China in 2025: Temporary adjustment or structural rebalancing of economic growth drivers?

The message delivered by Beijing at the annual meeting of the National People’s Congress at the beginning of March was clear: whatever the difficulties linked to trade and technological rivalries with the United States, the Chinese economy must achieve growth of close to 5% in 2025. The target has remained unchanged since 2023. It seems particularly ambitious this year, given that external demand, the driving force behind Chinese growth in 2024, is set to weaken significantly due to the rise in protectionist measures against China. The authorities are counting on domestic demand to pick up the slack, but this is still coming up against powerful obstacles. The authorities have announced further monetary and fiscal policy easing, as well as various initiatives to stimulate private consumption in the short term. However, the measures envisaged may not be sufficient to rebalance lastingly the sources of Chinese growth.

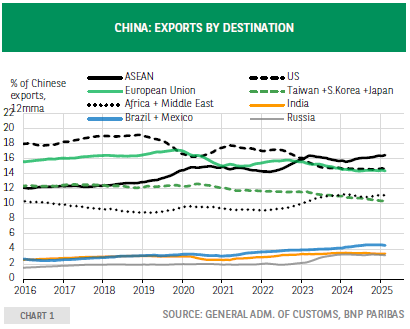

The export engine is likely to stall soon. Exports, which drove economic growth in 2024, are likely to be quickly penalised by increases in US customs tariffs. Of course, China will continue to apply its defence strategy, which has been successfully implemented since Trump’s first term in office. This strategy involves redirecting goods flows and diversifying trade partners (see chart 1), relocating part of production to connector countries in order to circumvent tariffs, and government support for the manufacturing sector. However, the protectionist shock under Trump 2.0 will be greater than the first: the tariff hikes aimed at China will be higher (+20 pp already applied to all goods since 20 January) and the US is likely to start targeting some of the connector countries soon. The European Union and other third countries could also step up measures to protect their markets from Chinese competition, which is affecting an increasingly wide range of goods.

In addition, the central bank has less room for manoeuvre to depreciate the yuan, and thus offset the effects of the new tariffs, than it did in 2018-2019. Moreover, Chinese exporters may be increasingly reluctant to reduce their sale prices after already two years of decline (export prices for manufactured goods fell 15% cumulatively over 2023-2024). Chinese export growth already slowed in January-February.

Private consumption is struggling to recover. Private consumption measured as a percentage of GDP, which fell during 2020-2022, is struggling to recover (it is estimated at 39.4% in 2024, the same level as in 2019). Since September, the measures introduced by the authorities to boost household demand have had very mixed success. Growth in retail sales accelerated slightly, mainly thanks to the government- subsidised consumer goods trade-in programme. Growth in outstanding bank loans to households reached an all-time low in January-February and housing sales, which had stabilised in Q4 2024, have fallen again since the start of the year, despite interest rate cuts and measures to encourage housing demand.

Chinese consumers remain cautious, after more than three years of property crisis that have eroded their wealth (the average price of second- hand homes has fallen by 17% since mid-2021) and because of relatively weak labour market conditions. These conditions have not returned to their pre-Covid situation with, in particular, a higher youth unemployment rate (16.9% in February) and slower growth in wages and incomes. Although consumer confidence indices have improved very slightly since October, they remain at historically very low levels.

Restoring confidence will be difficult in property, but possible in tech. In order to stimulate private consumption, the authorities must first reverse the trends observed since 2020. Firstly, by stabilising the property market. This has been a policy objective since spring 2024 (gradual easing of conditions for access to housing and mortgage credit, increased purchases of unsold homes by local governments to convert them into social housing) and will be maintained in 2025. However, success is uncertain. The continuing correction in house prices could continue to weigh on household sentiment and spending in the short term.

Secondly, by reassuring private players in the service sectors to encourage investment and job creation. In particular, this means stabilising and securing the legal environment. In fact, the President’s recent speech in support of private entrepreneurship and the promise of strategic support for tech companies mark a policy change compared with the last five years and the regulatory tightening in 2020- 2022. If confirmed, this change will boost innovation and investment, as well as job creation, particularly well-paid jobs and jobs for young graduates.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.