Previous week's events (Week 22-26.01.2024)

Announcements

U.S. Economy

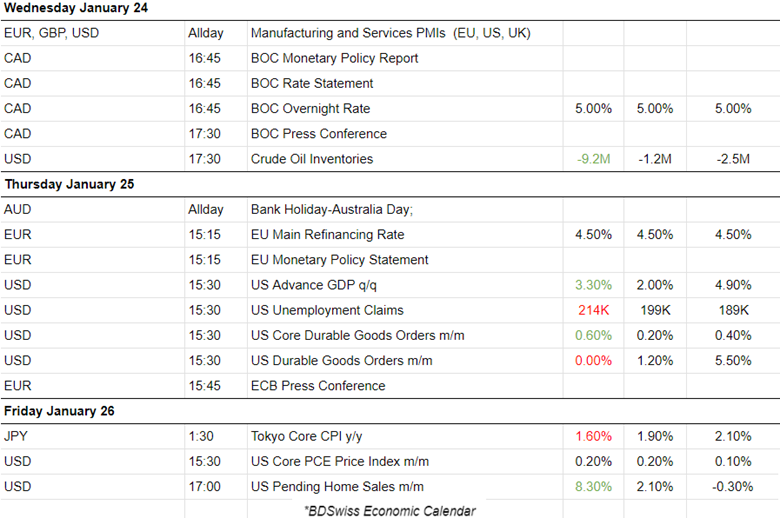

The quarterly GDP report for the U.S. last week showed that the economy grew at a faster pace than expected in the fourth quarter, suggesting the Federal Reserve would be in no rush to cut interest rates. The Advance GDP estimate showed a 3.3% annualised rate, compared with the consensus forecast of a 2% growth rate.

Initial claims for state unemployment benefits increased 25K to a seasonally adjusted 214K for the week ended Jan 20th. This was a strong increase showing tighter labour market conditions entering in January, and soon after the holiday season.

U.S. Inflation

U.S. prices rose marginally in December. The annual increase in core PCE inflation stayed below 3% for a third straight month. The U.S. central bank however is expected to keep its policy rate unchanged at the current 5.25%-5.50% range at its meeting this week. Excluding the volatile food and energy components, the PCE price index climbed 0.2% after rising 0.1% in November. The Fed tracks the PCE price measures for its 2% inflation target. Monthly inflation readings of 0.2% over time are necessary to bring inflation back to target.

New Zealand Inflation

New Zealand consumer inflation grew at a slower pace in the December quarter, meeting expectations. High-interest rates are having a desirable effect on inflation, however, it is not yet enough as the target level is still way lower. The Consumer Price Index (CPI) inflation rose 0.5% quarter-on-quarter, slowing from the 1.8% growth seen in the prior quarter. On an annualised basis, CPI rose 4.7% in the December quarter, easing from the previous quarter’s 5.6% growth.

Inflation is above the Reserve Bank of New Zealand’s (RBNZ’s) 1% to 3% annual target range and so interest rates are expected to remain higher for longer until inflation falls within its target range. The RBNZ has not said anything about trimming rates soon.

BOJ Interest Rates

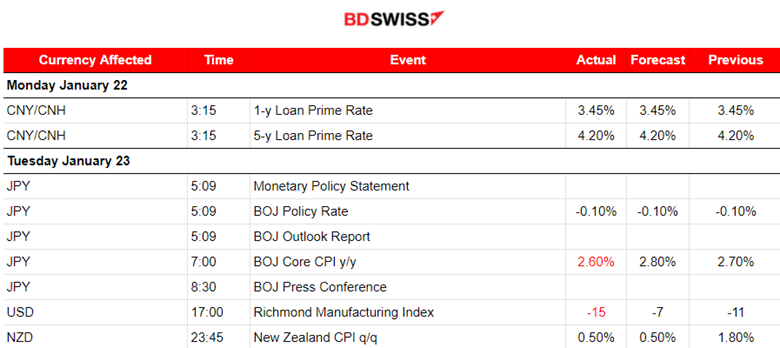

The Bank of Japan (BOJ) maintained the -0.1% policy rate, an ultra-easy monetary policy. The decision was widely expected. The central bank also suggested that an end to negative interest rates could take place soon. Negative rates have been in place since 2016.

