Equities markets were down for the week as volatility continued

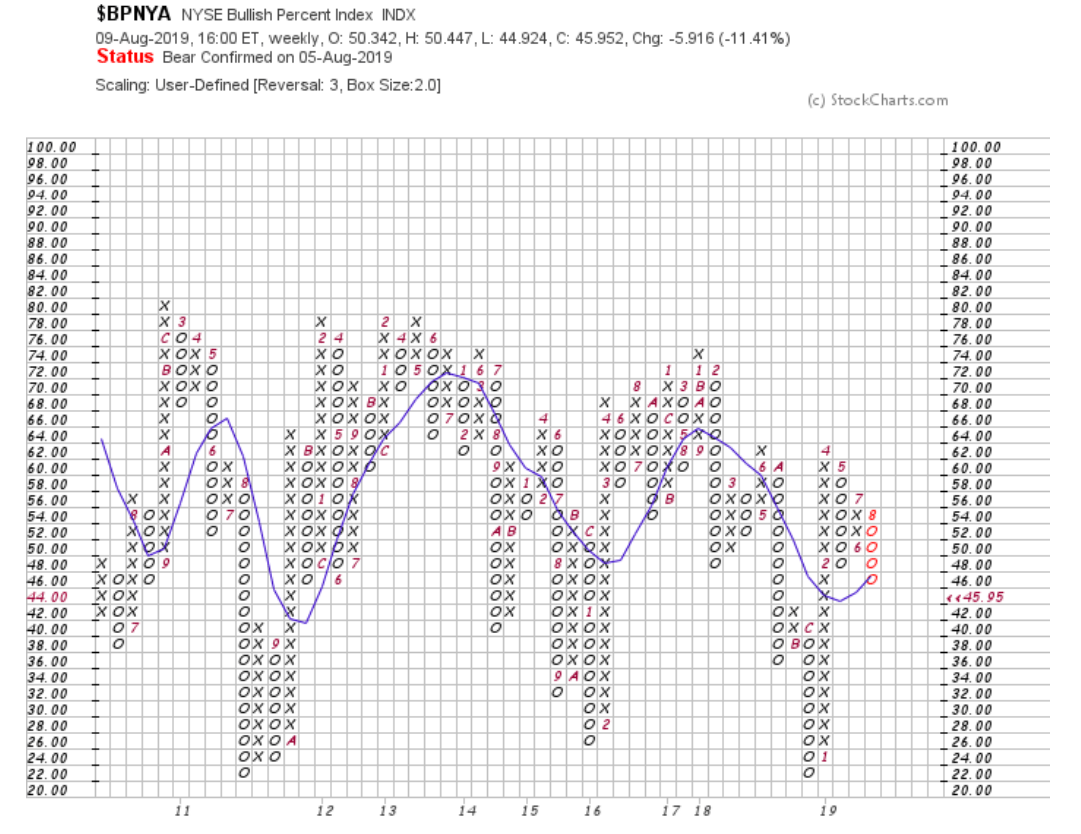

Long-term market internals broke below previous lows and now suggest further downside. Short-term market internals are not yet oversold despite bearish

sentiment. However, defensive assets are significantly overbought, suggesting a potentially precarious situation.

The Good:

- The S&P 500 has not broken below key moving averages or support levels.

- Several sectors remain in positive trends.

- The ECRI WLI is up 0.29% year-over-year.

The Bad:

