Dollar rallies but is it another chance to sell as traders eye Non-farm Payrolls?

Market Overview

Risk is marginally positive and the dollar is ticking higher in front of Non-farm Payrolls. However, despite the minor recovery in the dollar as the week has progressed, there is still a trend of using dollar rallies as a chance to sell. This is reflected in the market pricing for December’s Fed Funds Futures which are suggesting a probability of just around 35% for a rate hike. US Treasury yields continue to track lower and yesterday’s personal consumption data has hardly helped the situation. The Fed’s preferred inflation gauge, the core PCE has fallen back further to +1.4% and will likely keep the downward trend of yields intact. The market moves into today’s payrolls data almost as a free hit. There is no chance of a September hike although the Fed is likely to announce balance sheet reduction in the meeting in a couple of weeks. So a positive report will be positive for the dollar but also positive for risk appetite, with the market knowing that a rate hike is in no way imminent. Headline jobs and average earnings will be the two main components to watch.

Wall Street maintained the improvement in sentiment yesterday as the Dow broke higher again and the S&P 500 was +0.6% higher at 2471. Asian markets have also been positive in the wake of a better than expected China Caixin manufacturing PMI, with the Nikkei +0.2%. European markets tend to trade cautiously ahead of payrolls but there is mild cautious optimism in the early moves. In forex, the dollar is just taking back some of yesterdays renewed losses, but little direction is expected tin front of payrolls. In commodities, gold has slightly unwound some of yesterday’s gains, around $2 lower, whilst oil is also giving back some of yesterday’s sharp gains.

It is a day packed with tier one economic data as the Manufacturing PMI surveys and payrolls dominate proceedings. We start off with the European PMIs, with the Eurozone final Manufacturing PMI at 0900BST expected to stay at 57.4. The UK Manufacturing PMI is at 0930BST and is expected to dip very slightly to 55.0 (from 55.1 last month). The US Employment Situation will be the primary focus for trader today though, with the headline Non-farm Payrolls expected to drop back to 180,000 from last month’s strong 209,000. In the wake of Wednesday’s ADP employment change (private payrolls) which significantly bear expectations at 237,000, the expectations of another positive surprise in the payrolls report will be high. However look out for other components in the report with Average Hourly Earnings specially being watched. A rise in the year on year to +2.6% would be a welcome improvement, but still not suggest any major upside traction. Also watch the unemployment readings, with a debate over whether unemployment has finally bottomed. Headline unemployment is expected to stick at 4.3% whilst also the U6 unemployment (which includes underemployment) will be interesting after staying around 8.6% recently. Also watch the participation rate which has picked up recently to 62.9 and a move above 63.0 would be a notable improvement. Later in the afternoon the US ISM Manufacturing data is released at 1500BST which is expected to improve slightly to 56.5 (from 56.3) whilst the final Michigan Sentiment is also at 1500BST and is expected to stay at 97.4.