BOJ Governor Kazuo Ueda: “The prospects of seeing trend inflation hit 2 percent are gradually heightening. That is a desirable development. But it is hard to quantify how close we have come.”

BOC Interest Rates

As widely expected the Bank of Canada (BOC) held its key overnight rate at 5% on Wednesday and mentioned that cutting borrowing costs, rather than hikes, are more probable.

Annual inflation in December accelerated to 3.4%, still higher than the central bank’s 2% target but below a June 2022 peak of 8.1%.

ECB Interest Rates

The European Central Bank’s (ECB) decision was to hold the 3 key interest rates steady and reaffirmed its commitment to fighting inflation, commenting that soon will be the time to cut borrowing costs. The ECB mentioned that it is too soon to discuss a reversal in interest rates since price pressures persist.

While fighting inflation aggressively, economists worry about the economies in the Eurozone, since recent data show worsening business conditions.

The ECB expects household and government spending to drive a recovery but data appear to be painting a bleaker picture, with manufacturing remaining in recession and services cooling.

Disruptions to trade from attacks by Yemen’s Houthi group on shipping in the Red Sea could add to inflation by pushing up energy and freight costs, she warned. “We are observing it very carefully,” Lagarde said.

Currency markets impact – Past releases (Week 22-26.01.2024)

Server Time/Timezone EEST (UTC+02:00).

-

The BOJ kept interest rates steady, the policy rate at -0.10%, and ultra-easy policy as widely expected. The central bank noted that the likelihood of the economy achieving durable 2% inflation continued to “gradually rise”. The market reacted with strong JPY appreciation at the time of the release followed by a quick retracement. The USDJPY dropped nearly 60 pips upon policy rate release and more than 100 pips during the press conference that took place later at 8:30 and retraced again quickly.

-

In the U.S. the Richmond Manufacturing Index figure was reported more negative than expected for January indicating worse conditions. However, no major impact or intraday shock was recorded for USD pairs at the time of the release.

-

According to the CPI data for the December quarter, annual inflation was reported at 4.7%, its lowest rate since June 2021. The increase in the quarterly figure was as expected 0.5%, NZD however, appreciated moderately at the time of the report release. NZDUSD jumped near 20 pips.

PMI releases for both the manufacturing and the services sector.

Eurozone PMIs

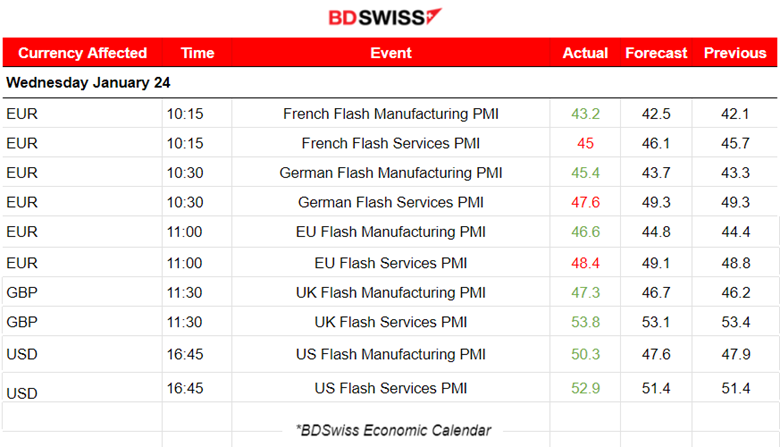

The French economy continues to show grim PMIs for both sectors with the manufacturing sector showing the worst figure of 43.2. Overall the economy ended the year 2023 in deep contraction and began the new year with more deterioration in January, with faster falls in output at both service providers and manufacturers leading to the steepest overall rate of decline since last September.

