Don't blame production slump on hurricanes

Summary

The outlook wasn't brilliant for industrial production that day. The consensus expectation was for a decline of 0.4% in October. The actual reported decline was "just" 0.3%, although downward revisions to prior data nullified any sense of relief from that.

No joy in muddville

October came with a strike at Boeing and hurricanes that disrupted activity, but the fact of the matter is the slump in industrial production is bigger than these one-off factors and output is not yet seeing relief from lower interest rates. In fact, a supplemental note in today's release clocked the drag from hurricanes as a drag of just 0.1 percent.

It is an unfortunate commentary on the state of affairs that the best that can be said about October industrial production is that the decline of 0.3% is a bit less than the 0.4% drop that was the glum consensus expectation (chart). Yet even this modest consolation turns out to be a hollow one after noting that last month's 0.3% decline was revised lower to report an even bigger drop in September output of 0.5%.

The Federal Reserve's base year for industrial production is 2017 and output set such that 2017=100 for the index. The October reading is 102.3. In the years since 2017, total industrial production has grown less than 3%.

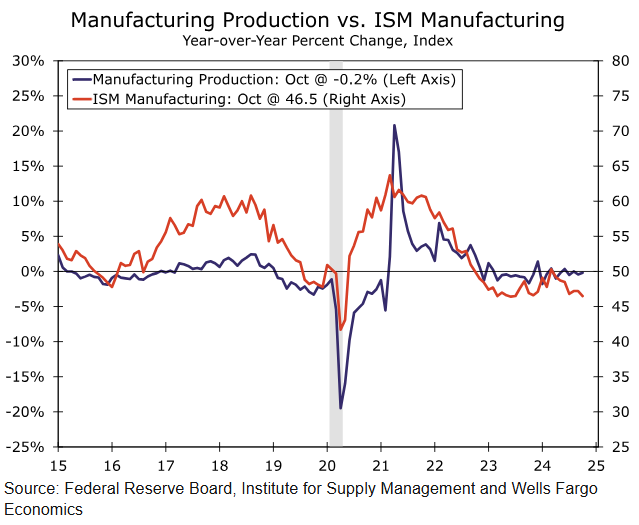

For manufacturing production, the backdrop is worse (chart). The October reading there is 98.5, meaning output is actually down since 2017. The weakness here transcends politics; at its zenith during the past 15 years, manufacturing output never exceeded a reading of 102. Manufacturing production fell again in October just as it has in three out of the past four months.

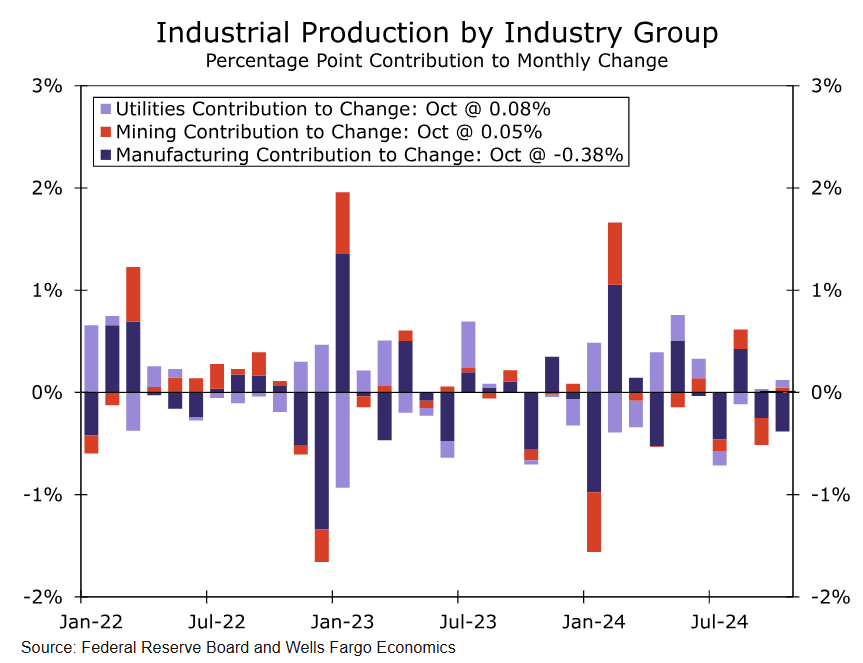

Utilities and mining production, which together comprise about a quarter of overall production both eked out modest gains in October.

Author

Wells Fargo Research Team

Wells Fargo