ECB monetary transmission: One size currently fits all

The European Central Bank's (ECB's) rate hikes so far have led to a tightening of financing conditions for households and businesses. While mortgage loan growth has already slowed, business borrowing is affected more by recession fears than by higher rates.

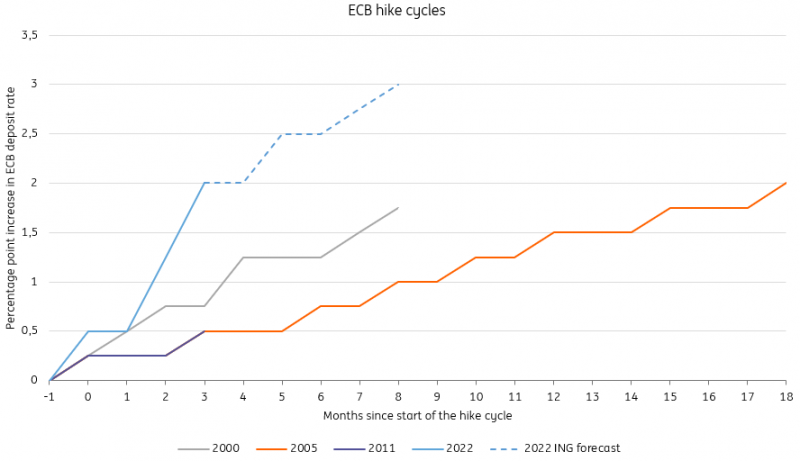

Slow out the gates, but the ECB is now hiking at a record pace

The rate of the current hike cycle in the eurozone is the fastest since the ECB came into existence in 1999. It took the ECB just three months to hike interest rates by 200 basis points, while in the previous tightening cycles it took 18 months. And it's not finished; we expect the ECB to hike interest rates by another 100bp before the end of the first quarter of 2023. After a long period of negative rates, this interest rate shock is intended to normalise monetary policy and cool off economic activity, which in turn will tame inflation in the medium term.

At this week’s ECB meeting, the discussion on how far to hike interest rates will be more heated and controversial. First officials have started to argue in favour of waiting for the rate hikes recently put in place to unfold their full impact on the economy as the usual delay in monetary transmission is considered to be 12 to 18 months. Others clearly sympathise with further aggressive rate hikes and focus instead on actual inflation and inflation expectations. So the question is: can we already see an impact of this year's rate hikes on the real economy?

This is the most aggressive hike cycle from the ECB ever

Source: ECB, ING Research

Are higher rates already having an impact?

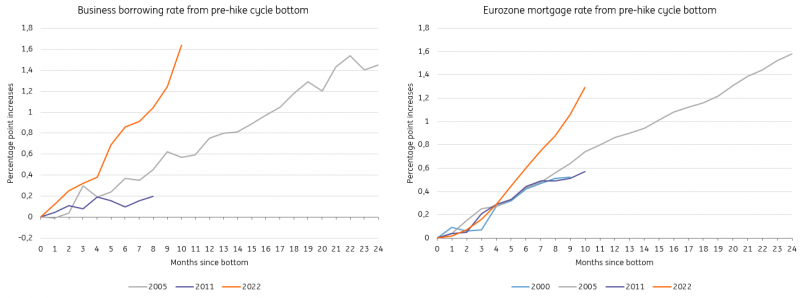

The simple answer is yes. In fact, the transmission of monetary policy tightening started well before the hike cycle actually began. The long end of the curve started to increase materially when the ECB announced tapering in December, but also because of anticipation of rate hikes and higher inflation. Average borrowing rates for businesses and households increased significantly, mimicking the ECB’s policy rate hikes. When comparing to previous hike cycles, it’s hard to show exact timings as the anticipation of hikes already increases the long end of the curve, which is an important driver of business and household borrowing rates. So in charts 2 and 3, we measure the increase in rates for businesses and households starting from their trough. This is mostly just before the ECB started hiking.