Germany continued the downturn in the private sector while stepping into the new year as business activity fell for a seventh straight month in January. The manufacturing PMI, despite improvement to a 45.4 figure, remains in contraction while the services PMI actually moved away from the 50 threshold, to a worse 47.6 points figure.

The Eurozone downturn moderates somehow at the start of 2024. The PMI figures are still reported in contraction however reports show that business activity fell at the slowest rate for six months in January. Downturns persist significantly in both manufacturing and service sectors, however, the market runs with a sense of optimism about future business conditions.

The U.K.’s PMIs are obviously showing a better picture, especially for the services sector. The Manufacturing sector saw an improvement but is still in contraction while the services sector continues with a stable expansion with the last PMI figure for services to be recorded at 53.8 points, in the expansion area. The rise in service sector activity was the fastest since last May, whereas manufacturing production decreased to the greatest extent for three months.

The U.S. PMI for the manufacturing sector, surprisingly, was recorded in expansion while the services PMI improved. Business activity expanded at the fastest pace in seven months boosting confidence with stronger orders growth and expectations for lower inflation in 2024.

-

Bank of Canada (BOC) maintained the overnight rate to 5%. No rate cuts are on the table yet. The market reacted with strong CAD depreciation after the news and press conference.

-

The European Central Bank (ECB) decided to keep the three key ECB interest rates unchanged. They are determined to ensure that inflation returns to its 2% medium-term target. No talks for cuts yet. The market reacted with a low-level intraday shock at that time and the EUR started to depreciate more and more against the dollar as time passed, with more movement taking place after the press conference.

-

The U.S. gross domestic product (GDP) grew at an annualised rate of 3.3% in the final quarter of the year, down from 4.9%. However, it is still higher than the estimated 2% for the quarter. The Durable Goods Orders figure for the U.S. was reported higher than expected, a change of 0.6% against 0.2%. Unemployment claims were reported higher than expected showing a still-tight labour market when entering the new year. There was a slight reaction in the market with USD experiencing strength but the effect soon faded.

Forex markets monitor

Dollar Index (US_DX)

A surprising upward and.

GBP/USD

The pair reversed from.

CRYPTO MARKETS MONITOR

BTC/USD

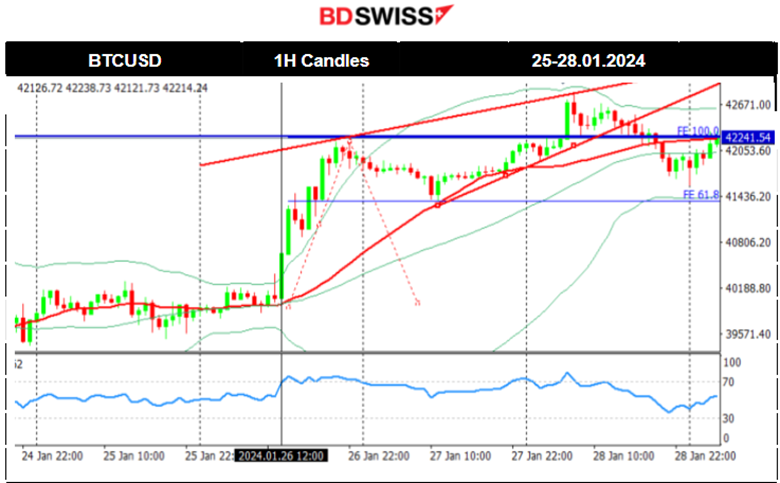

Bitcoin started to recover slowly from the recent downturn that followed after the long-awaited ETF approval from the U.S. regulator for some major asset managers. On the 26th Jan, it recorded a rapid price movement to the upside, leaving from the 40,000 USD mean, and reaching the resistance 42,250 USD. Retracement followed back to the 61.8 Fibo level that coincides with the 30-period MA. The price continued upwards steadily breaking that resistance and reaching the next at 42,800 USD before it reversed back to the MA and finally settled near the 42,250 USD level.

