China’s no longer to set to beat US GDP by 2030 as challenges mount

Nearly half of the world’s GDP comes from China and the US combined. China has overtaken the eurozone as the world’s number two largest GDP contributor behind the US. Having had years of double-digit growth analysts were expecting China to overtake the USA’s GDP contribution as early as 2030. However, the recent slower growth path that China has taken due to its weak post-covid rebound has had Bloomberg economists extend the time it could take China to catch up with the US.

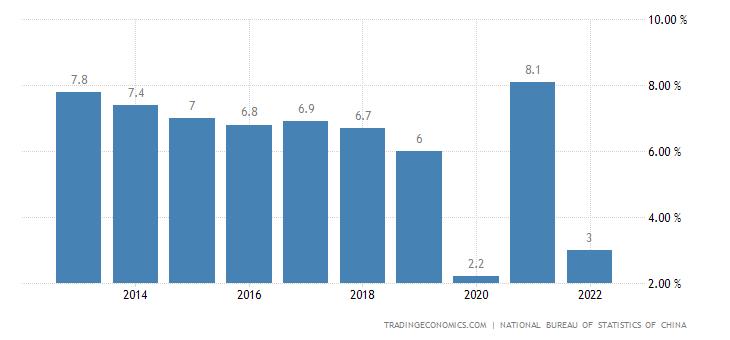

Bloomberg economists now see the mid-2040s as the time it will take China to overtake the US. Concerns over China’s property market and increasing worries about Beijing’s management of China’s economy means Bloomberg economists now sees growth slowing to 3 1/2% in 2030 to around only 1% by 2050. Those projections are revised down from the growth of 4.3% in 2030 and 1.6% in 2050. These downward revisions reflect the slower rate of China’s economic growth which has expanded by just 3% last year, which is one of its lowest rates of growth in decades.

Furthermore, the Covid recovery that was expected has not materialised. Export levels have fallen and difficulties in the property sector have become more entrenched. This has resulted in a flurry of downwardly graded growth forecasts for 2024 from analysts at major banks.

So, this is prompting the question as to whether China has reached its peak. Some long-term challenges for China include a population drop last year, regulatory crackdowns, and geopolitical tensions with the US and other Western governments, particularly over Taiwan, raising concerns about China’s ongoing growth prospects.

What does this mean?

Well, it means China’s growth is going to be in increasing focus over the next few months. Can Beijing overcome its structural issues? Will the property market worries spill over into bank worries? Will there now be a more comprehensive support package for China post-Covid? Keep a careful eye on Beijing’s response as it could offer opportunities for medium-term buys into China’s economy if it takes steps to turn around these latest growth headwinds.

-638296699261466506.png)

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.