ECB and BoC decisions next week amidst the ongoing US-China trade war

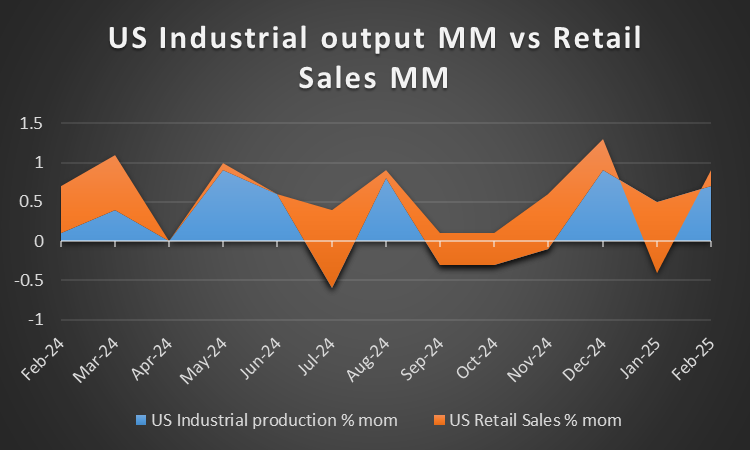

The week is drawing to a close, and as usual, we open the door to see what next week has in store for the markets. Starting on Monday, we note the UK’s house price Rightmove rate for April and China’s trade balance figure for March. On Tuesday we note the RBA’s April meeting minutes, the UK’s unemployment rate, Germany’s ZEW economic sentiment figure and Canada’s BoC Core CPI rate for March. On Wednesday we get Japan’s machinery orders rate for February, China’s GDP rate for Q1,the UK’s CPI rate, the Eurozone’s final HICP rate for March, the US’s retail sales and industrial production rates for March as well and ending the day is the BoC’s interest rate decision. On Thursday, we get New Zealand’s CPI rate for Q1, Japan’s trade balance figure and Australia’s employment data both for March, the CBT’s interest rate decision, the US weekly initial jobless claims figure, the US Philly Fed business index figure for April and the ECB’s interest rate decision. Lastly, on Friday we note Japan’s nationwide CPI rate for March.

USD – Tariff narrative takes over

On a macroeconomic level, the main event for dollar traders this week was the release of the US CP rates for March. The CPI rates were expected by economists to showcase easing inflationary pressures in the US economy and tended to do so following their release with the figure coming at 2.4% on a year-on-year basis which is lower than the prior and expected rate of 2.8% and 2.5% respectively . The lower-than-expected CPI rates may weigh on the dollar, as it may provide the Fed with some leeway should they wish to cut rates in the near future.

Sticking to the Fed on a monetary level, the FOMC’s last meeting minutes were released earlier this week. In the bank’s minutes Fed policymakers appeared to be concerned over the resilience of the US economy with participants stating that “These moves appeared to reflect increased perceived risks—rather than a base case—of a significant deterioration of the U.S. outlook” as a result of the developments in trade policy. However the comment that “As a result, participants generally saw increased downside risks to employment and economic growth and upside risks to inflation while indicating that high uncertainty surrounded their economic outlooks” tends to paint the narrative that the Fed may adopt a wait and see approach.

On a fundamental level, US President Trump tariff plans have been shelved with the President stating that he would be placing a 90-day pause on higher tariffs. During the course of this week, we saw · China and the US trading tariff blows with both nations increasing tariffs on each other. Yet, the most recent development of “pausing” the tariffs tends to showcase a willingness by the US administration to come to the negotiation table to find an amicable trade deal.