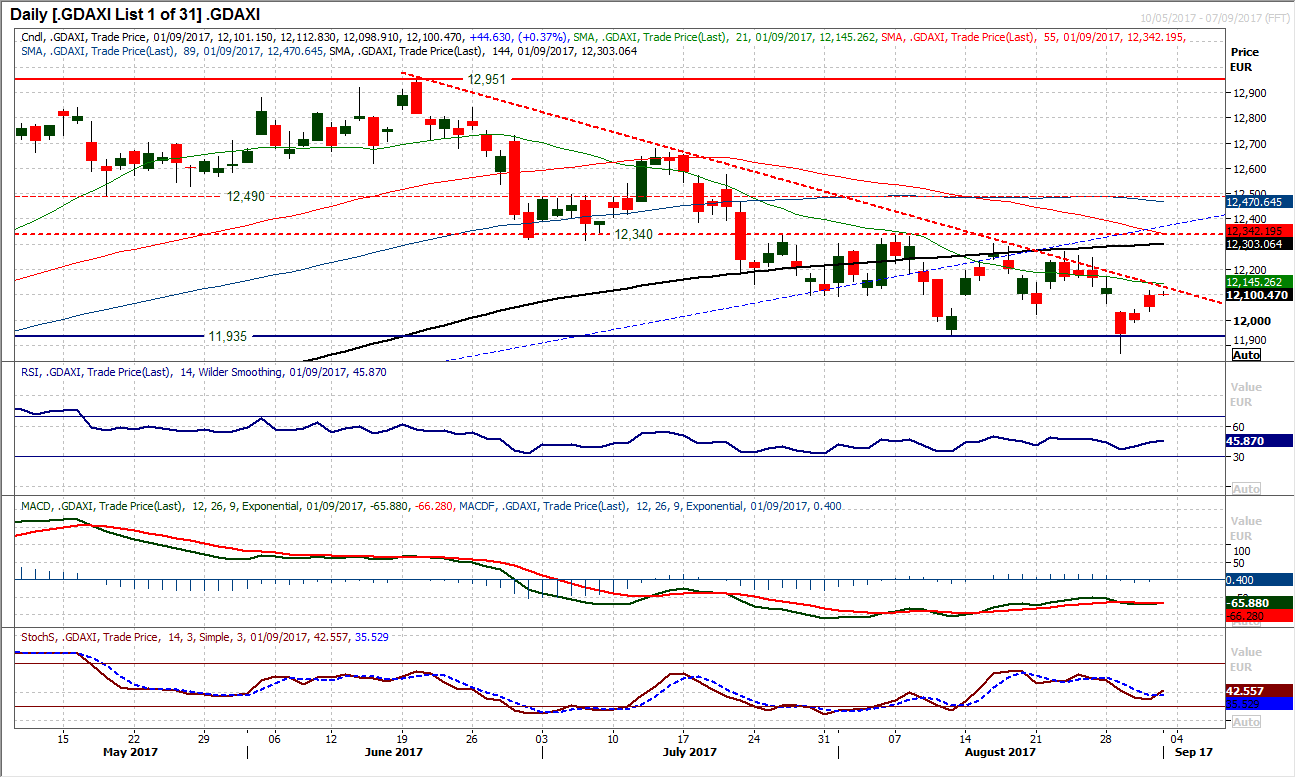

Chart of the Day – DAX Xetra

The DAX has been trending lower since the middle of June as a string of lower highs and lower lows has unwound the market by over 1000 ticks. A rally in the past few days from the low posted on Tuesday at 11,869 threatens a recovery back to the downtrend which comes in today at 12,134. However the bulls do not look to be in control of the recovery, with the daily candlesticks of each of the past couple of day’s gains showing negative real bodies. This suggests that the bulls have lost impetus following early session gains. With today’s open again higher and also back towards the downtrend, is this just another rally that will be sold into? The medium to longer term configuration of the momentum indicators suggests that rallies remain a chance to sell. The hourly chart also reflects this with the rebound losing steam late into yesterday’s session, whilst the hourly RSI again has failed around 60 with the Stochastics topping out and MACD lines back to neutral suggests this is a chance to sell. It is also interesting to see the market failing around an old key support around 12,100, a level around which is being tested again this morning.

