CNB preview: The need for less restrictive monetary policy builds

Reducing policy rates has become fashionable, and the CNB will likely not want to fall behind with another soft cut. Doubts about the strength of the economic rebound and a deteriorating foreign environment call for continued easing, while elevated core inflation amid stubborn price dynamics in the service sector still warrants some caution.

Softening economic outlook requires lower rates

Everybody is factoring in a softer Czech recovery for the year’s second half due to the worsening situation in manufacturing and the subdued performance of the main trading partners. The Czech National Bank will not release a new forecast at this time, yet the deteriorating economic outlook since the summer is obvious and will factor into the decision function of the Bank Board. Economic developments in Germany have come in well below the CNB's expectation in terms of foreign demand and support for Czech exports, although the situation in some other eurozone countries is not that hopeless. That said, the dichotomy between the nonperforming supply side, represented by declining industrial output, and the reasonably well-performing demand side, measured by a lofty dynamic in real retail sales, has become even more prominent in recent months.

Real retail sales gained 4.5% in July, just below the historical average of 4.7% recorded during times of robust economic expansion between 2016 and 2019, confirming that the Czech consumer entered the second half of the year in good spirits. Spenders are benefiting from continued solid nominal wage growth of 6.5%, which was recorded in the first quarter, or 3.9% after adjusting for inflation. Both figures came in below the CNB expectations, so this seems like rather reassuring news for future price pressures. However, over the past decade, the long-term average real wage growth in Czechia has been 1.7% annually. Excluding the period of significant reduction in real purchasing power from late 2021 to 2023, this average rises to 4%. The recent real wage increase will still provide enough juice to propel household spending in the months ahead and perhaps foster pricing in the service sector. The continued tightness in the labour market is another factor to consider, especially regarding the segment of skilled workers.

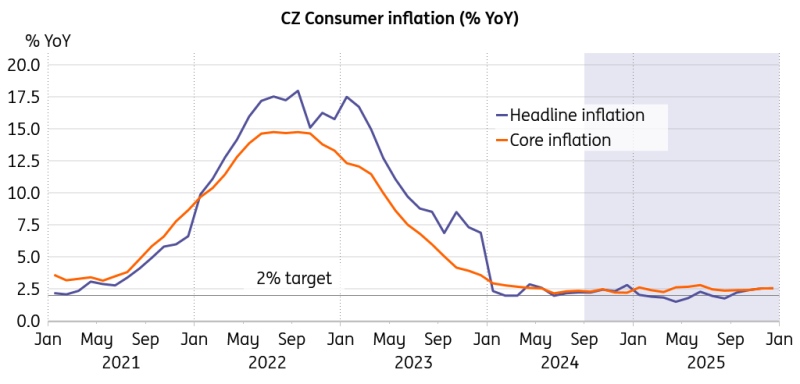

Core inflation to remain elevated

CNB, ING, Macrobond

Annual headline inflation remained at 2.2% in August, which is 0.4pp above the CNB Summer forecast, while core inflation picked up to 2.4%, coming in 0.2pp above the central bank's expectation in the same month. Persistent price growth in the service sector is the main driver of core inflation. It seems that the service sector switched from a relatively low-inflation environment to a persistently higher-inflation environment, with the transition from the latter regime to the former not being linear and subject to additional effort. We see the core rate staying in the upper bound tier of the CNB confidence band throughout the next year, though the expected economic growth of 2.1% is not extraordinary. So, the pricing in the service sector and core inflation will remain the writing on the wall over the coming quarters, especially should the recovery gain some steam mid-next year.

Overall, reasons for a less restrictive monetary policy stance have clearly accumulated and hold the upper hand, as the softening economic outlook calls for some support. On the other hand, quickening core inflation and persistently strong pricing in the service sector, supported by still robust wage growth, require some caution. In such a situation, a 25bp rate reduction represents our base case scenario for the coming meeting.

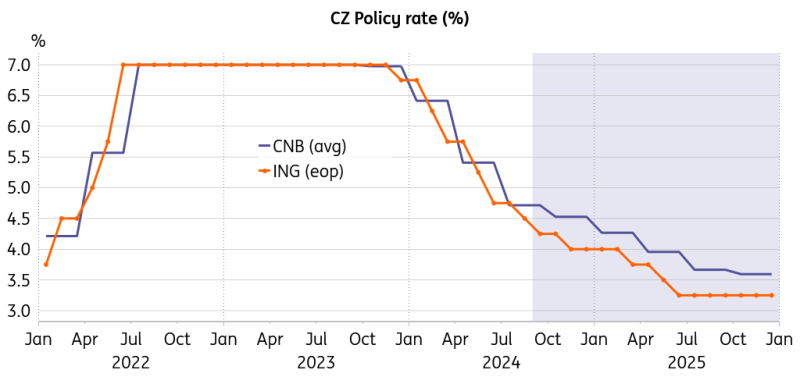

Scope for rates reduction has increased

CNB, ING, Macrobond

To pause in December or not to pause?