Analyst’s opinion (USD)

“It has been an incredible week for dollar traders. The announcements by Trump and the tariff blows between the US and China have kept us all on the edge of our seats, with the narrative changing on an almost hourly basis. A little unorthodox, but we would like to note that the fact that Trump decided to add his initials ‘DJT’ on his TruthSocial post that “THIS IS A GREAT TIME TO BUY” implies to this author that the President felt the need to personally reassure market participants. As such we would not be surprised to see the US announcing trade negotiations and progress on trade deals to fix its deficit with its trading partners. Yet we must remember that this is Trump we are talking about and thus the picture could easily change in the coming week”

GBP – UK CPI rates next week

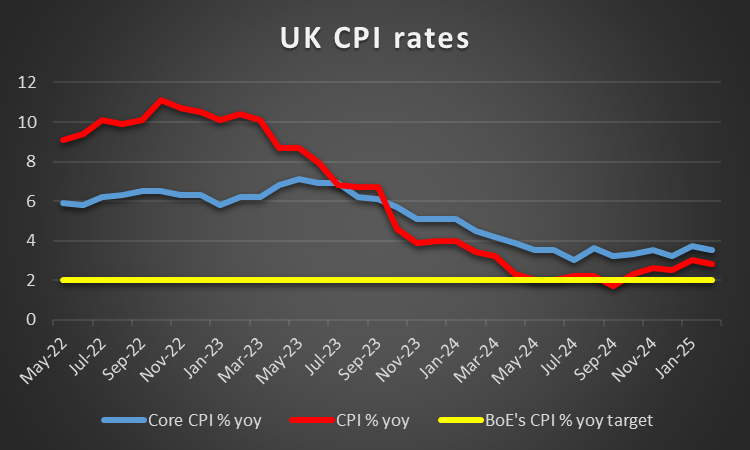

On a macro-economic level, it’s been a pretty easy going week for pound traders with the exception of the Halifax House Prices rate which came in lower than expected on a month-on-month basis at -0.5% versus the expected rate of 0.2%. However, of greater interest may have been the release of the UK’s GDP rates for February earlier on today which came in better than expected, which in turn may have aided the pound as the week comes to an end. For next week, we would like to note the UK’s unemployment rate for February and their CPI rates for March. Starting with the unemployment rate, should the financial release showcase a resilient labour market, it may be seen as a positive for the UK economy which in turn could aid the pound and vice versa. Moving on to the CPI rates, should the showcase stubborn or even an acceleration of inflationary pressures in the UK economy it may increase pressure on the BoE to adopt a wait and see approach which could aid the pound. Whereas easing inflationary pressures could increase calls for the bank to continue on their rate cutting cycle which could weigh on the sterling.

On a political level, we note that UK Prime Minister Keir Starmer earlier on this week had pledged to sign a trade deal with the US only if it was in the UK’s national interest. The UK according to the BBC was hoping to sign a deal with the US to limit the impact on the UK in exchange for tax changes on · big tech firms. However, with Trump’s announcement yesterday that the tariffs would be postponed for another 90 days, the impact on the UK economy may not be seen in the near future.

Analyst’s opinion (GBP)

“The financial releases from the UK may influence the sterling. Yet as was seen this week the narrative stemming from the US tends to dominate the market sentiment and news airwaves and thus should significant news emerge from the US and in particular references to tariffs, the financial releases stemming from the UK may be overshadowed. ”