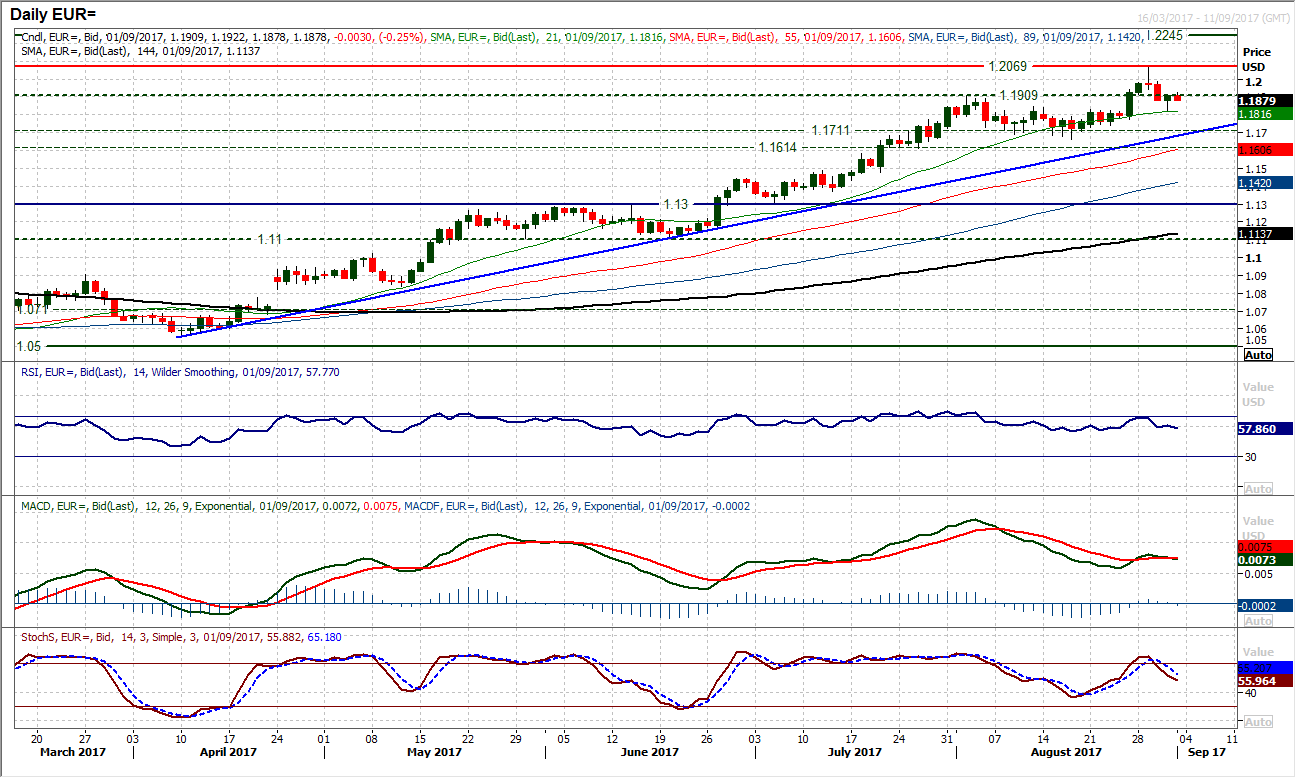

EUR/USD

The renewed weakness of the dollar yesterday pulled the pair back higher again and now the market is back to a near term crossroads again. This comes ahead of Non-farm Payrolls today, which is likely to mean little real direction until 1330BST. With a marginally positive candle yesterday, the pair has rallied back to the resistance around the $1.1909 high from early August. The daily momentum indicators are medium term positively configured (to reflect the continued buying into weakness of the uptrend) but near term are looking somewhat mixed. This mixed outlook moving into payrolls is reflected in the hourly chart where yesterday’s rally has rolled over to leave resistance this morning at $1.1922. Support from yesterday’s low is at $1.1820. Undoubtedly, payrolls will dive the near term reaction and a strong report could pull the market deep into the support around $1.1700/$1.1800. The key resistance remains this week’s high at $1.2070.

