ECB rate cuts will benefit bank loan quality

The strong boost from higher interest rates has ended. Banks relying more on fee-based income rather than solely net interest income and with the potential for mergers and acquisitions are somewhat better positioned.

The ECB shifts to rate cuts to support bank loan quality

European bank fundamentals have been supported by the positive effect of high interest rates and the (for the most part) relatively benign loan quality conditions. While we have seen a clear shift higher in non-performing loans in some specific sectors such as real estate and construction, the substantial revenue boost from high rates has largely offset these impacts on a net basis so far.

The ECB is however increasingly moving to a rate-cutting mode with 125bp of rate cuts expected by our economists by the end of 1H2025. We expect the interest rate cuts to negatively affect net interest margins, although some banks are relatively well hedged against this impact. It may be challenging to offset this effect solely through volume growth in the current economic climate. Southern European banks may get some support from stronger expected economic growth. To achieve growth, we think that the focus is increasingly turning to fee and commission income instead, alongside mergers and acquisitions (M&A).

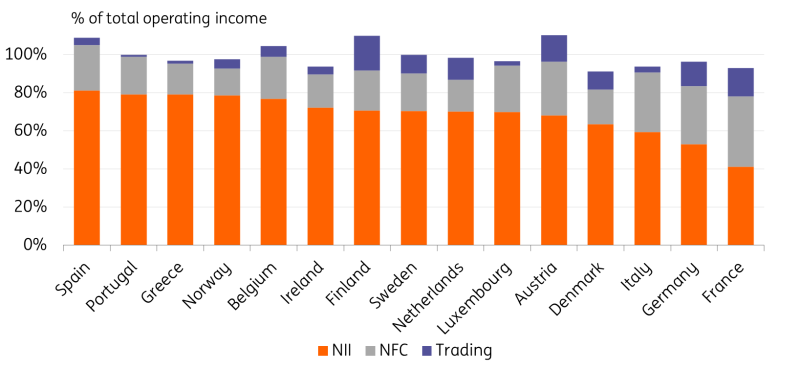

With lower rates, banks less reliant on NII are better off

Source: ING, EBA

We have seen more life in the European bank M&A scene this year than we have in years.

Two major eurozone banks are still pursuing their targets, and 2025 may give a better indication of how these stories will play out in the end. Both are facing tight resistance in the respective target countries.

If the deals do not succeed, we would take that as a sign that pulling off a merger or acquisition in the eurozone, despite apparent support and even encouragement from authorities, remains challenging due to substantial (possibly unofficial) barriers.

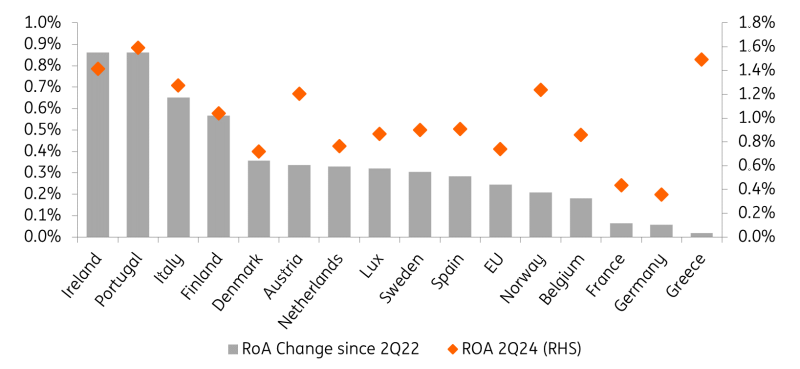

Eurozone periphery leads bank profitability higher

Source: ING, EBA

Since the ECB started its series of rate hikes, we have seen the return on assets improve by 25bp for EU banks based on EBA country data. In the eurozone, Irish, Portuguese and Italian banks have seen the strongest improvement since the summer of 2022, and in 2024 Greek banks showed the strongest improvement year-to-date.

The robust developments reflect higher net interest margins, supported by the ECB rate hikes between July 2022 and September 2023. Spanish banks have also benefited from the higher rates, but the improvement hasn’t significantly impacted their bottom line. Dutch banks fall somewhere in the middle. Only French banks haven’t seen their margins improve due to local regulations, which has resulted in their profitability lagging, placing them at the lower end of the range alongside Germany.

