CNB minutes show a gradual rebound as inflationary risks persist

All Czech National Bank board members but one voted for a soft cut, perceiving some inflationary risks as still relevant to consider when maintaining a cautious approach to rate reductions. Mounting challenges to global growth represent a clear risk to the Czech economic rebound, bolstering the case for further easing.

Potential price pressures warrant a cautious approach to easing

The CNB reduced rates another 25bp to 4.25% in late September, with all but one board member voting in favour. Tomas Holub voted for a 50bp rate cut, seeing the monetary policy-relevant inflation below target and the economy operating below its potential. Overall, the Board assessed the risks and uncertainties to the outlook as broadly balanced. The governor, Ales Michl, stated that inflation had been higher in recent months than the CNB and financial markets had expected. The fight against inflation doesn't appear to be entirely over, so it is necessary to only reduce interest rates gradually.

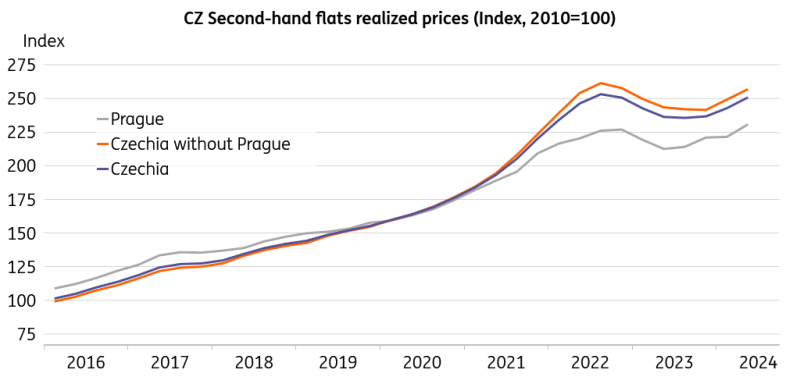

Residential prices started to recover

Source: CZSO, Macrobond

Most of the inflationary risks identified at the August meeting were assessed by the majority of the Bank Board as being unrelenting. Those are predominantly linked to persistent price growth in the service sector and the continued tightness in the labour market. The renewed rise in real estate prices and its potential impact on both market and imputed rents is to be taken seriously when it comes upward to inflation pressures. An unexpected increase in the fiscal deficit also represents the potential for upward price pressures, as stressed by the central bank's governor.

Deteriorating growth outlook abroad is a drag

On the contrary, the deterioration of global economic conditions and the weaker performance of the German economy were identified as significant anti-inflationary risks. The subdued foreign demand from main European trading partners reflects a combination of cyclical and structural factors, which could warrant more pronounced monetary policy easing from the European Central Bank.

With respect to a cautious approach towards monetary easing, most of the Board members see inflationary pressures as still being rooted in the economy. Jan Prochazka added that maintaining positive real interest rates would contribute to pressure on higher productivity and limit the passthrough of rising labour costs to consumer prices. Some members admitted that the easing process may be interrupted in future meetings as the interest rate approaches the long-term neutral value. Eva Zamrazilova reiterated that she perceives the possible undershooting of the inflation target to be a less serious problem than overshooting.

In contrast, Tomas Holub assessed the medium-term risks as slightly anti-inflationary amid the country's gradual economic rebound and the backdrop of a worsening global outlook. He showed a preference for easing monetary policy conditions to a larger extent, a view that resonated with the medium-term considerations of Jan Frait – although he opted for the milder reduction, due to the potential pressure on a weaker exchange rate once financial markets could reassess the long-term growth potential of the Czech economy.

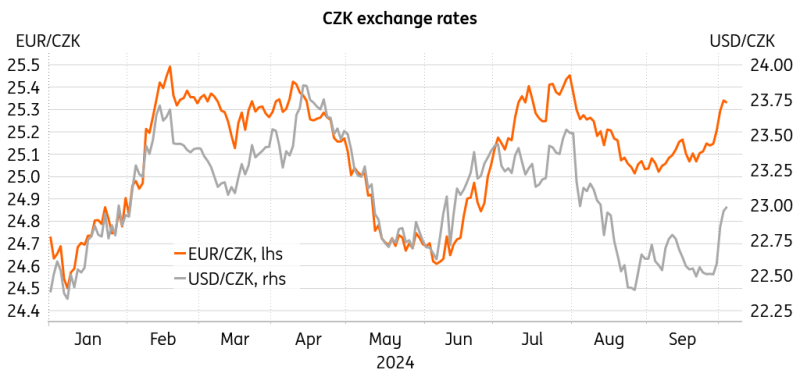

Koruna came under pressure recently

Source: Macrobond

Wait and see, or hit and run?

We still see the risks for elevated core inflation as relevant, especially due to persistent price dynamics in the service sector. The price growth of non-tradeable items, excluding regulated prices, increased to 4.4% in August, interrupting the previous slowdown. The potential for a hike in market and imputed rents would likely manifest itself mainly at the beginning of the next year, following the historical pattern.

Overall, we expect the bank board to reduce rates by 0.25pp at its November meeting to 4%, followed by a pause to consider the state of consumer prices in January. The real interest rate could go down to only 1% in December if headline inflation picks up to 3% as per our projections. Still, the pause in December is a close call, especially if the economic recovery comes under more pressure. If January’s inflation reading shows no ugly surprises, rate cuts should be set to resume at a soft pace early next spring, bringing the policy rate to 3.25% by mid-year.

Read the original analysis: CNB minutes show a gradual rebound as inflationary risks persist

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.