Business and household borrowing rates have adjusted accordingly

Source: ECB, ING Research

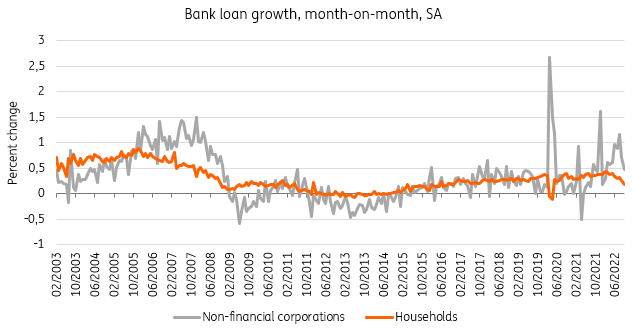

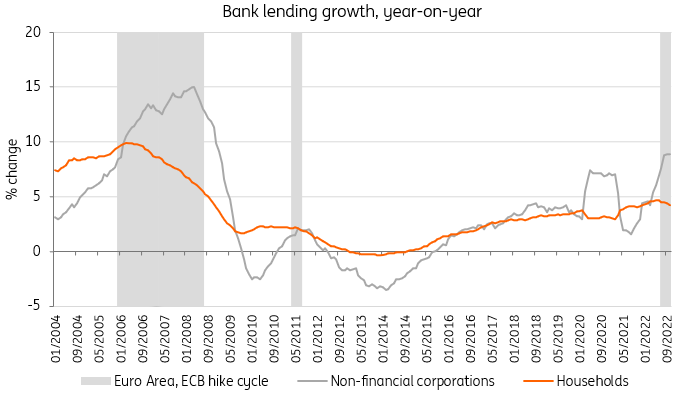

Interestingly, and despite the fact that both interest rates for business and mortgage loans have increased proportionally, the impact on actual loan growth shows a large divergence. Mortgage loan growth has come down significantly, while business borrowing – although volatile – has seen strong months despite higher nominal rates. The ECB bank lending survey shows, however, that this is not because of investment opportunities, but mostly due to working capital and inventory reasons. With high input costs and businesses now stocking up – with inventories having been depleted amid shortages – this has required extra borrowing. Demand related to business investment has been falling for the past two quarters according to the survey. So non-financial corporate borrowing is currently elevated, but not because of investment plans. That suggests that the impact of higher rates is being felt across the board.

Business borrowing remains elevated, but not for investment reasons

Source: ECB, ING Research

What we are currently witnessing is a usual pattern in a rate hike cycle: mortgages do adjust more quickly than business borrowing. The volume of lending to non-financial corporates generally only starts trending down at the end of the tightening cycle. That suggests that business borrowing is less interest rate sensitive than mortgage borrowing. However, in the past, hiking cycles also led to economic slowdowns or even recessions. At the current juncture, the recession is already triggered by the energy price crisis and the impact of the hiking cycle will be overlapping. As a result, once business demand for working capital is satisfied, the full impact of higher rates on business borrowing looks likely.

Households usually adjust borrowing to higher rates more quickly than businesses

Souce: ECB, ING Research

No evidence of unwarranted differences in tightening between large economies so far

Turning to the transmission of the ECB’s tightening of monetary policy in the three largest economies up to now, we see that mortgage interest rates and business borrowing interest rates have increased the most in Germany since the beginning of the year and the least in France. At the same time, however, the spread between French and Italian government bond yields with Germany has widened this year (although spreads have fallen again since mid-October).

That wider spread in government bonds is also reflected in longer-term interest rates for businesses, but remains far from unwarranted tightening in these countries either. Loans with a maturity of more than five years have seen an increase in rates to just over 2.5% in Italy in October, while they stood at 1.7% and 1.9% in France and Germany, respectively. So for now, there is no evidence of extreme transmission of policy in countries with higher government bond yields.

The transmission of the ECB’s policy rate hikes so far will definitely be a hot topic at this week’s meeting. For both households and corporates, there has already been a clear tightening of financing conditions. A tightening that is already reflected in weaker mortgage growth but not yet in business borrowing. Interestingly, the tightening of financing conditions is not showing unwarranted tightening in peripheral markets, and government bond spreads have even fallen over the past two months. While tighter financing conditions should support calls for a slowing of the rate hike pace, there currently doesn’t seem to be a need to protect the transmission of monetary policy.

Read the original content: ECB monetary transmission: One size currently fits all

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.