DAX soars to 5-month high as investors expecting more doves from Fed

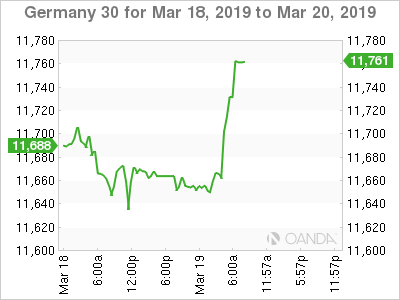

The DAX has posted sharp gains in the Tuesday session. Currently, the DAX is at 11,759, up 0.88% on the day. The index is at its highest level since early October. Car maker shares are showing sharp gains, boosting the DAX on Tuesday. Daimler has soared 3.5%, while BMW and Volkswagen have both climbed 1.8%.

In economic news, German ZEW Economic Sentiment remained in negative territory, but improved to -3.6 points. This easily beat the estimate of -11.0 points. The eurozone event showed a similar trend, improving to -2.5 points. This beat the forecast and was the highest reading since May. On Tuesday, Germany releases PPI and the Federal Reserve issues its monthly rate statement.

With a dearth of fundamentals early in the week, for most of the week, investors will have plenty of time to analyze the Federal Reserve meeting on Wednesday. The Fed is widely expected to maintain the benchmark rate at a range between 2.25 – 2.50 percent. However, investors will have more on their mind than just interest rate levels. The Fed has been sending a dovish message to the markets, and this stance is expected to continue in the March rate statement. The Fed’s balance sheet will also be under scrutiny, with the policymakers expected to announce when they will stop reducing the $4 billion balance sheet. The Fed has been reducing assets by $50 billion a month, but there has been criticism that this tightening is choking economic growth. The Fed will also publish its new dot plot, which is used to convey its interest rate outlook.

The ECB is also in a dovish mode, as the economic slowdown continues to weigh on the eurozone. Inflation climbed slightly in February to 1.5% year-on-year, but remains well below the ECB target of 2 percent. Low inflation means there is no pressure on the bank to raise rates in the near future. At the March policy meeting, policymakers delayed a rate hike to 2020 at the earliest, and this sent the euro to lower levels. The bank also lowered its inflation forecast for 2019 to 1.2%, down from the previous forecast of 1.6%.

Commodities Weekly: Crude oil at four-month high as OPEC sticks to plan

More Brexit Twists as 10 Day Countdown Commences

Economic Calendar

Tuesday (March 19)

-

6:00 German ZEW Economic Sentiment. Estimate -11.0. Actual -3.6

-

6:00 Eurozone ZEW Economic Sentiment. Estimate -15.1. Actual -2.5

Wednesday (March 20)

-

3:00 German PPI. Estimate 0.2%

-

14:00 US FOMC Economic Projections

-

14:00 US FOMC Statement

-

14:00 US Federal Funds Rate. Estimate <2.50%

-

14:00 US FOMC Press Conference

Previous Close: 11,657 Open: 11,668 Low: 11,651 High: 11,759 Close: 11,764

Author

Kenny Fisher

MarketPulse

A highly experienced financial market analyst with a focus on fundamental analysis, Kenneth Fisher’s daily commentary covers a broad range of markets including forex, equities and commodities.