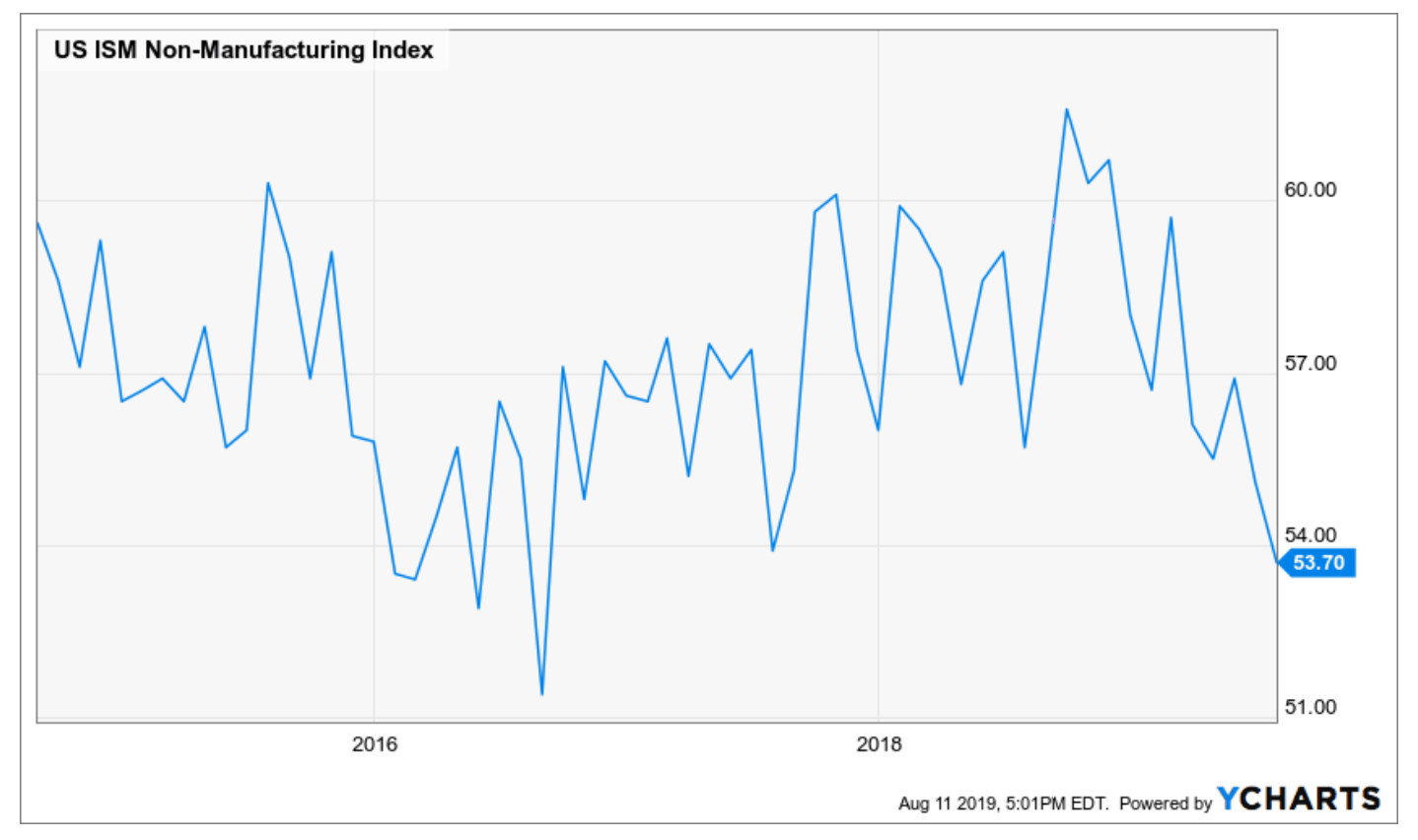

- ISM Non-Manufacturing PMI dropped last month.