JPY – CPI rates next Friday

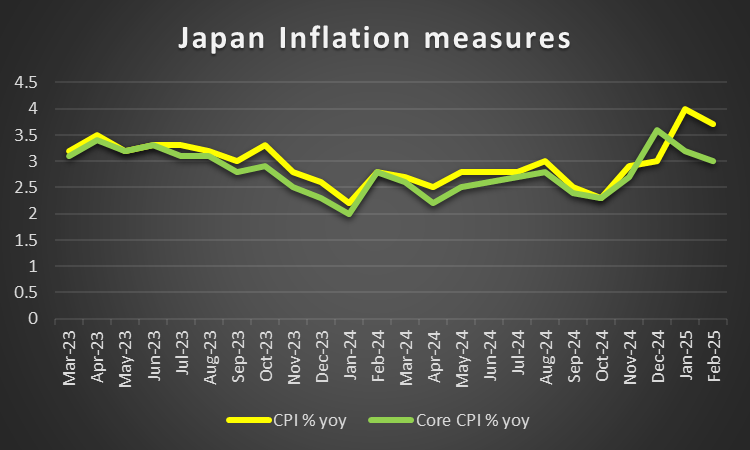

On a macroeconomic level, this week was easy going for Yen traders with no major financial releases from the nation. Thus, we turn our sights to next week’s nationwide CPI rates for March which are set to be released on Friday. Should the CPI rate come in higher than the prior rate of 3.7% it would imply an acceleration of inflationary pressures in the Japanese economy, which in turn could open the door for the BOJ to return to their rate hiking cycle, thus potentially aiding the JPY. However, a lower CPI rate which would imply easing inflationary pressures could have the opposite effect and could thus weigh on the Yen.

On a monetary level the highlight for Yen traders may have been BOJ Governor Ueda’s comments who per Reuters stated that “we need to pay due attention to risks, especially recent heightening uncertainty over developments in each country's trade policy," implying that the bank may remain on hold in the foreseeable future until a clearer picture emerges on the potential tariffs being imposed by the US on Japan. Nonetheless, should BOJ policymakers imply that they may resume their rate hiking cycle it could aid the JPY.

However, as we have mentioned in previous paragraphs in this report, Trump’s decision to postpone the implementation of tariffs for 90 days may provide some reprieve for traders and thus could provide some leeway for the bank should they decide to hike rates.

Analyst’s opinion (JPY)

“The BOJ is placed in a difficult like every other central bank as a result of Trump’s tariff rhetoric. The 90-day reprieve could allow the bank to hike in their next meeting should inflation appear to be accelerating.

Yet, any hawkish rhetoric or actions from the BOJ may be limited in nature for the next 90 days until and if a trade deal emerges with the US, otherwise we are back to square one ”

EUR – ECB decision to occur next week

The EU’s relationship with the US is on fragile turf, with the EU having prepared their countermeasures against Trump’s implied tariffs. The EU specifically had prepared a retaliatory 25% tariff on US goods, yet at the time of this report appears to have rescinded that decision following Trump’s announcement to postpone his tariffs for the next 90 days. In turn things appear to have calmed down temporarily, yet unless the EU manages to secure an agreement with President Trump in the next few months we may return to the volatility seen earlier on this week in the EUR and the European Equities markets.

On a monetary level, the ECB’s interest rate decision is set to occur next week. The bank is widely expected by economists to cut rates by 25 basis points with EUR OIS currently implying a 94.75% probability for such a scenario to materialize. Thus with market participants all but having fully priced in a rate cut by the ECB we turn our attention to the bank’s accompanying statement. Should the accompanying statement showcase a continued concern for the resilience of the European economy in spite of Trump’s 90 day pause on tariffs, it may imply that the ECB could continue cutting rates in the near future which may weigh on the EUR. On the flip side, should the ECB showcase concern about a resurgence of inflationary pressures it may imply that the bank could remain on hold which may aid the common currency.

