlook despite a possible correction lower. It should be noted that the price action corrected lower after flirting with the upper Bollinger band, yet since the latest peak the distance between the price action and the upper Bollinger band has widened a bit allowing for some room for the bulls to play. Should the bulls regain control over the index’s direction, we may see S&P 500 breaking the 6030 (R1) resistance line and we set as the next possible target for the bulls the 6250 (R2) resistance level. Yet should the correction lower be extended, the foundations for a possible bearish outlook could be set. Yet a bearish outlook for the time being seems remote and for it to be adopted we would require the index’s price action to drop breaking the 5890 (S1) support line, continue to break the prementioned upward trendline, in a first signal of an interruption of the upward movement, and move even lower by breaking the 5675 (S2) support base.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69.80% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Our services include products that are traded on margin and carry a risk of losing all your initial deposit. Before deciding on trading on margin products you should consider your investment objectives, risk tolerance and your level of experience on these products. Margin products may not be suitable for everyone. You should ensure that you understand the risks involved and seek independent financial advice, if necessary. Please consider our Risk Disclosure. IronFX is a trade name of Notesco Limited. Notesco Limited is registered in Bermuda with registration number 51491 and registered address of Nineteen, Second Floor #19 Queen Street, Hamilton HM 11, Bermuda. The group also includes CIFOI Limited with registered office at 28 Irish Town, GX11 1AA, Gibraltar.

Recommended Content

Editors’ Picks

EUR/USD tumbles further and hit new YTD lows near 1.0580

The Greenback now resumes its uptrend and advance to new highs. forcing EUR/USD to abandon its initial constructive stance and reach new yearly lows in the 1.0580 region on Wednesday.

GBP/USD accelerates its losses below 1.2700

GBP/USD breaks below the 1.2700 support on the back of the sudden resurgence of buying interest in the US Dollar following US CPI data and some hawkish remarks from the Fed's Logan.

Gold extends slide to fresh two-month low

After shedding some ground throughout the first half of the day, the US Dollar is back in fashion. XAU/USD trades at its lowest in two months in the $2,580 region and is technically poised to extend its slump.

Australia unemployment rate expected to remain steady for third straight month in October

The Australian Unemployment Rate is foreseen stable at 4.1% in October. Employment Change is expected at 25K, much lower than the 51.6K posted in September. AUD/USD is under pressure and may soon pierce the 0.6500 mark.

Trump vs CPI

US CPI for October was exactly in line with expectations. The headline rate of CPI rose to 2.6% YoY from 2.4% YoY in September. The core rate remained steady at 3.3%. The detail of the report shows that the shelter index rose by 0.4% on the month, which accounted for 50% of the increase in all items on a monthly basis.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.