Don’t call it a comeback, ISM been here for years

Summary

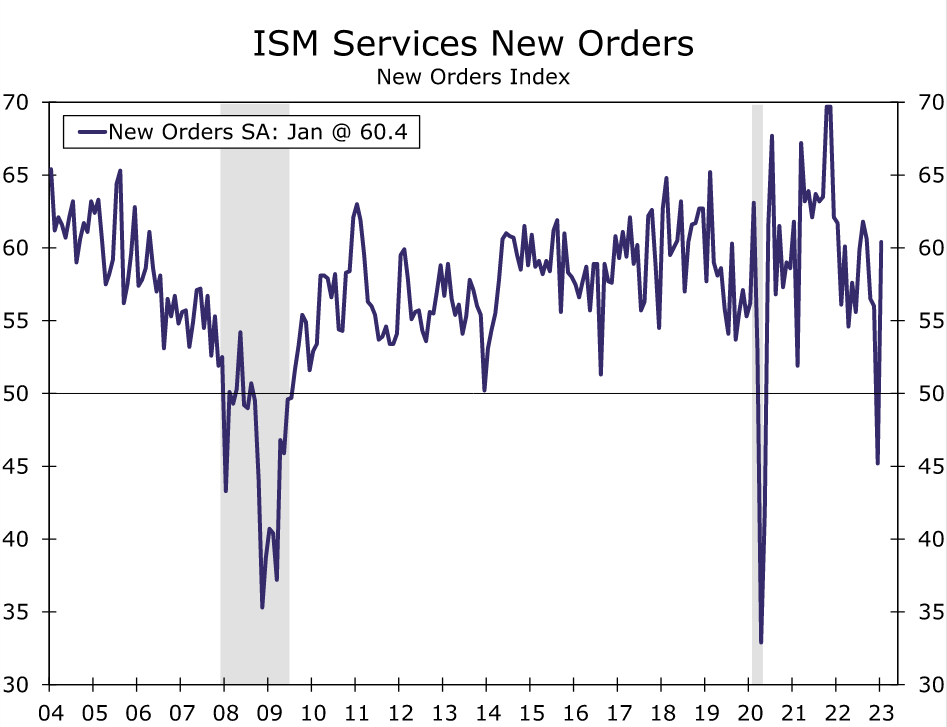

After just a single month in the penalty box, the services ISM shot back up into expansion. New orders posted a stunningly swift rebound of more than 15 points to rise to 60.4. While December now looks like a blip, the breadth of services expansion has still slowed.