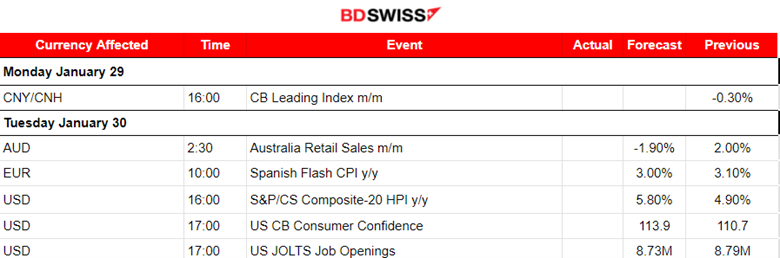

Next week's events (29.01 - 02.02.2024)

Coming up next week, two Central Banks, the Federal Reserve (Fed) and Bank of England (BoE) will comment on monetary policy and release their interest rate decisions.

Major news include labour market data releases for the U.S. with a focus on the NFP report on Friday.

Manufacturing PMI releases this week.

Currency Markets Impact:

-

On the 30th Jan, Australian retail sales are going to be reported at 2:30. The expected change is negative, meaning that a decline of near 1.9% is expected. Is the economy affected by elevated rates so much that spending would lead to this figure? A moderate shock could take place at that time causing high deviation and quick retracement for AUD pairs.

-

CB Consumer confidence is taken heavily into consideration since expectations shape the short-term course of prices. Households’ views about the relative level of current and future economic conditions affect policymakers’ decisions. The related figure shows optimism, expected to rise to 113.9. Since inflation is expected to fall further and borrowing costs to ease soon, consumers are more likely to continue spending, with the labour market getting hotter. JOLTS report at 17:00 will confirm if in December the labour market indeed was hotter than anticipated with more job opportunities, coinciding with the rest of the data, such as NFP. At the time of these two releases, a moderate intraday shock affecting USD pairs could occur.

-

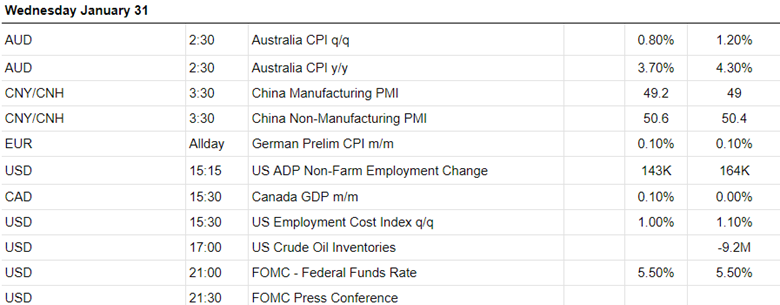

On the 31st, the CPI data for Australia at 2:30 will probably cause a shock, with AUD pairs deviating from the mean heavily and retracement will probably take place soon after, something that happens often during the Asian session. Analysts expect lower inflation figures and that, based on how quickly inflation drops in Australia, expectations are probably valid. Despite the fact that we might have no surprise, high volatility should take place at that time.

-

The U.S. ADP Non-Farm Employment change figure might shake the markets at 15:15, especially the USD pairs. This is another figure this week adding to the U.S. labour data for January and is expected to be reported lower. This expectation coincides with the latest Unemployment Claims figures that showed a significant increase, indicating that the labour market might be cooling a bit as interest rate policy remains unchanged.

-

At 21:00, the market will be affected by the anticipated FOMC meeting and Fed Fund Rate decision. A press conference will take place 30 minutes after the release. The worldwide view is that there will be no change in interest rate policy and the shock at 21:00 will probably be moderate without surprise. However, during the press conference statements from the officials could lead to increased volatility with high deviations from the means for USD pairs and asset prices denominated in dollars. Extreme caution should take place for retracement opportunities as they tend not to be completed during that session.

