![]() ING Global Economics Team

ING Global Economics Team

ING Economic and Financial Analysis

China’s property prices saw a smaller decline and retail sales bounced to an eight-month high, while fixed asset investment and value added of industry growth remained stable on the month.

Housing prices showed some signs of stabilisation

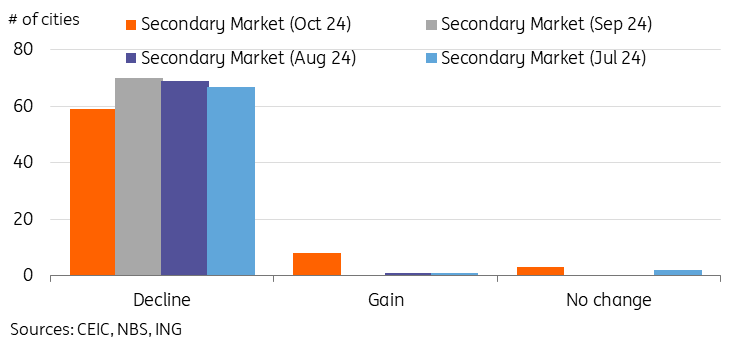

The National Bureau of Statistics kicked off the day of data releases in China with October's 70-city property prices still in decline but showing signs of improvement. New home prices fell by -0.51% month-on-month, up from -0.71% MoM in September, while secondary home prices fell by -0.48% versus a -0.93% MoM move the prior month. The rate of the decline was the smallest since March for new home prices, and the smallest since September 2023 for the secondary market.

An encouraging sign was that 11 of the 70 cities saw secondary market prices stabilise or increase, which was far and away the best read of the year. Among these 11 cities, Beijing (1.0%), Shanghai (0.2%), Shenzhen (0.7%) all saw prices move higher in the month, with Guangzhou (-0.4%) the only Tier 1 city with prices continuing to fall. In our previous reports we have often stated that the stabilisation in property prices will start from the core, and October's data is a good sign this could be starting to play out – though we still need to see more data to confirm this trend. 7 of 70 cities also saw new home prices rise, which was the best read since March.

October's data was the first full month of data since September's rate cuts, and combined with continued city-level policy support, the early signs are encouraging. With an expected ramp up of unsold home purchases in the coming months and a continued policy focus on halting the decline of the property market, the October data release showed that there is hope of seeing prices gradually bottom out in the coming months.

Property investment unsurprisingly remained weak, slipping to -10.3% year-on-year (year-to-date). Base effects aside, we do not expect a substantive recovery of property investment until prices stabilise and housing inventories normalise. This process is still expected to be lengthy.

Eleven cities saw secondary market prices stabilising or increasing in October, the best read of the year

Retail Sales bounced back to eight-month high

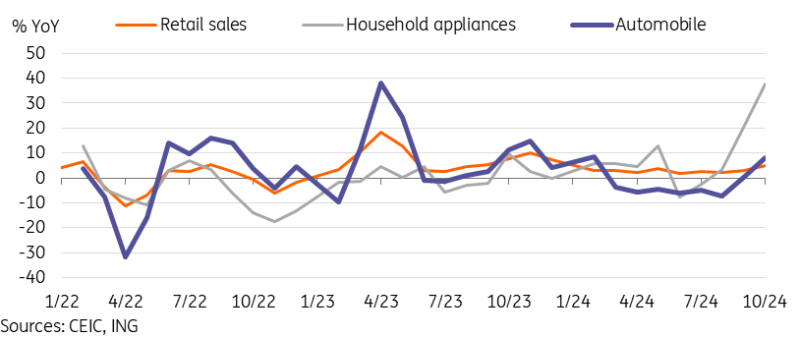

Retail sales rebounded to 4.8% YoY, up from 3.2% YoY – significantly beating market expectations and our forecasts for a milder uptick. The 4.8% YoY read marked the highest level since the combined January-February read of 5.5% YoY, and helped bring the YTD growth of retail sales from 3.3% YoY to 3.5% YoY.