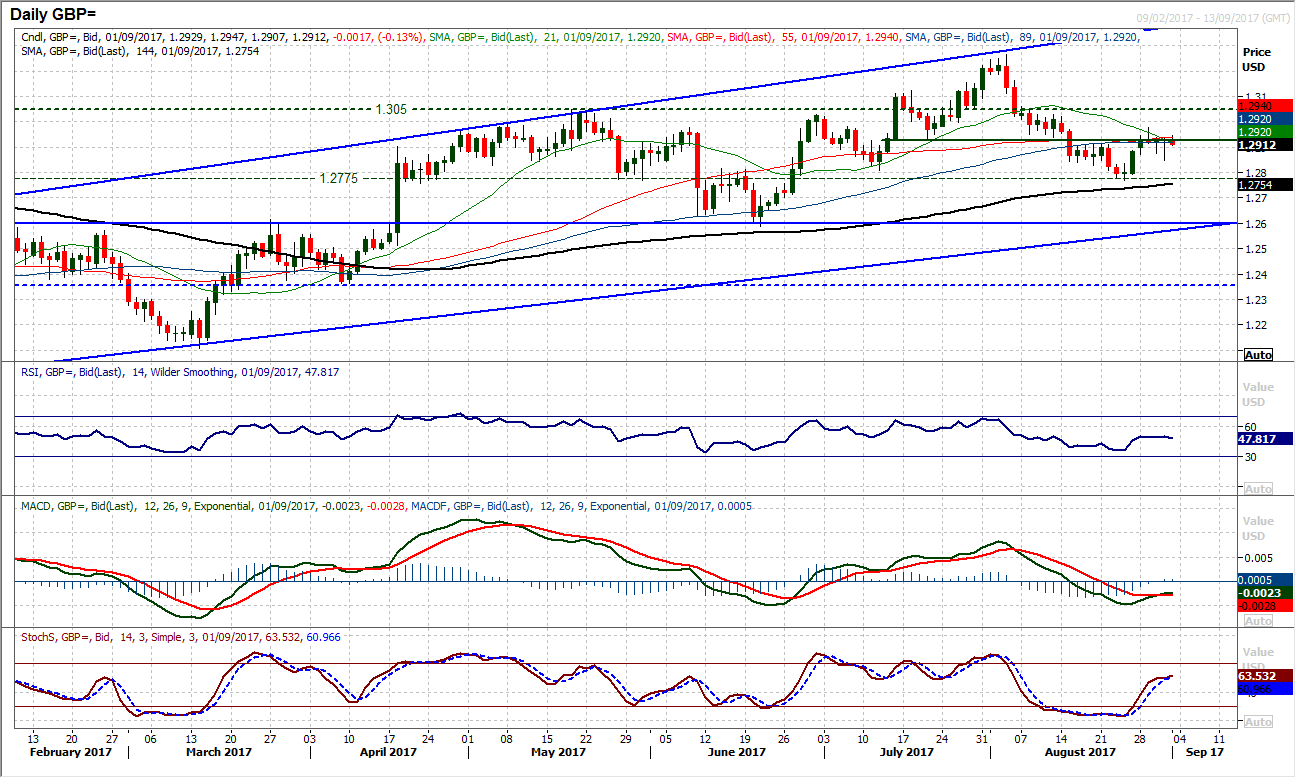

GBP/USD

Despite early intraday weakness, the market recovered yesterday to post yet another small bodied candle around the neckline resistance at $1.2930. This comes with momentum indicators continuing in consolidation mode and little direction on the chart for the bulk of this week. The last couple of candles have longer lower shadows, suggesting the sellers are trying but cannot quite grasp control. There is though little real sign of decisive direction on the hourly chart either, with mixed signals again. With this consolidation, payrolls will be a driver of the near term outlook, with support at $1.2850 and resistance at $1.2978 to watch.