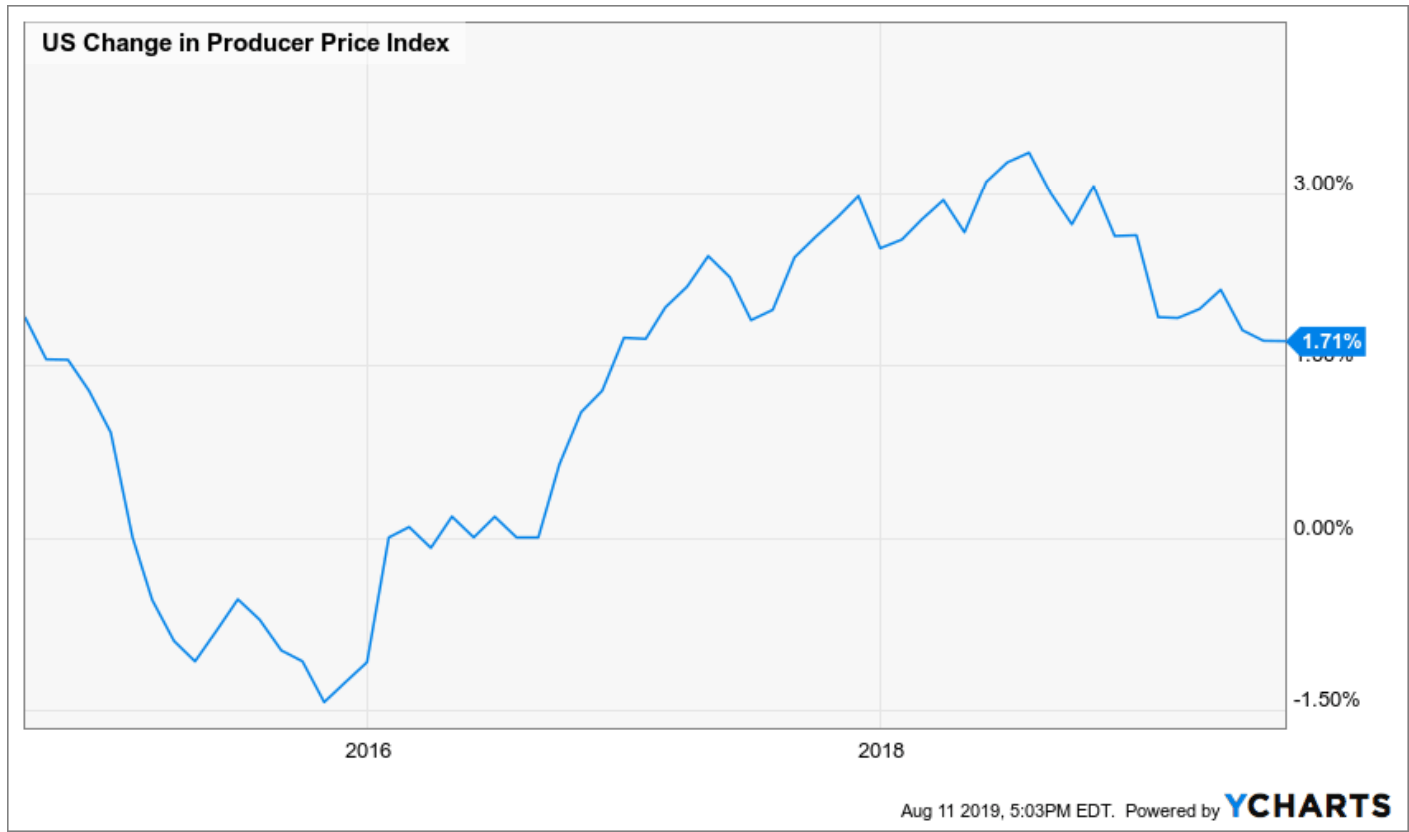

- Inflation continues to slow.

- The Dollar remains in a positive trend and the Yen was strong last week.

- Market sentiment is negative as the risk free asset is outperforming both international and domestic equities as well as high yield bonds in a majority of time frames.

The Ugly:

- The 4-week moving average of the ECRI WLI is negative -1.29% year-over-year.

- Credit spreads are not confirming the S&P 500 and are widening.

- Defensive factors and sectors are leading the market.

- The U.S. 10-year yield dropped 12 basis points and suggest slower growth.

Chart of the Week: Long-term market internals are breaking down. This suggests that equity markets could also break down.

Chart 2: The U.S. ISM Non-Manufacturing Index dropped to 53.70, the lowest level since the 2015-2016 slowdown.

Chart 3: Producer Prices show a continued slowdown in inflation on a year over year basis.

Author

Clint Sorenson, CFA, CMT

WealthShield

More from Clint Sorenson, CFA, CMT