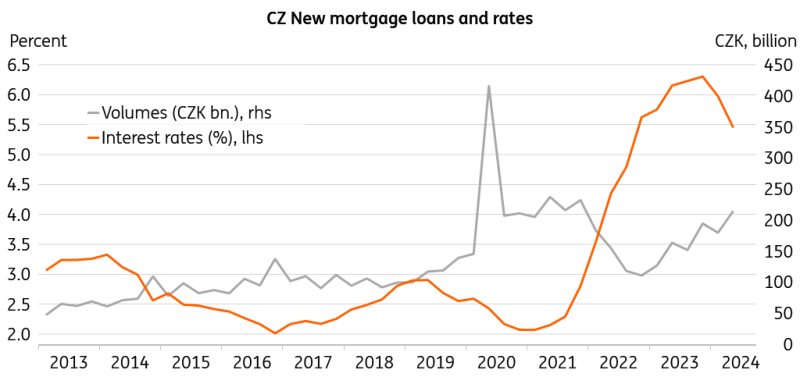

We see a 4% policy rate as the terminal rate for this year, with another soft cut to follow in November. A pause in December is still likely in our view unless things turn ugly in manufacturing over the rest of the year. Household credit activity has revived, with volumes of new mortgages trending upward for some time despite the still-elevated borrowing costs. Banks are lowering interest rates for households only gradually, which is a setback for the transmission of monetary policy. However, residential prices already started to recover at the beginning of this year and may affect rent-related items within the consumer basket over the coming months. An increase in market and imputed rents would be recorded as a spike in core inflation in January, so we believe that policymakers will prefer to wait a bit rather than risk a surprise by a pronounced increase in housing costs at the start of the year.

New mortgage loans trend upward

Macrobond

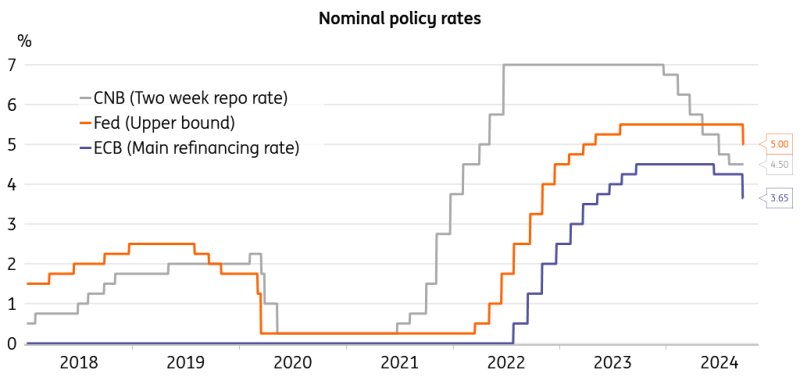

Base effects will drive headline inflation higher from November onward, and there is some risk that it will get close to 3% in the December reading. That said, announced cuts to end prices of electricity and natural gas are set to bring regulated prices down at the beginning of next year, pushing headline inflation back to the target. Meanwhile, core inflation is set to remain elevated, so policymakers will have to decide amid contrasting conditions. The Bank Board will also take into account the lower policy rates abroad, as the European Central Bank continues in the cutting cycle and the Federal Reserve has just embarked on its easing cycle with a bold move. A hawkish stance from the CNB will likely lend support to the Czech koruna and keep imported inflation at bay. The scope for further easing in monetary policy conditions will prevail, so we expect the cutting cycle to carry on in early spring to bring the policy rate to 3.25% by mid-next year amid a continued economic rebound.

Everyone down with rates

Macrobond

The German recovery question and potential for decoupling

Economic recovery became the leading topic, as inflation has been tamed and is close to target. That said, the performance of the German economy is a critical issue for Czech industry, as it is significantly export-oriented, and a substantial part of the domestic businesses is owned or invested heavily from the side of the German capital. Some of the firms are direct suppliers to the German automotive sector, which is under pressure from mounting regulation and too much red tape on one end and skyrocketing competition from China on the other. Whether the German economy will be able to rise from the ashes is a crucial question for Czech industry, despite the increasing tendency to reach out to new markets in the US and Asia directly.

As the stagnation has dragged on for too long on the German side, there are signs of Czech industry partially decoupling from its limping neighbour. It also seems essential for the future development of the Czech export engine, and we will closely watch whether such an effort bears fruit. In an adverse scenario, the structural issues and setbacks to the German economic model may result in a long-term downward shift in the business cycle in the sense that the upswings become stagnations and downswings outright recessions. At the same time, the chancellor, Olaf Scholz, has appeared relatively unperturbed even after his party's failure in the recent regional election. A bold call for a revamp in economic strategy does not seem to be in sight, which only strengthens incentives for the Czech industrial sector to decouple further, even though it is a challenging task achievable only to a certain extent in the medium term.

Read the original analysis: CNB preview: The need for less restrictive monetary policy builds

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.