China’s credit activity remained weak in July

New aggregate financing and loans both missed forecasts again in July amid high real interest rates and limited borrowing appetite.

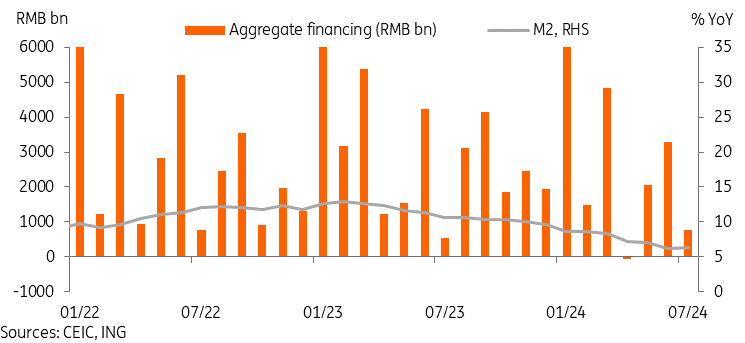

Weak credit activity continued into July

New aggregate financing slowed to RMB 770.8bn in July. This brings the year-to-date new increase of aggregate financing to RMB 18.87tn, which represents a 14.6% year-on-year decline.

Subcategories of aggregate financing were mixed on the month. In general, loan activity was weak in July. New RMB loans fell into contraction at RMB 770.8bn, lowering the year-to-date new increase of RMB loans to RMB 12.38tn, a 20.9% YoY decline. Foreign currency loans were also weak in July, falling RMB 88.9bn to bring the year-to-date level to a decrease of RMB 97bn.

Other categories of financing fared a little better on the month. Corporate bond issuance increased by RMB 202.8bn in July, bringing the year-to-date growth to 23.9% YoY. Though still very low compared to historical levels, equity financing also edged up to RMB 23.1bn in July which marked a six-month high.

Another slight bright spot in today's credit data was M2 growth, which edged up slightly to 6.3% YoY after reaching an all-time low of 6.2% YoY in June, the first monthly increase of the YoY growth level in 17 months.

Aggregate financing continued to disappoint while M2 growth edged up

Rate cut could start to offer a level of support but more needs to be done

Recall that the People's Bank of China surprised markets on 22 July with a 10bp cut to the 7-day reverse repo rate, and then again on 25 July with a cut to the medium-term lending facility (MLF). These rate cuts came too late in the month to substantively affect July's data, so we will wait to see if there is any improvement in the credit activity data in August.

With that said, economic conditions remain well-suited for further monetary policy easing. Inflation saw a slight uptick in July but remains well below the level where it should inhibit rate cuts. Private investment and credit activity remain weak, illustrating that real interest rates remain too high given the current state of the economy and private sector confidence. Finally, RMB depreciation pressure, which we believe impeded earlier easing, has also faded somewhat amid recent expectations for faster US rate cuts.

As such, we continue to expect at least one more rate cut in 2024, with potentially more if global central banks start cutting rates more aggressively than expected, and indeed our house view for US rate cuts was recently revised up to 100bp for the year with a 50bp cut in September. If this scenario plays out, we could see another cut as early as next month in China as well, and another cut in the fourth quarter would be on the table as well. China is expected to ease policy at a slower rate than most global central banks, which should still provide a relatively favourable backdrop for the RMB in the medium term. We recently set our year-end forecast for the USD/CNY pair at 7.10 in light of recent monetary policy developments.

Read the original analysis: China’s credit activity remained weak in July

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.