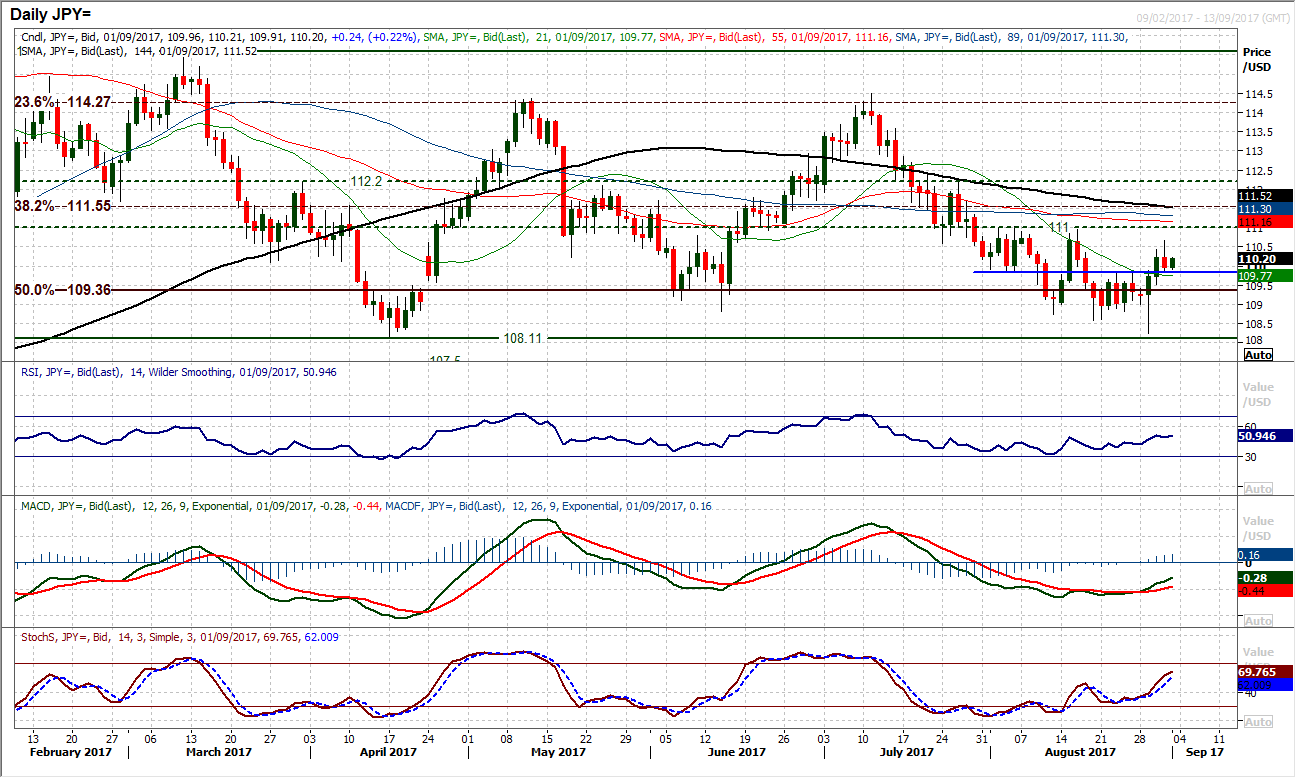

USD/JPY

The pivot around 109.80/109.90 seems to still be a key level to watch as a retracement candle has just kept the recovery in check. The run of strong recovery candles has been stunted however the bulls will see this as a potential opportunity. The recovery in the momentum continues, with the MACD and Stochastics lines tracking higher. The pivot held for yesterday’s low and continues to hold today, whilst the move in the wake of payrolls will be key for the near term outlook. A continuation of the support will likely encourage buying pressure to continue higher in the coming days. The hourly chart shows the market back to levels where the buyers tend to resume. There is further support at 109.40 and 109.00, whilst the bulls will need to break yesterday’s high at 110.65 to open a test of the key resistance at 111.00. A strong payrolls report could be te catalyst the bulls need.