-

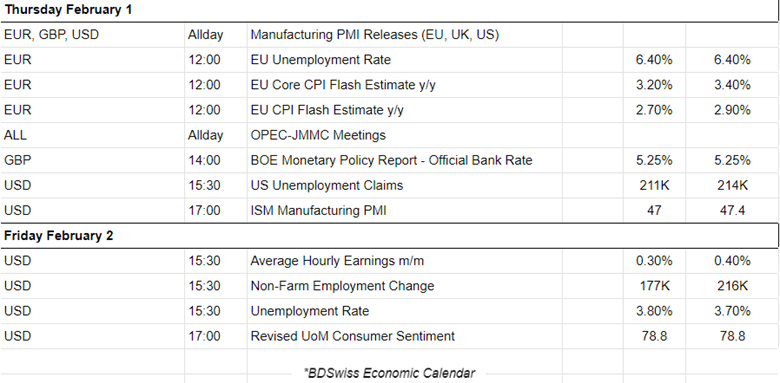

On the 1st of Feb, manufacturing PMI figures will be released during the trading day, potentially raising FX volatility. At 12:00 the CPI data could cause an effect on the EUR and related pairs. They are expected to be reported lower as inflation tends to drop as expected in the Eurozone. However, the impact on the market would probably be moderate with no major movement at that time.

-

The Bank of England (BoE) is going to release its interest rate policy decision at 14:00 and the market expects it to be unchanged. At that time the GBP will be affected probably moderately, though there is a possibility of high intraday shock at that time for the related pairs. That depends on the statements in the monetary policy report with a focus on future rate-cut-related expectations. Intraday traders should look for reversals as they tend to create opportunities.

-

The next U.S. Unemployment Claims report takes place at 15:30, expected to be reported above 200K and close to the previous figure. No major shock is expected at that time. The USD pairs could see, though, higher volatility, especially in the case of a big surprise to the downside.

-

The ISM Manufacturing PMI will add to the PMI figures this week. It is not expected to have much impact on the market unless it shows expansion, and that is unlikely.

-

On the 2nd Feb, the NFP report will be released along with the average earnings data and the jobless rate. It is the most important news of the month and refers to January. The employment change figure for December was high enough to suggest that for the specific month, the labour market was hotter than expected with the unemployment rate unchanged. In addition, inflation was actually higher than anticipated. In January, the market expects labour market cooling, as we move away from the holiday season and interest rates remain elevated. Higher Jobless rate to 3.8% and lower employment change. Nevertheless, during this major news, the USD pairs will probably see major intraday shock at the time of the release.

Commodities markets monitor

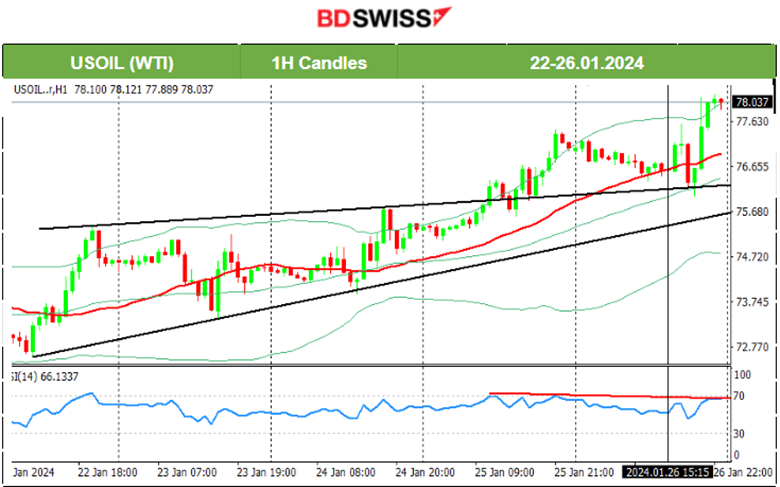

US Crude Oil

Crude oil moved higher, as mentioned in our previous report since technicals were strongly supporting an upward movement. During last week the price had steadily formed an upward wedge that was broken to the upside on the 25th. Crude oil moved upwards to find resistance at near 77.5USD/b before retracing to the 30-period MA and bouncing upwards until it reached 78 USD/b.

