Confidence dive hits Czech industry

Czech consumer and business confidence both weakened in December. Consumers are now less optimistic about the economic outlook and the business mood was further dragged down by industry. Meanwhile, the service sector saw further improvements.

Consumer mood remains above the long-term average

The Czech consumer confidence indicator shed 1.2 points to 100.4 in December, remaining just above its long-term average. The business confidence indicator decreased by 0.4 points to 96.9 in the same month, with the country's underperforming industry proving the main drag. Both indicators came in below market expectations.

The share of consumers expecting the overall economic situation in Czechia to worsen over the next 12 months has increased slightly, and the proportion of consumers who believe that the current period is not appropriate for large purchases has increased. In contrast, the number of households assessing their current financial situation as worse than in the previous year fell slightly.

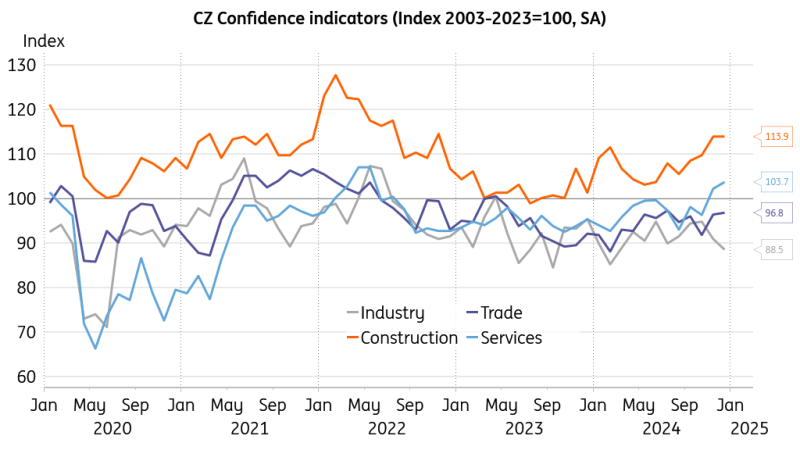

When looking at the business domain, confidence picked up again in the service sector (+1.5 points) and slightly in trade (+0.4 points). Meanwhile, the mood in industry dropped by 2.4 points to 88.5 in December, setting a clear downward trend. Confidence in the construction sector remained unchanged at an elevated level, reflecting the recent upswing in demand for residential property.

Services continue to gain; the industry loses out

Source: CZSO, Macrobond

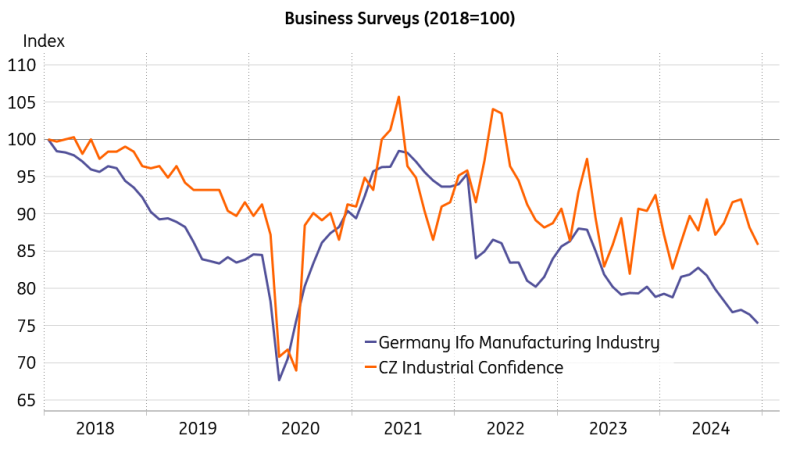

Overall, the December survey corrected the previous month's uptick for both consumers and businesses. Consumers expressed increased concerns about the economic outlook. The lousy mood in industry relates to the havoc in the European automotive sector and the continued industrial misery in Germany. Indeed, these are challenging conditions for the future performance of the Czech economy. Meanwhile, service providers see better times ahead, which may foster price inertia in this segment.

No fundamental turnaround in sight

The dichotomy between a well-performing consumer and an underperforming industry is set to continue. With Czech industry closely linked to that of Germany, this recent weakness is likely to persist given that barriers to Europe's economic performance are predominately of a structural nature. It seems that leaders in Europe do not perceive such a peculiar situation as a pressing issue, and we've seen quite some resistance to the adoption of growth-oriented adjustments to regulations, policies, and investment incentives.

For now, no fundamental turnaround in industry can be seen on the horizon. We're reminded of the maxim pereat mundus, fiat reglamentum – let the world perish but preserve the regulations. A tough choice, perhaps.

Where does it stop?

Source: Macrobond

Read the original analysis: Confidence dive hits czech industry

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.