![]() Richard Perry

Richard Perry

Independent Analyst

Market Overview

Cautious consolidation has set in across major markets with uncertainty ahead of arguably the most keenly anticipated FOMC meeting for years. Is today going to be the day that the FOMC cuts the Fed Funds rate for the first time since 2008? The short answer is yes. If the FOMC were to sit on its hands today it would be a surprise of humongous proportions, and cause a massive shock through financial markets. Whilst the US economy is ticking along relatively strongly still, the Fed is concerned about slowdown in the global economy, the impact of trade disputes and subdued inflation. An insurance cut of 25 basis points is the very least the market has priced for today. The question is one of what the Fed would do beyond a 25 basis points cut. The market is pricing for three cuts in the next year. Donald Trump is calling for a “large” rate cut. Of course Fed chair Powell will claim there is no political influence on their decision, but with Trump increasingly politicising appointments, is this really the case? That all given, we believe the market has gone too far. We believe there will be 25 basis points (to undo the highly contentious December 2018 hike) and then for the Fed to suggest that unless inflation picks up there will be another 25bps cut. The Fed has very little room to play with on interest rates for if the economy were to really hit the skids. It needs to keep its powder dry, at least for now. Market reaction will be fascinating as there are so many different ways of reading the decision. Very dovish could be initially risk positive, but also risks panicking the market so could see a risk bounce quickly dissipate. The Fed going “one and done” would be dollar strong, and cause a significant stir to Wall Street still trading close to all-time highs. Away from the Fed this morning, we have had mixed news out from the Chinese PMIs where manufacturing was a mild beat and services a mild miss. China Manufacturing PMI improved to 49.7 (49.6 exp, 49.4 in June) but still in contraction, whilst China Services PMI slipped to 53.7 (54.0 exp, 54.2 in June), meaning a mild tick higher on China Composite PMI to 53.1 (from 53.0 in June).

Wall Street closed another session in cautious consolidation, with the S&P 500 -0.3% at 3013. US futures are mildly higher today by +0.1% as markets continue to lack direction. In Asia, there has been a cautiously corrective session, with the Nikkei -0.9% and Shanghai Composite -0.6%. In Europe, yesterday’s slide is again cautiously continuing, with both FTSE futures and DAX futures around -0.2% back in early moves. In forex, there is a degree of USD slip back after recent gains. Most notably though there is a degree of support on GBP, as traders have something other than Brexit to focus on today. In commodities, the support continues to build for gold, whilst oil also continues to tick higher.

It is a big day on the economic calendar for traders on both sides of the Atlantic. First up the Eurozone flash inflation for July is at 1000BST. Eurozone headline HICP is expected to drop back to +1.1% (from +1.3% in June), with Eurozone core HICP expected to drop back to +1.0% (from +1.1% in June). There is also other key data for the region with flash Eurozone GDP for Q2 at 1000BST which is expected to show +0.2% QQ and +1.0% YY (back from a final reading of +0.4% in Q1 and +1.2% for the YY). Eurozone Unemployment is at 1000BST and is expected to remain at 7.5% for June (7.5% in May). US ADP Employment change is at 1315BST and is expected to increase to 150,000 (from 102,000 in June). The EIA oil inventories are at 1530BST with crude stocks expected to be in drawdown for the seventh consecutive week at -1.8m barrels (-10.2m barrels last week). Distillates are expected to build by +0.9m barrels (+0.6m last week) with gasoline stocks expected to drawdown by -1.5m barrels (-0.2m last week). The big focus will be later in the session with the FOMC monetary policy decision at 1900BST which is expected to show a 25bps cut to the Fed Funds rate range to 2.00%/2.25% (from 2.25%/2.50% in the June meeting).