Gold (XAU/USD)

A triangle formation was apparent on the 24th Jan. The price dropped heavily breaking the triangle formation and moving to the 2010 USD/oz support level. Retracement followed back to 2020 USD/oz and the 61.8 Fibo level. On the 25th, gold experienced high volatility but the path remained sideways overall. That day it reached the resistance of 2025 USD/oz when it jumped after the ECB news, and reversal followed soon after back to the lows. It finally retraced later back to 2020 USD/oz. On the 26th Gold tested the resistance at near 2025 USD/oz without success during the volatile moves that took place, caused by the U.S. PCE Price Index news. It reversed immediately back to the MA continuing with the path around it and settled near the range 2018-2020 USD/oz once more.

Equity markets monitor

NAS100 (NDX)

Price Movement

All benchmark U.S. indices moved to the upside quite rapidly in the past few days, particularly since the 17th Jan. The uptrend is clear with some retracements taking place every day, however not being complete as the path is quite strong to the upside. The 4H chart below shows why this is clear. Volatility levels are higher than usual. I am expecting a retracement soon. Upon NYSE opening it would be more clear if the index will move further to the upside or break the intraday support and eventually retrace to the 61.8 Fibo level as per the chart.

Risk Warning: CFDs are complex instruments and come with a high risk of losing your invested capital due to leverage. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

The content of this material and/or any information provided by BDSwiss Group should not be in any way construed, either explicitly or implicitly, directly or indirectly, as investment advice, recommendation or suggestion of an investment strategy with respect to a financial instrument and it is not intended to provide a sufficient basis on which to make investment decisions, in any manner whatsoever. Any information, views or opinions presented in this material have been obtained or derived from sources believed by the BDSwiss Research Department to be reliable, but BDSwiss makes no representation as to their accuracy or completeness. BDSwiss Group accepts no liability for losses arising from the use of this data and information. The data and information contained herein are for background purposes only and do not purport to be full or complete.

Recommended Content

Editors’ Picks

AUD/USD defends gains above 0.6400 as US Dollar finds fresh demand

AUD/USD is retreating from near YTD highs but defends minor bids above 0.6400 early Tuesday. Hopes that the US will start to announce some trade deals remain supportive of a positive risk tone and renewed US Dollar demand, capping the pair's upside.

USD/JPY bounces back to near 142.50 amid light trading

USD/JPY rebounds toward 142.50 in the Asian session on Tuesday as a positive risk tone undermines safe-haven assets such as the Japanese Yen while providing support to the US Dollar. However, the further upside appears elusive amid a Japanese holiday-led thin trading conditions.

Gold holds below $3,350 on firmer US Dollar, easing US-China trade tensions

Gold price loses ground to around $3,335 during the early Asian session on Tuesday. The yellow metal edges lower amid a modest rebound of the US Dollar and a softening in tensions between the United States and China.

Coinbase launches new Bitcoin Yield Fund, offering investors 4–8% annual returns

Coinbase Asset Management is set to launch a new institutional product designed to deliver sustainable bitcoin-denominated returns for investors outside the United States. The Coinbase Bitcoin Yield Fund aims to tap into over $1 trillion in bitcoin liquidity to offer annualized returns of 4% to 8%.

Week ahead: US GDP, inflation and jobs in focus amid tariff mess – BoJ meets

Barrage of US data to shed light on US economy as tariff war heats up. GDP, PCE inflation and nonfarm payrolls reports to headline the week. Bank of Japan to hold rates but may downgrade growth outlook. Eurozone and Australian CPI also on the agenda, Canadians go to the polls.

The Best brokers to trade EUR/USD

SPONSORED Discover the top brokers for trading EUR/USD in 2025. Our list features brokers with competitive spreads, fast execution, and powerful platforms. Whether you're a beginner or an expert, find the right partner to navigate the dynamic Forex market.