Dipping dots — The monetary policy of the future

Summary

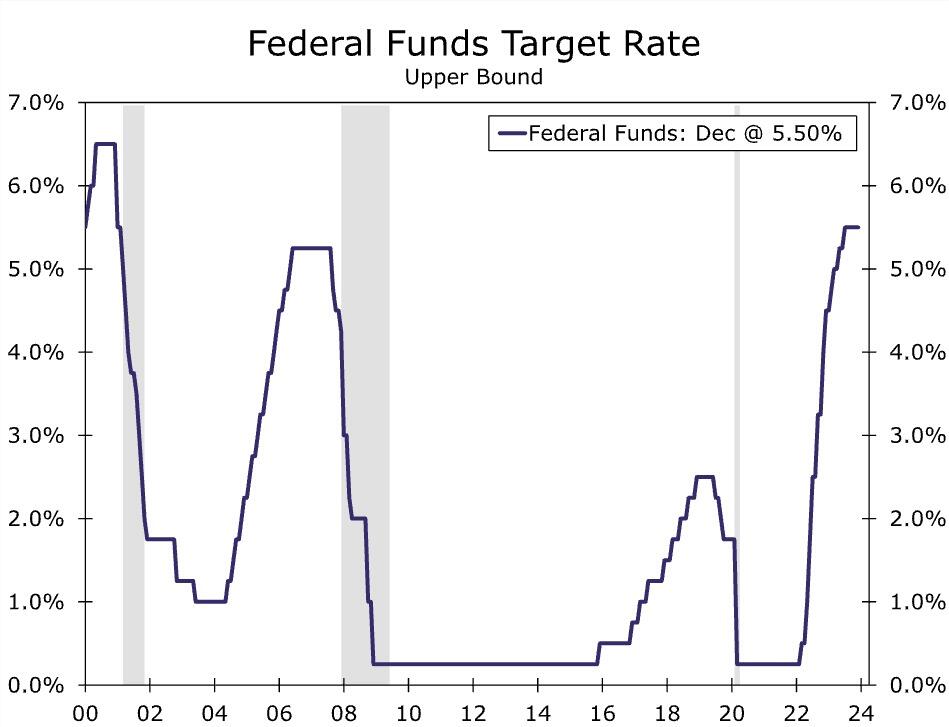

The doves won the day at the last FOMC meeting of 2023. The Federal Reserve left its policy rate unchanged at its December 12-13 meeting, a move that was widely anticipated. More important were the changes to the post-meeting statement and the latest Summary of Economic Projections (SEP). The new statement noted that inflation "has eased" over the past year, although still being elevated. The door was left ajar for additional tightening, but the "dot plot" signals that this was not the base case for most participants. The median projection in the dot plot called for 75 bps of easing in 2024 followed by another 100 bps of rate cuts in 2025. A more benign inflation outlook explains why the dots were revised lower for the first time since June 2020.

The job is not yet finished on the inflation fight, and the Committee will need to see additional data to confirm that the recent deceleration in prices is firmly entrenched. That said, the trend appears to be in place, and we expect the incoming data to confirm that inflation is gradually returning to 2%. After a period of nearly two years of rapid monetary policy tightening, a pivot to cuts next year seems like the most probable outcome. We expect the first rate cut of the easing cycle to occur at the June FOMC meeting.

A more dovish outlook from the FOMC heading into 2024

As was widely expected, the FOMC left the fed funds target range unchanged at 5.25-5.50% in a unanimous decision by the 12 voting members at the conclusion of its meeting today. Having last raised the fed funds rate at the Committee's July meeting, the decision to leave the policy rate at its current setting marked the third consecutive hold. Along with a somewhat more dovish statement and rate projections, today's meeting delivered the Fed's clearest message yet that the torrid hiking cycle that began in March of last year has, in all likelihood, come to an end.

With inflation still too high and the Committee committed to bringing it down to 2%, the FOMC did not fully close the door to additional policy tightening today. The post meeting statement noted that it would continue to take into account the cumulative amount of tightening undertaken, policy lags, and economic and financial conditions when determining "additional policy firming." This phrasing suggests to us that, in the near term, the Committee's bias for future policy adjustments remains toward higher rather than lower. That message was reiterated by Chair Powell in the post-meeting press conference when he stated that the policy rate is "likely at or near its peak" and that the FOMC is "prepared to tighten policy further, if appropriate."

Yet, tweaks to the statement indicated that while further tightening remains possible, it is growing less probable. The FOMC seemed less convinced an additional hike would be necessary, noting that it was determining "the extent of any additional policy firming" rather than "the extent of additional firming" (emphasis ours). Powell confirmed in the press conference that the Committee discussed the process of bringing down rates at the meeting, in another sign that the balance of risks to the Fed's next move is shifting away from a hike and toward eventual cuts.

The more dovish guidance comes as the FOMC seems a bit more encouraged by inflation's progress back toward 2%. Core PCE inflation has slowed to a 2.4% annualized pace over the past three months, suggesting the year-over-year rate has further to fall in the coming months (chart). In the FOMC's assessment of current economic conditions, it noted that inflation "has eased over the past year" even as it continues to recognize that inflation "remains elevated." The only other adjustment to the statement was a slight downgrade to recent economic growth, noting it had slowed from its strong pace in the third quarter.

Source: Federal Reserve Board and Wells Fargo Economics

Author

Wells Fargo Research Team

Wells Fargo