Easy to talk away weakness

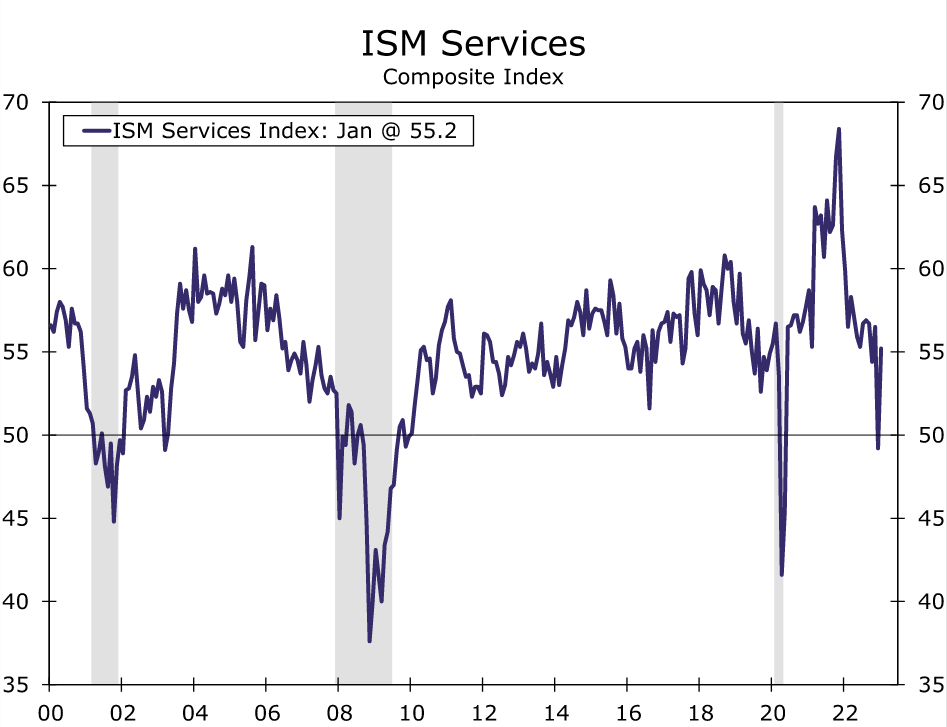

The slowdown in services activity to end last year now looks more like a blip rather than the start of a lasting slowdown in the sector. That's at least according to the latest ISM services release, which revealed the index advanced 6.0 points to 55.2 after a temporary drop below 50 in December (chart). Ten of 18 industries reported growth during the month, and of the eight in contraction the only one to really surprise us was Arts, Entertainment & Recreation. Recall that this report extends beyond traditional 'service' industries and reflects the non-manufacturing side of the economy. Other areas of weakness in the January ISM services report (retail, wholesale trade, transportation & warehousing and mining) were consistent with weakness in goods spending. A pullback in construction also reflects a housing sector in correction, while information and finance & insurance reflects some right-sizing in those industries and a higher rate environment. While we find it easy to talk away some of the weakness in this report, month-to-month movements in the ISM can be volatile and the breadth of expansion has eased.

That said, most components of the ISM improved, with the measure of business activity up 6.9 points to 60.4 and new orders matching that index level leaping 15.2 points after registering contraction in December (chart). New orders now match the highest level registered over the past 12 months, an indication that activity continues to hold up in the services sector.

"Shortened lead times and increased fill rates"

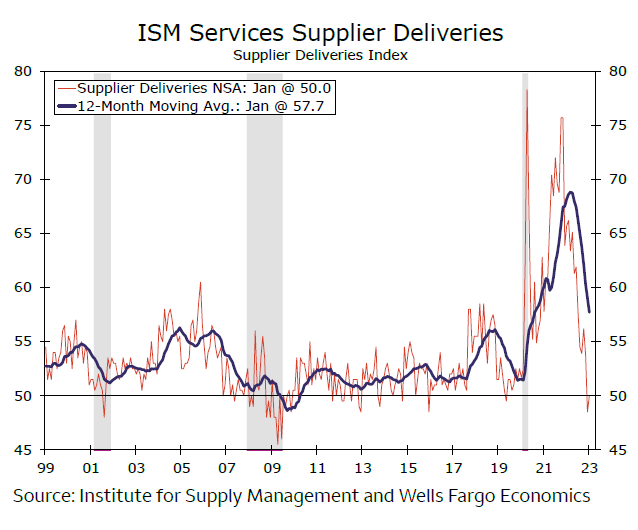

The supplier deliveries index came in right at the breakeven 50, adding 1.5 points from December's reading of 48.5 (chart). After months of hand-wringing about the state of the supply chain situation, there are indications that the gradual improvement continues. Respondents noted: “Post-holiday freight has proven to be more efficient” and “shortened lead times and increased fill rates.”

To some extent, firms are learning to operate better despite only modest improvements. The healthcare profession has been beset by shortages since the onset of the pandemic and the scramble to procure an adequate supply of personal protective equipment. A respondent from the healthcare trade noted that demand "for services remains high, yet we continue to satisfy demand despite continuing supply chain disruptions."

As supplier delivery times improves, the inventory draw down has become less urgent with that component rising more than four points to 49.2; still in contraction, but only barely. The sentiment about inventories at 55.8 is roughly unchanged from last month and suggests that stockpiles are still too high on balance.

The easing of supply problems is also somewhat benefiting price pressure. At 67.8 the prices paid index remains firmly in expansion, but it has declined the past four consecutive months.

Author

Wells Fargo Research Team

Wells Fargo