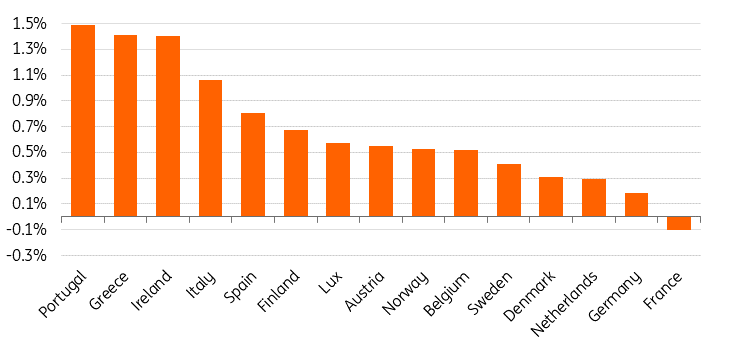

Rate hikes have contributed to stronger margins

Change in NIM since 2Q22.

Source: ING, EBA

Overall, the positive margin impact has counterbalanced the relatively minor decline in loan quality so far. Since the summer of 2022, EU banks have experienced a 6bp increase in their cost of risk, reaching 51bp, while the non-performing loan (NPL) ratio inched 5bp higher to 1.9%.

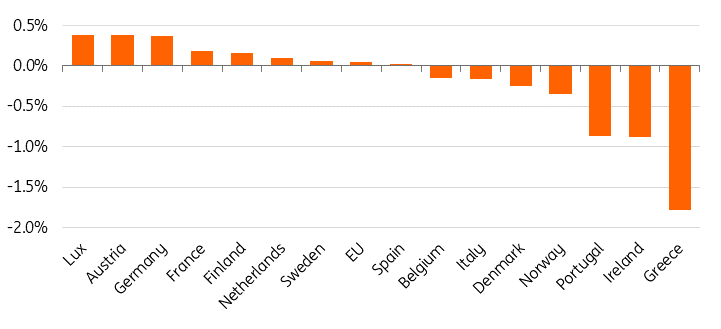

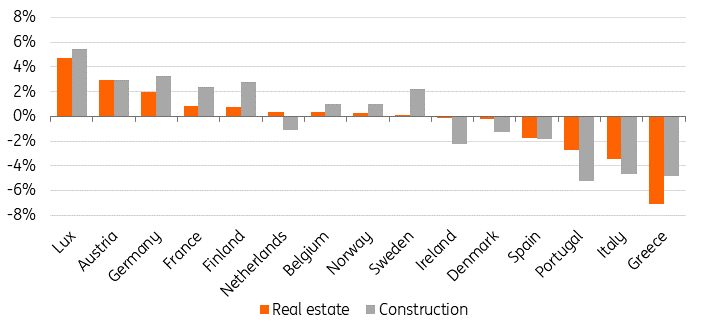

It is mainly banks with higher commercial real estate (CRE) exposure that have seen a stronger weakening in their loan quality metrics. The most significant increase in NPL ratios, nearly 40 basis points, was observed in banks from Luxembourg, Austria, and Germany, all of which have banking sectors heavily exposed to real estate.

Lux, Austria, Germany and France see NPLs grow

Change in NPL ratio, 2Q24 vs 2Q22.

Source: ING, EBA

…driven by the weakness in real estate-related lending

Change in NPL ratio since 2Q22.

Source: ING, EBA

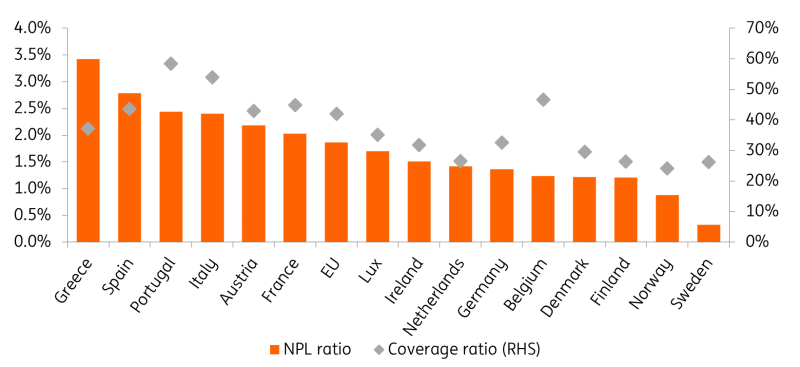

Despite these increases, the overall levels continue to remain below those of the eurozone periphery which still carries some legacy NPL burden.