Most categories saw growth move higher on the month. We believe the stronger-than-expected retail sales are primarily illustrating the impact of expanded trade-in policies taking effect. These programmes have been primarily targeting home appliances and autos, and both categories saw an uptick in October, with home appliance sales surging to 39.2% YoY from 20.5% YoY and auto sales also rising to 3.7% YoY from 0.4% YoY. October's data also featured a surprising surge of cosmetics sales, which spiked from -4.5% YoY to to 40.1% YoY after being in negative growth for several months.

Finally, it looks like the a stronger base effect is starting to cut into the "eat, drink, and play" theme which had so far significantly outperformed in the year. Catering (3.2%) and alcohol and tobacco (-0.1%) underperformed the headline for a second consecutive month, though the sports and recreation (26.7%) category continued to significantly outpace headline growth.

It is likely that measures such as the reduced mortgage payments, rate cuts, and consumption vouchers may have contributed to some extent, though the exact impact is hard to gauge.

Retail Sales were buoyed by trade-in policies

Fixed asset investment growth again unchanged

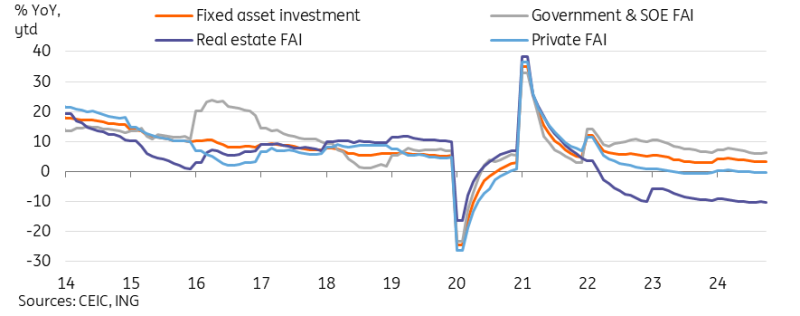

Fixed asset investment remained steady at 3.4% YoY YTD for the third consecutive month, basically in line with expectations. Given the year-to-date nature of the numbers, at this point the changes will be incremental absent any major catalysts, and with the fiscal stimulus rollout unlikely to substantively affect data until next year, what we got was a very stable report.

Public investment edged up 0.1ppt to 6.2% YoY YTD, while private investment further slid 0.1 ppt to -0.3% YoY YTD. Public investment is unlikely to significantly pick up until the measures to alleviate local government debt issues are rolled out and there are more plentiful funds available for pushing out new stimulus measures; this process may take a few months and will most likely be seen in 2025 data. It is likely that actual corporate investment will take time to recover, and will likely await concrete rollout of support policies. Foreign enterprises' FAI continued to fall, down to -20.6% YoY YTD as uncertainty persists.

This year's FAI continues to be led by manufacturing (9.3%) and electricity, heat, gas and water production and supply (24.1%) FAI.

Public investment uptick enough to offset further slowdown in private and real estate investment

Value added of industry growth little changed in October

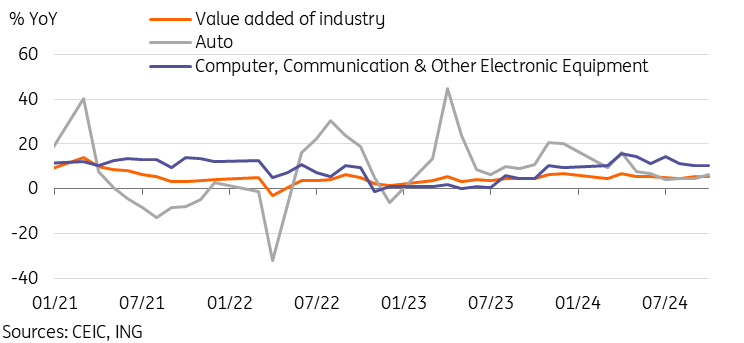

Value added of industry growth edged down slightly to 5.3% YoY from 5.4% YoY. This read was on the disappointing side, as earlier PMI data had signalled a potentially larger recovery of the data, but nonetheless showed growth continuing in a stable range for the last few months.

