China’s CPI inflation edges up as non-food inflation raises deflation fears

CPI inflation in China edged higher as food prices turned positive for the first time in 14 months, but non-food inflation shows the effect of a weak property market and consumer confidence.

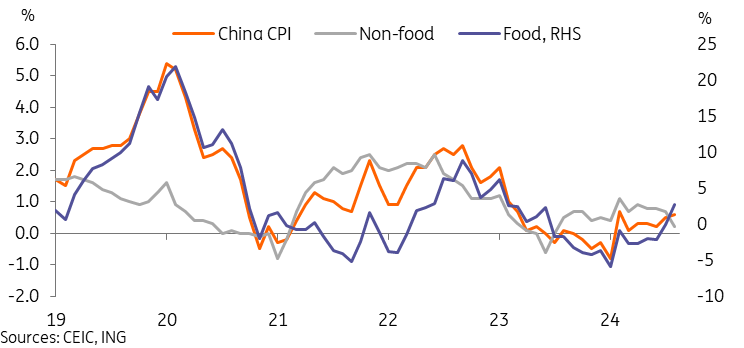

CPI inflation hit six-month high on support from food prices

Inflation edged up in August on food price recovery

August CPI inflation in China rose to 0.6% year-on-year, up from 0.5% YoY in July, coming in exactly in line with our forecasts this month and reaching a six-month high. In month-on-month terms, CPI inflation rose 0.4%, reflecting a 3.4% MoM uptick in food prices and outweighing a -0.3% MoM decline in non-food prices.

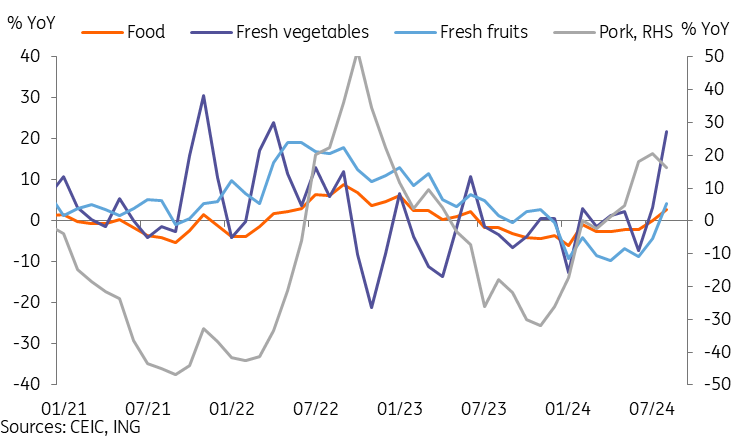

Food prices were the main driver behind the slight uptick in overall inflation, rising 2.8% YoY in August, up from 0.0% YoY in July. Pork (16.1%), fresh vegetable (21.8%), and fresh fruit (4.1%) prices were the main contributors to food inflation, as some other categories such as grains, oils, and dairy remained in negative territory.

August's data marked the first time since June 2023 that food inflation was positive in year-on-year terms, and this momentum should continue in the next few months as well given a supportive base effect.

Pork, vegetable, and fruit prices drove food inflation higher in August

Non-food inflation showed increasing signs of weakness

However, non-food inflation painted a more concerning picture for those worried about deflation. Non-food inflation fell to 0.2% YoY, the lowest level since July 2023, and there is a risk that it could move toward negative levels in the next few months if there are no new stimulus measures to boost consumption activity.

The transportation and communications category was the biggest drag on non-food inflation at -2.7% YoY. Heavy competition in the auto sector continued to lead to deflation in the transportation facility category, which registered at -5.5% YoY in August. Communications facilities also saw a -2.1 % YoY decline amid price competition and limited appetite for smartphone upgrading in an environment of heightened household caution over discretionary spending.

The property market weakness also continued to translate to lower rent prices, which fell -0.3% YoY in August, unchanged from July's level.

Low inflation continues to give ample room for policy easing

Overall, inflation in China remains very much subdued despite the slight uptick over the month. Given the cyclical nature of food prices, non-food prices are likely to be more in focus with regard to the overall inflation outlook, and the data showed that weak consumption momentum is starting to translate into deflationary pressure in various categories.

This means that as far as monetary policy is concerned, the People's Bank of China (PBoC) should have no impediments to further policy easing to help support the economy in the coming months. We expect there will be at least one rate cut before the end of the year, and potentially more if the Federal Reserve cuts rates as aggressively as markets are currently anticipating.

On the fiscal side, there have been growing calls for the implementation of more demand-side policies. Measures aimed at directly stimulating consumption – such as consumption vouchers or tax relief measures – could be beneficial for kickstarting a short-term virtuous cycle, and could be increasingly necessary given the challenges of reaching the 5% growth target amid moderating manufacturing momentum.

Read the original analysis: China’s CPI inflation edges up as non-food inflation raises deflation fears

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.