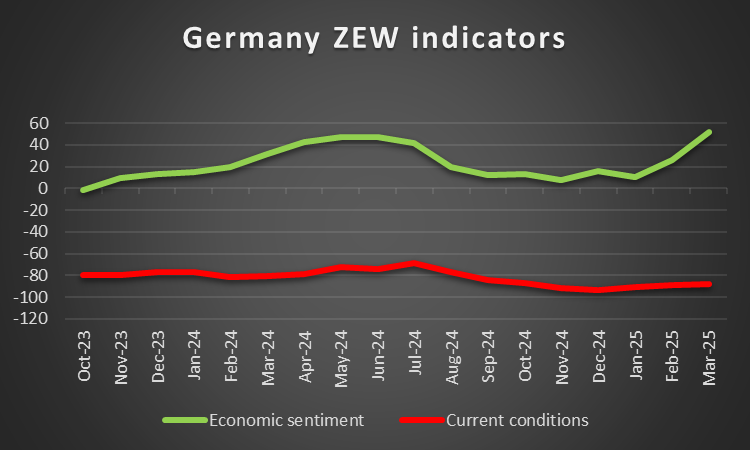

On a macroeconomic level Germany’s CPI rates for March came in lower than expected implying easing inflationary pressures in one of the most important economies in the Zone. However, due to the ongoing tariff narrative during the week, the release may have been glossed over. Nonetheless, for next week would like to note Germany’s ZEW economic sentiment figure for April as a gauge for the health of the consumer side of the economy. An improvement in the figure may aid the EUR and vice versa.

Analyst’s opinion (EUR)

“The tariff narrative has taken over the direction of the EUR. In spite of easing inflationary pressures in Germany, the EUR appears to be gaining against the dollar,pound and Yen , showcasing how the narrative emerging from EU Leaders and US President Trump has dictated the week. Our view is that the ECB may adopt a wait-and-see approach even if they do decide to cut rates next week. Our reasoning is that the situation is so dynamic that significant developments could happen in the upcoming week in regards to the trade wars and thus this uncertainty might be something the ECB may be looking to ‘hedge’ against.”

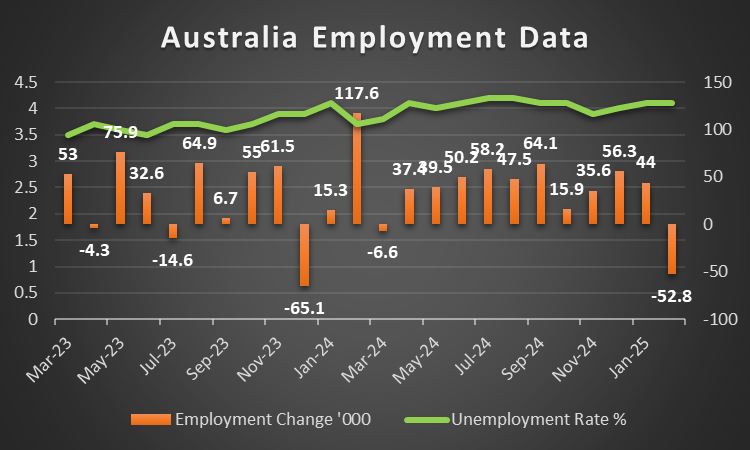

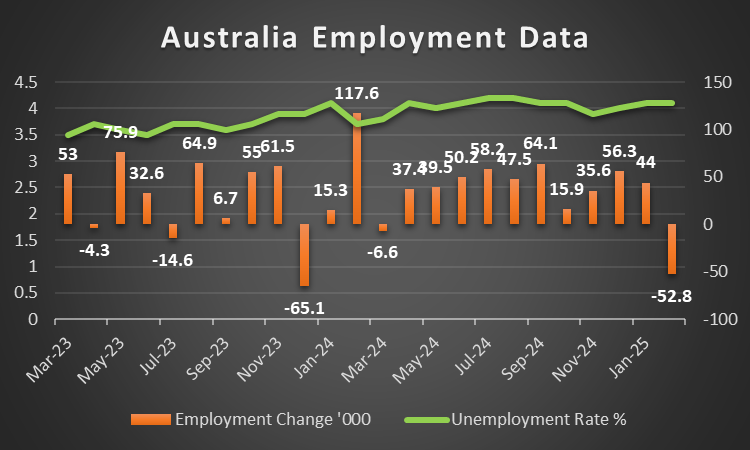

AUD – RBA meeting minutes due out next week

On a monetary level the RBA’s last meeting minutes are set to be released next Tuesday. The minutes may provide further clues into the bank’s inner deliberations and the mentality of policymakers as to how they may approach their next decision. Therefore, should the minutes showcase a willingness by the bank to cut rates it may be perceived as dovish in nature which in turn could weigh on the Aussie. On the other hand, should the minutes showcase a restraint by policymakers thus implying keeping interest rates steady, it may be perceived as hawkish in nature which in turn could aid the AUD. However, given that the bank’s decision was taken before the rapid changes in the ongoing trade wars which occurred last week, the effect of the minutes on the FX market may be limited in nature.