In terms of the category breakdown, hi-tech manufacturing moderated slightly to 9.4% YoY, down from 10.1% YoY, but continued to outpace headline growth. The computers, communications and other electronic equipment category also remained resilient at 10.5% YoY, down just 0.1 ppt from September. Auto manufacturing growth picked up to 6.2% YoY from 4.6% YoY, benefiting from the recent uptick in both domestic sales and exports. On the other hand, the previously surging category of rail, ships, and aeroplanes slowed to 4.4% YoY from 13.7% YoY.

Overall, China's manufacturing sector could face further headwinds once additional tariffs from the US are introduced. The view from our global research team is that this may not be the case until the third quarter of 2025 at earliest, which means that industrial activity could still hold up decently well through the first half of 2025, with room for upside if support policies boosting domestic demand continue to roll out.

Auto Manufacturing recovery helped stabilise overall industrial activity

October data keeps China on track to reach 2024 growth target

Following on September's upside surprise, October's economic data remained on the encouraging side. Property prices were still in decline overall but the smaller decline and city level data gave hope that a bottoming out could be on the horizon. The activity continued to show further stabilisation of the economy in the first full month after September's monetary policy easing measures, and the 2024 growth target of "around 5%" should be achieved barring any significant surprises in the last two months of the year.

There has been a lot of angst in financial markets on the potential impact of Trump 2.0 on China, and the initial market repsonse to China's fiscal package was one of disappointment. The prospect of a Trade War 2.0, combined with a likely slower and shorter global central bank monetary policy easing, will certainly have a dampening impact on growth. However, considering our house view for a later timing of tariff implementation and our expectations for China to adopt a more "forceful" fiscal policy stance and continued monetary policy easing from the People's Bank of China next year, we are relatively less pessimistic on the 2025 outlook compared to most of the market heading into the home stretch of 2024.

Read the original analysis: China’s economy further stabilised in October, with more stimulus ahead

Content disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/content-disclaimer/

Recommended Content

Editors’ Picks

EUR/USD recovers toward 1.0600 as US Dollar retreats ahead of data

EUR/USD extends the rebound toward 1.0600 in the European session on Friday. The renewed upside is mainly linked to a broad US Dollar pullback as traders look to the topt-tier US Retail Sales data for a fresh impetus. ECB- and Fedspeak also eyed.

GBP/USD holds above 1.2650 after UK data

GBP/USD holds its recovery momentum above 1.2650 in European trading on Friday. The mixed UK GDP and industrial data fail to deter Pound Sterling buyers as the US Dollar rally takes a breather ahead of Retail Sales and Fedspeak.

Gold stabilizes after bouncing off 100-day moving average

Gold trades little changed on Friday, holding steady in the $2,560s after making a slight recovery from the two-month lows reached on the previous day. A stronger US Dollar continues to put pressure on Gold since it is mainly priced and traded in the US currency.

Bitcoin to 100k or pullback to 78k?

Bitcoin and Ethereum showed a modest recovery on Friday following Thursday's downturn, yet momentum indicators suggest continuing the decline as signs of bull exhaustion emerge. Ripple is approaching a key resistance level, with a potential rejection likely leading to a decline ahead.

Trump vs CPI

US CPI for October was exactly in line with expectations. The headline rate of CPI rose to 2.6% YoY from 2.4% YoY in September. The core rate remained steady at 3.3%. The detail of the report shows that the shelter index rose by 0.4% on the month, which accounted for 50% of the increase in all items on a monthly basis.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.