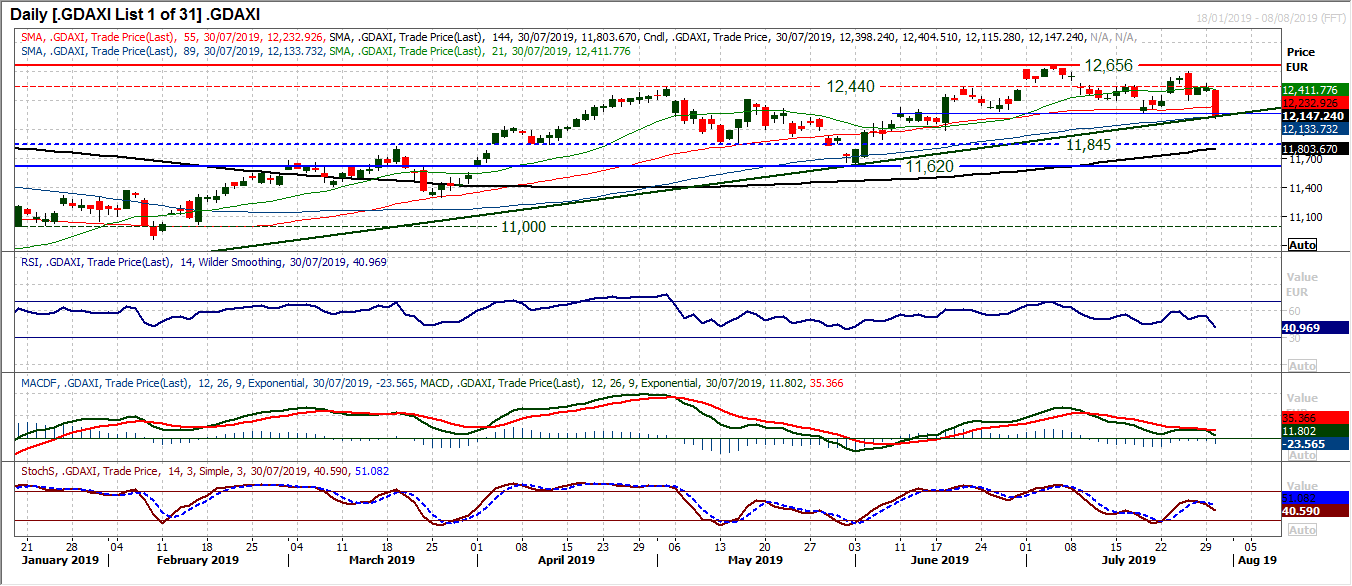

Chart of the Day – DAX Xetra

We looked at the outlook for the DAX earlier in the week, discussing the importance of how the market responded around the 12,440/12,465 key pivot band. Things can move fast on the DAX. Concerns over a no deal Brexit, coupled with Trump’s negativity over the China trade talks have hit the DAX hard. A massive bull failure around the old pivot now has quickly seen the DAX selling sharply lower and at a crucial crossroads. The DAX is back to the support of a seven month uptrend. Momentum has taken a worrying turn for the worse, with the bear kiss on MACD and bear cross on Stochastics. However, the RSI is on the brink. Having consistently found a bottom throughout the uptrend in the low 40s, a move back into the 30s would be a significant medium to longer term negative development. A close below 12,190 (support of the June and July lows) has effectively completed a five week top (a second closing breach would confirm) and this would imply around 460 ticks of additional corrective downside towards 11,725. This would put the index bang into the midst of the massively important long term higher low and band of support 11,620/11,845. On a technical rally today 12,190/12,227 becomes a neckline band of resistance. Realistically though, the bulls need to get back above 12,299 to improve the outlook once more.