On a macroeconomic level, no major financial releases emerged from Australia during this week. Therefore, we take a look into next week’s releases, where Australia’s employment data for March is set to be released on Thursday. Should the nation’s employment data showcase a loosening labour market, it may imply a worsening economic outlook for Australia, which in turn could weigh on the AUD. On the flip side, should the employment data showcase a resilient labour market it may aid the Australian dollar.

Fundamentally speaking, Australia has been placed in a difficult spot between China and the US as their trade wars intensify. Specifically, the US and China have been trading blows over the past week with both nation’s announcing retaliatory tariffs almost on a daily basis. Overall, should the trade war negatively impact China’s economy, it may inadvertently weigh on the Aussie as well given their close economic ties.

Analyst’s opinion (AUD)

“In our view, the dollar may continue weakening in the coming week which in turn could aid the Aussie. However we cannot stress enough that the ongoing trade war between China and the US may negatively impact China’s economic growth over the long term. Therefore, given Australia’s and China’s close economic ties, at a certain point the negative connotations as a result of a trade war between the US and China could spill over into the AUD.”

CAD – BoC to cut by 25 bp?

On a monetary level, we note that the BoC’s interest rate decision is set to take place next Wednesday. The majority of market participants are currently anticipating the bank to cut rates by 25 basis points with CAD OIS currently implying a 66% probability for such a scenario to materialize. Therefore, should the bank cut rates as is currently expected by market participants it may weigh on the Loonie. Moreover, we would like to highlight the bank’s accompanying statement which may provide insight into the bank’s considerations into the ongoing trade war between the US and its trading partners. Should the bank showcase hesitancy to continue cutting rates in the future it may aid the Loonie as it could be perceived as hawkish in nature. On the other hand, should the bank imply that it may continue cutting rates it may have the opposite effect and could thus weigh on the CAD.

On a macrolevel we highlight the release of Canada’s Ivey PMI figures for March which where released this Tuesday. The financial release came in lower than expected at 51.3 versus 53.2 and even lower that the prior figure of 55.3 implying a worsening manufacturing sector of in the Canadian economy. The lower-than-expected figure may have temporarily weighed on the Loonie. Yet as a result of the ongoing trade wars and the weakening dollar, the financial releases may have been overlooked. For next week traders may be looking forward to the release of the BoC Core CPI rate for March which is due out on Tuesday. Should the Core CPI rate showcase an acceleration of inflationary pressures in the Canadian economy it may increase pressure on the BoC to remain on hold which in turn could aid the CAD. On the flip side, should the Core CPI rate showcase easing inflationary pressures it may weigh on the Loonie.

Analyst’s opinion (CAD)

“The BoC’s interest rate decision may be the main event next week for Loonie traders. In our view, we wouldn’t be surprised to see comments by policymakers in regards to the ongoing trade wars and their risks to the global economic outlook and the possibility of a resurgence of inflationary pressures. Moreover, we wouldn’t be surprised to see the bank implying that they may need a clearer picture on the tariff narrative before continuing on their rate cutting path.

General comment

As a closing comment, we expect the USD to maintain the initiative in the FX market in the coming week given the dynamic situation emerging as a result of Trump’s tariff announcements. As for US Equities markets the bleeding appears to have been temporarily halted, the degree of uncertainty still surrounding the markets may imply that this is simply the beginning. As for gold’s price, the precious metal formed new all time highs as the global economic outlook remains uncertain as a result of the blows being traded between the US and China. Therefore, we would not be surprised to see the precious metal gaining from safe haven inflows in the coming week as well.

Author

Phaedros Pantelides

IronFX

Mr Pantelides has graduated from the University of Reading with a degree in BSc Business Economics, where he discovered his passion for trading and analyzing global geopolitics.