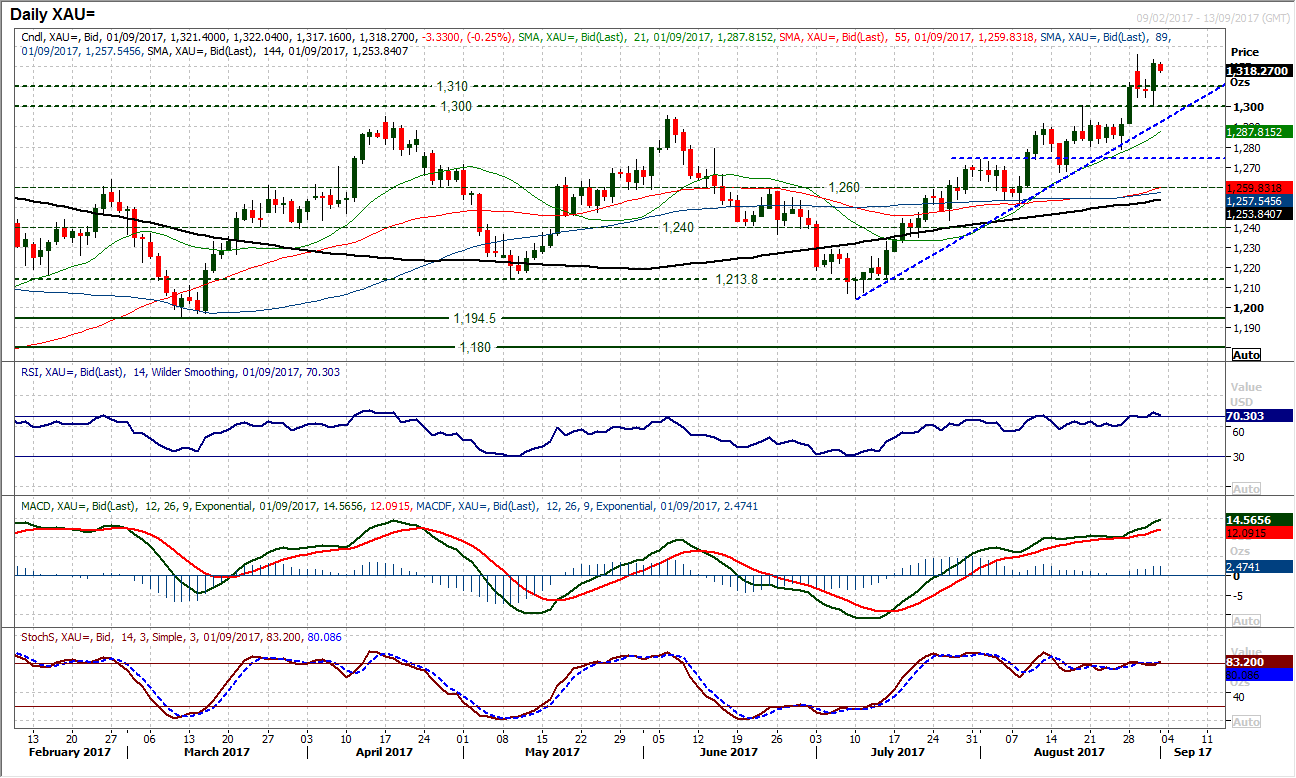

Gold

I have talked previously about the technical strength of gold that was holding up the price (all whilst another safe haven play, the yen, has been wilting). This technical strength continued yesterday, with a strong bullish engulfing candle that has pulled gold to its highest close since September 2016. The strong bull candle has also bolstered the support of the key $1300 level. The 7 week uptrend is firmly intact, along with strong momentum indicators. There is a degree of consolidation which has seen the gold price drift a touch lower today in front of payrolls, and this is leaving resistance at $1326.00 for now. Near term direction will be driven by payrolls but it would take an unambiguously strong report for the market to not only retreat below $1300 but also break the uptrend which today comes in around $1292. Above $1226 the next resistance is the $1337.40 resistance from November’s spike high.