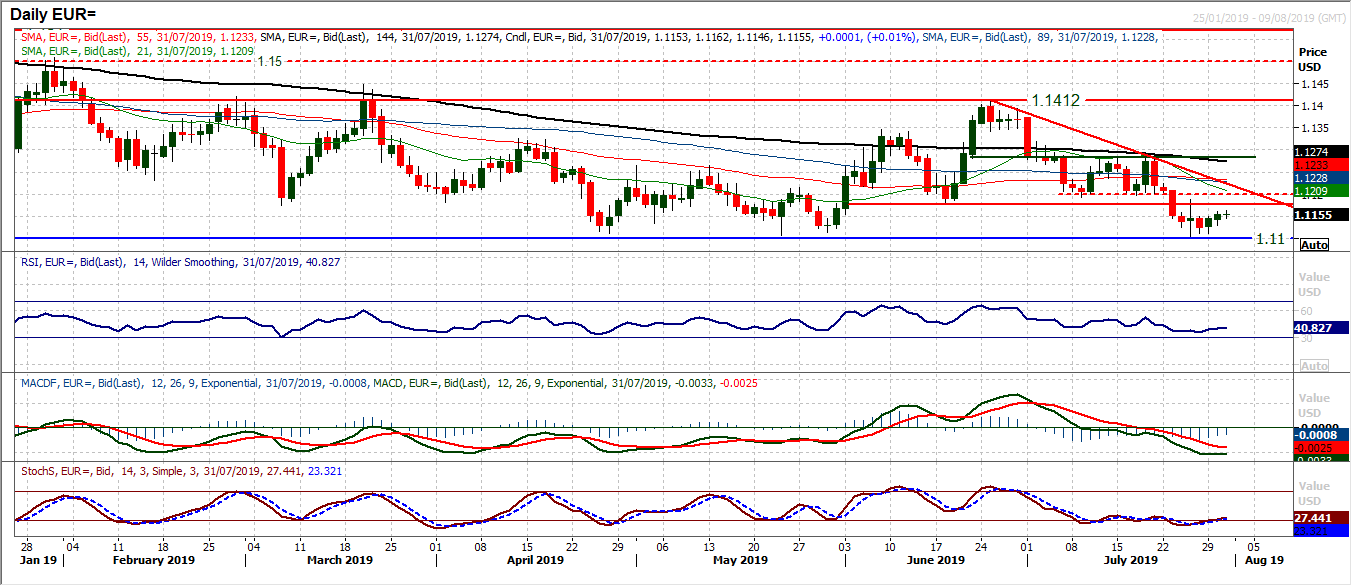

A second consecutive positive candlestick has just helped to stabilise the outlook once more. The market has picked up and is now trading well off the support band $1.1100/$1.1110 which has been so important in recent sessions. The market has also edged above the initial resistance at $1.1150. Essentially though, this is a market biding time in front of the crucial Fed meeting. The technical outlook on the euro remains one to sell into strength. The resistance of overhead supply from the June and early July lows between $1.1180/$1.1200 did for the post ECB rally and is again important. A five week downtrend also comes in at $1.1225 today. Momentum indicators are negatively configured to suggest that rallies are a chance to sell. The big move would be a hawkish surprise from the Fed which would see the market dragged back under $1.1100 support. A closing breach would open $1.1000 initially but the next key support is not until $1.0850.