The highest problem loans remain in the eurozone periphery

Source: ING, EBA

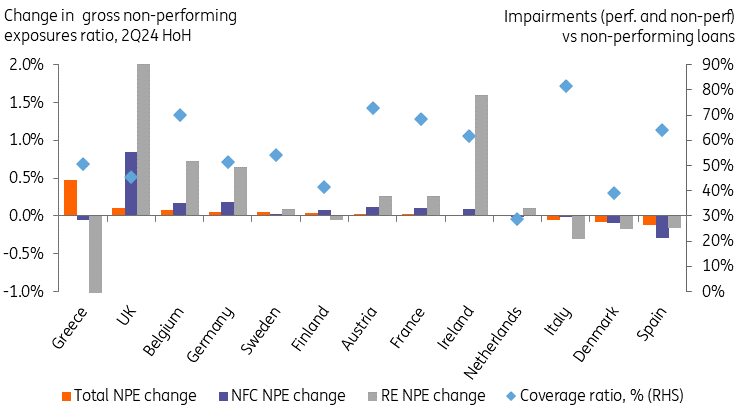

The chart below shows how non-performing exposures (NPE) for a selection of 39 banks performed in the first half of 2024 compared with the end of 2023, just before the ECB started to cut rates. For these banks, the NPE ratio was on average at a low level of 1.4%, just 3bp higher from the year-end with the coverage ratio including impairments for both non-performing and performing exposures a tad below 58%.

Furthermore, the non-performing exposures for non-financial corporates have increased, although only by 3bp on average, with the strongest increases reported by banks that have also seen their non-performing loans to real estate counterparties clearly increase at the same time.

The largest increases in non-performing exposures were reported by banks in Greece, the UK, Belgium and Germany. Of these, the share of problematic real estate assets increased in all the sampled banks but the Greek one. In contrast, banks in Spain, Denmark, and Italy all reported lower non-performing exposure ratios compared to the end of last year, coinciding with lower NPE for corporates and more specifically for real estate counterparties.

Most countries with the strongest increase in non-performing corporate loans also saw weaker real estate exposure

Note: data for 39 banks.

Source: ING, company data

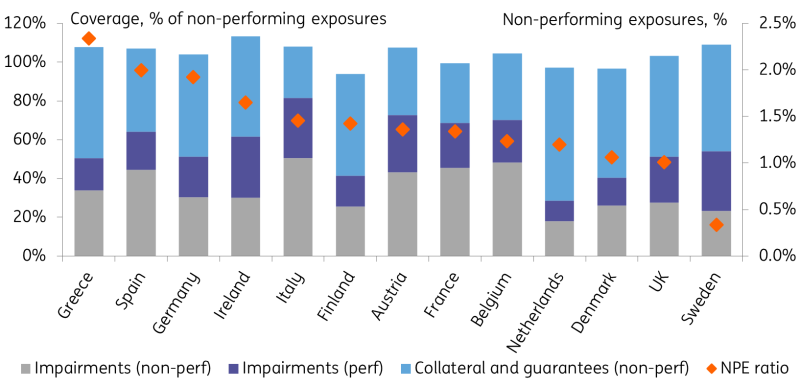

In terms of overall loan quality, Swedish banks are at the top of the range, with robust coverage for potential further weakening.

The highest problem exposures are for the selected German commercial real estate-centric banks that tend to have relatively limited direct coverage via impairments but have topped up the support with collateral and guarantees.

However, at the national level, Germany’s non-performing exposures are generally lower than those in Southern Europe. Spanish and Italian banks, which have higher NPE ratios, also have somewhat higher impairment coverage ratios, potentially mitigating the impact of further weakening on their earnings.

Banks are overall well prepared for weakening in exposures, while lower impairment coverage points to higher risk ahead

Note: data for 39 banks.

Source: ING, company data

To conclude, the strong tailwind from higher interest rates has come to an end, and banks are relying more on fee-based income instead of solely net interest income, with the potential for M&A a bit better positioned. This should include banks in Germany, Italy, Spain and France, for example, although French banks may suffer more from sovereign worries.

Loan quality should be supported by ECB rate cuts. We expect credit costs in 2025 to remain elevated but come below the levels seen in 2024. While we consider banks with a mix of higher NPEs and lower coverage more at risk for further weakness, those with higher NPEs will also benefit the most from the ECB easing measures. This should be helpful for banks with higher cyclical exposures such as real estate, in particular.

Although it’s too early to declare the all-clear, the ECB rate cuts are expected to alleviate some pressure on loan quality next year.

Read the original analysis: ECB rate cuts will benefit bank loan quality

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.