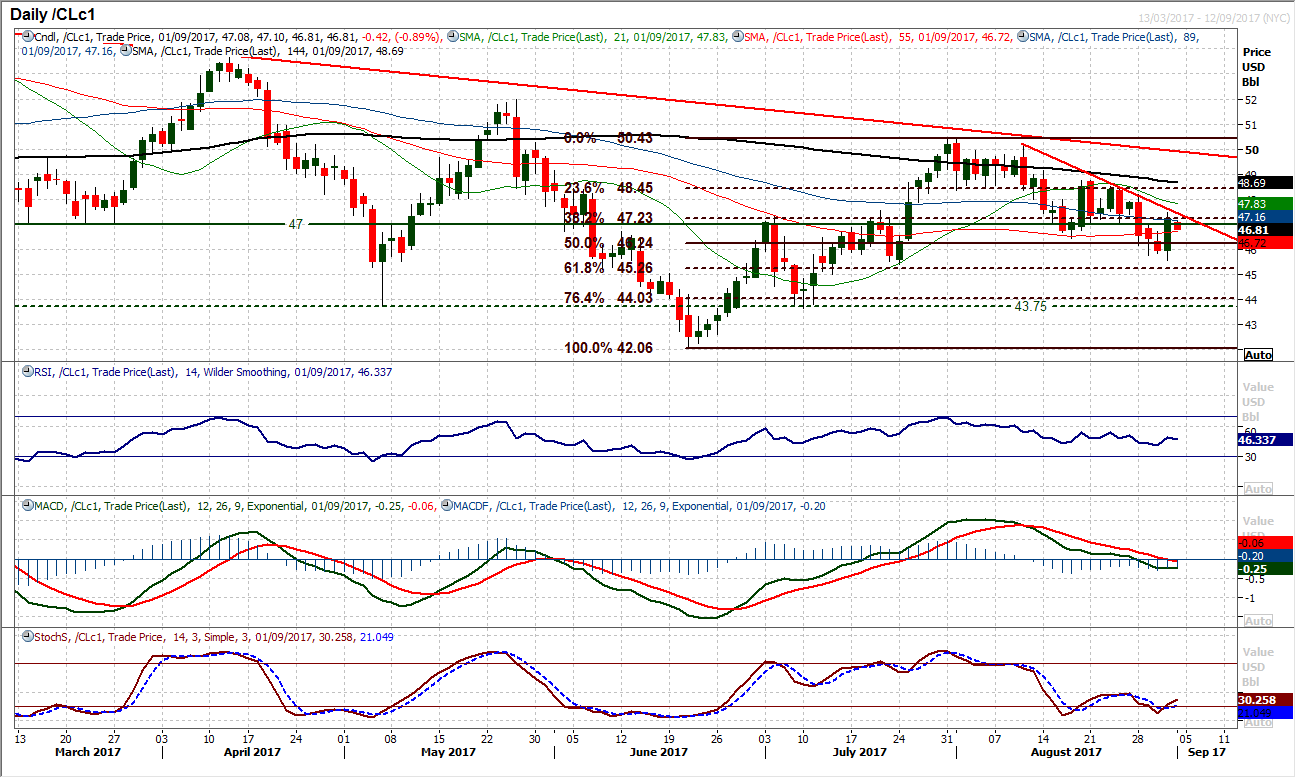

WTI Oil

With the horrendous weather throughout the Gulf of Mexico there will be elevated volatility on oil markets with the region so key to the supply and refinery of oil. Yesterday’s sharp one day rally has looked to improve the outlook once more but the trend of the past few weeks has been negative and for now the move is simply a rebound within the run of lower highs. The market is back into the resistance band around $47.00 with the 38.2% Fibonacci retracement of $42.05/$50.43 coming in at $47.23 as an old basis of support that is now resistance. The market has subsequently started to drift back lower again. The downtrend comes in today at $47.45 and how the bulls react in today’s session will be key to the near term outlook. The big bullish engulfing candlestick pattern (bull key one day reversal) improves the sentiment, with the momentum indicators ticking higher. However the bulls need to do more to convince. Yesterday’s high of $47.47 becomes a key level of confirmation of the rebound now.

