China: Timing of recovery is a big question mark

China has drastically eased its Covid-19 measures. Both domestic mobility and international traffic should increase in 2023. But the question is in which quarter? The current Covid wave could last at least a few months. By then, the US and EU will likely be in recession, hurting China's exports. We also worry about the fiscal deficit getting bigger.

China: At a glance

The Chinese economy has slowed since the second quarter of 2022, mainly due to strict Covid measures that disrupted port and land logistics, retail sales and catering, and caused temporary shutdowns of factories in some key manufacturing locations. Even when restrictions were eased, a mixture of a weak domestic economy and high external inflation hit manufacturing in the fourth quarter of 2022. In addition, real estate developers have struggled to get enough cash to complete residential projects. This triggered a slew of easing measures for real estate developers to get financing via banks, stock and debt markets in the fourth quarter. The fragile economy means there has been no inflation pressure at all, and luckily no deflation. The People's Bank of China (PBoC) has used re-lending programmes to inject liquidity into specific areas, such as small and medium-sized enterprises and real estate. Conventional interest rates and required reserve ratios were not used frequently as those tools were not effective when there were Covid restrictions. The strong dollar combined with the weak Chinese economy resulted in a weak Chinese yuan (CNY) in 2022.

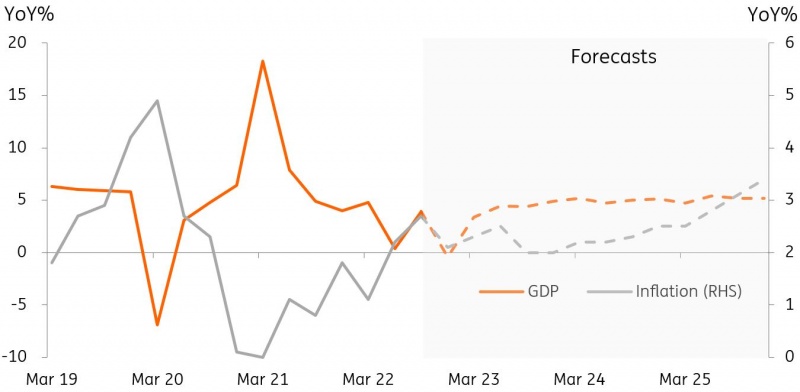

GDP and inflation outlooks

Source: CEIC, ING estimates

Three calls for 2023

1. It is really about timing when it comes to the question of economic recovery

Most Covid-19 measures were removed in December 2022. The removal of mandatory quarantine when entering Mainland China suggests that business travel will resume soon, even with the current spike in Covid cases as people in most locations outside China have become used to living with the virus. Residents could start to visit Hong Kong to get medicines and healthcare services, and then later in the year they could begin to travel to foreign countries for leisure activities. We believe that leisure travel into Mainland China could resume from the Easter holidays. Retail sales should recover, and the current Covid wave should ease after a few months (although it's difficult to gauge the timing), which should minimise the risk of supply chain disruptions.

2. External demand to be weaker in 2023

The US and Europe have been China's second and third top export destinations respectively. According to our house forecasts, the timing of recession in the US and Europe should be around the first half of 2023, and therefore should not overlap with the peak export season of the fourth quarter. But whether export demand can recover after the recession is still in question. China's trade with ASEAN – the number one export destination for China – and the rest of Asia also depend on the consumer market in the US and Europe. Both exports and imports could enter yearly contraction in the first half of 2023. Trade could recover towards the second half when domestic and external economies recover.

3. Fiscal deficit could become an issue, and unconventional monetary policy could become a norm

The fiscal deficit has not previously been an issue for China. But Covid and the real estate crisis have changed this. The fiscal deficit-to-GDP will be around 8% by the end of 2022, which is higher than the historical high (data goes back to December 1995) of 6.2% in the fourth quarter of 2020. The fiscal deficit-to-GDP should remain at 8% in 2023 even if there is much less spending on Covid tests and quarantines. Fiscal spending on high-tech development will increase. As for monetary policy, the PBoC may choose to stay on hold next year as the central bank has hesitated to lower the 7D interest rate any further to avoid falling into a liquidity trap. We do not expect the PBoC to cut the required reserve ratio or interest rates in 2023. That said, the re-lending programme for specific targets should continue at least into the first half of 2023. Further liquidity injections via the re-lending programme in the second half will depend on the speed of recovery of real estate developers and external markets. We expect the CNY to strengthen against the dollar as the economy picks up and the US enters a recession.

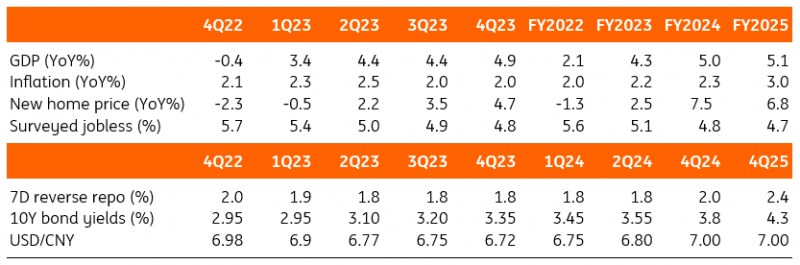

China forecast summary table

Source: CEIC, ING estimates

Read the original analysis: China: Timing of recovery is a big question mark

Author

Iris Pang

ING Economic and Financial Analysis

Iris Pang is the economist for Greater China, joining ING Wholesale banking in 2017. Iris was previously employed by Natixis and OCBC Wing Hang Bank. She earned a PhD in economics from Hong Kong University of Science and Technology.