Croatia joining 'A' rating club

Domestic demand driving GDP growth.

ECB: next interest rate cut in October.

S&P delivering anticipated rating upgrade.

Weaker dollar expected.

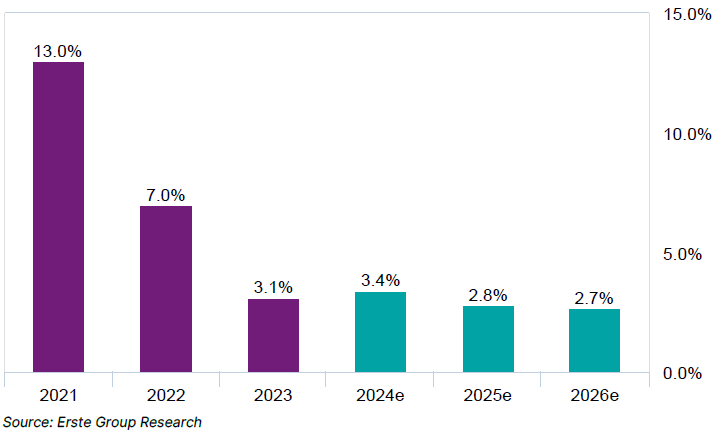

GDP remained in solid gear in 2Q24, adding 3.3% y/y and 0.8% q/q s.a. Domestic demand continued to push strongly, with private consumption adding 6.1% y/y and investments maintaining double-digit growth (12.9% y/y), while net exports remained a drag. Going forward, domestic demand is anticipated to maintain supportive momentum, reflecting strong labor market fundamentals on the consumption side and EU fund backing on the investment side. Exports should deliver a steady tourism footprint, but weak EU growth keeps weighing on a stronger goods export recovery. We maintain our FY24 call at 3.4%, with risks tilted modestly to the downside.

Inflation kept a moderating trend amid supportive supply-side factors. Demand-side pressure continues, fueling above-EU average inflation, with the average CPI in 2024 landing close to 3%. The budget gap is expected to slip to 2.5% of GDP in 2024, reflecting pre-election generosity. In anticipation of the 2025 budget, a stronger consolidation effort seems unlikely at present. S&P delivered a strong message with a rating upgrade to ‘A-‘ and even more so with the outlook remaining unchanged at positive. The latter signals an increasing likelihood of another upgrade in the 1-2 year horizon. Fitch and Moody’s are likely to act in a similar fashion.

GDP (real,y/y)

Author

Erste Bank Research Team

Erste Bank

At Erste Group we greatly value transparency. Our Investor Relations team strives to provide comprehensive information with frequent updates to ensure that the details on these pages are always current.