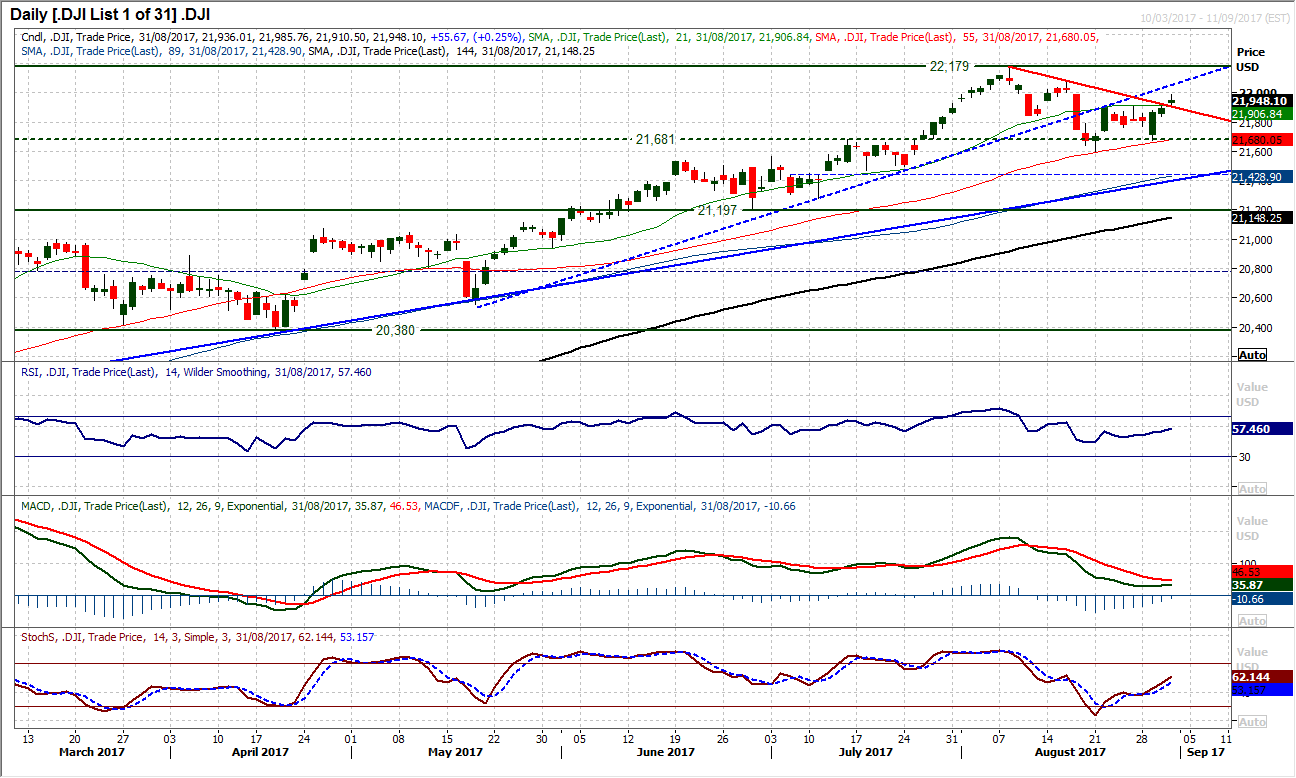

Dow Jones Industrial Average

The bulls continue to run the market recovery higher and have now broken a trend of lower highs that has been forming over the past few weeks. A third consecutive positive candle has taken the market above the near term resistance at 21,913 which is around a confluence of technical barriers that have now been taken out. The bulls now need to hold on to the break of the trend but also now build a new basis of support as a higher low above the low from earlier this week at 21,673. The momentum indicators are backing the recovery with the Stochastics tracking higher and the RSI rising back above 50. Furthermore, the MACD lines look to be bottoming as the momentum indicators collectively look to be improving now. The hourly chart reflects this improvement and the move above the 38.2% Fibonacci retracement at 21,913 now becomes supportive and opens upside above 22,000 once more. Next key resistance is 22,085.

Author

Richard Perry

Independent Analyst