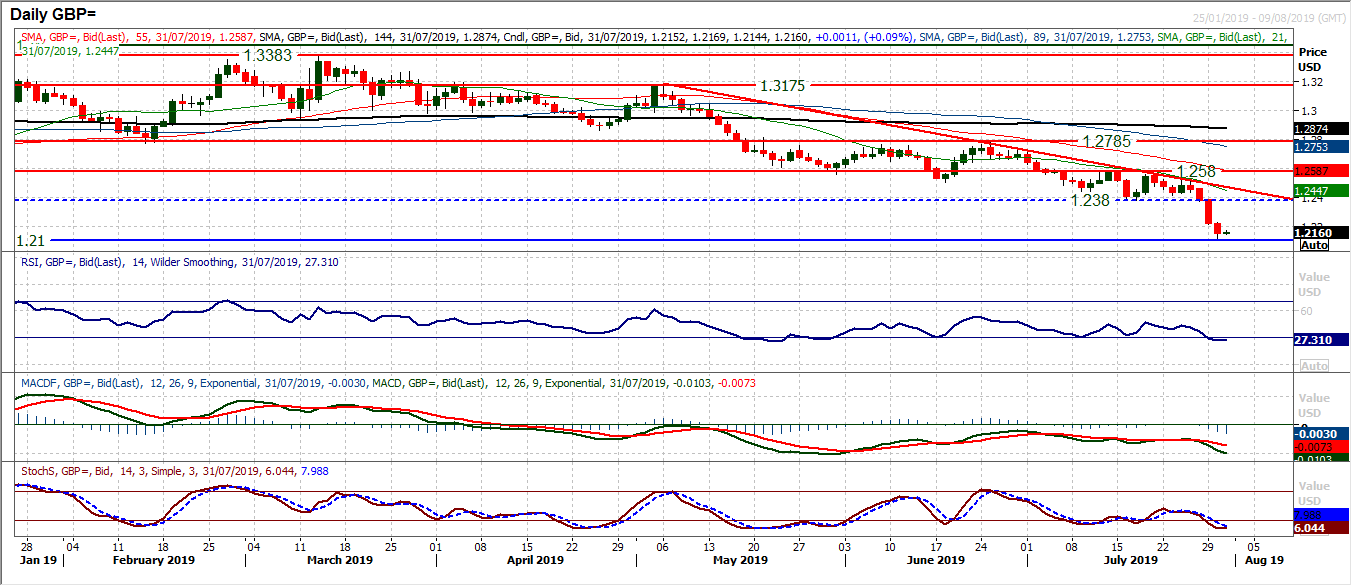

The selling momentum on Cable has just begun to dissipate in front of the Fed. Having lost four big figures (400 pips) in the past four sessions, Cable has (temporarily at least) found a floor at $1.2117. This is a shade above the next key low from way back in March 2017 of $1.2100. There is now a degree of consolidation forming. However, the next move is likely to be Fed focused and later in today’s session. Technically, the chart remains extremely negatively configured and any intraday strength is a struggle. The stretched nature of momentum would normally suggest that an unwinding move (technical rally) is due. However, looking on the hourly chart, it is in the process of already playing out. The is minor resistance $1.2190/$1.2210 which if the bulls can muster some sort of momentum then they could engage a more considerable move. There is little real resistance until $1.2350/$1.2380. Our fear is that the downside is not done yet, not by a long shot. Under $1.2100 opens the critical low at $1.1980, below which all bets are off.

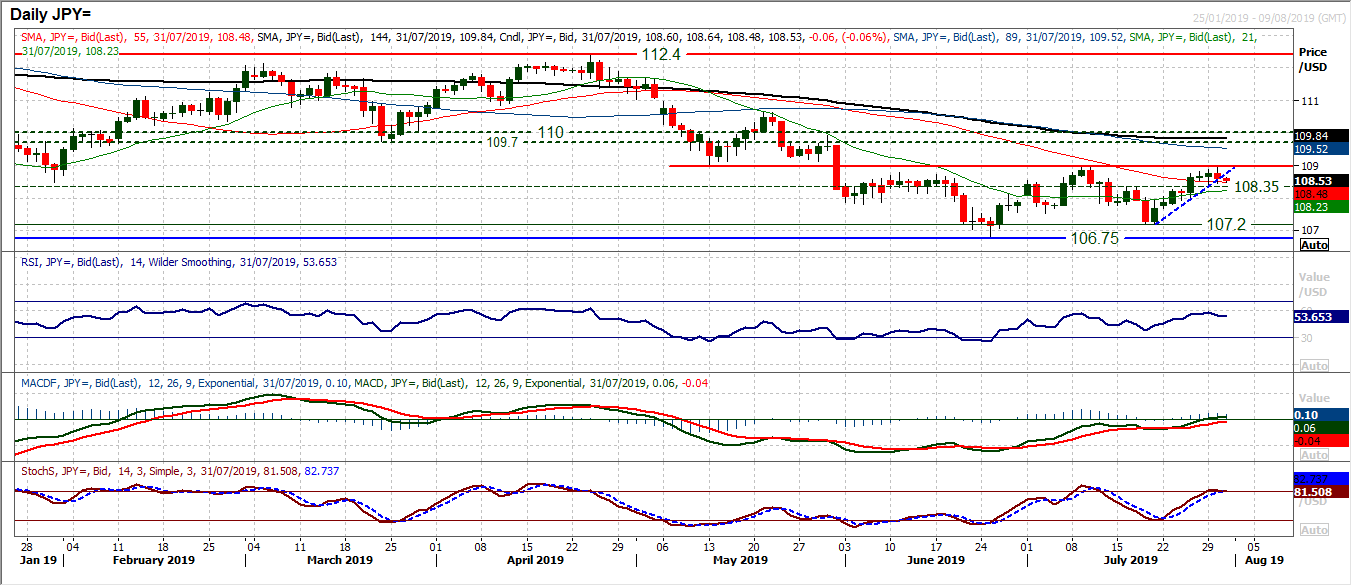

The bulls have just lost a degree of control in the eight week range again as the market slipped back from the key resistance at 109.00. This has resulted in the breach of a sharp near term uptrend. This consolidation, or loss of trend is not to be unexpected ahead of such a crucial (and uncertain) decision by the Federal Reserve today. However, it also runs the risk of this being another bull failure on Dollar/Yen. The rolling over for the RSI under 60 is happening again and has been a consistent feature of the past three months, whilst the MACD lines are simply back to flatten around neutral too. A gauge for the market comes in at the near term pivot at 108.35. A close back under 108.35 tonight would certainly suggest a risk off reaction to the Fed and a likely renewal of a corrective move lower within this 106.75/109.00 range. We continue to see the path for Dollar/Yen upside is difficult to sustain with 109.00 resistance but also the medium term pivot band 109.70/110.00.

Gold

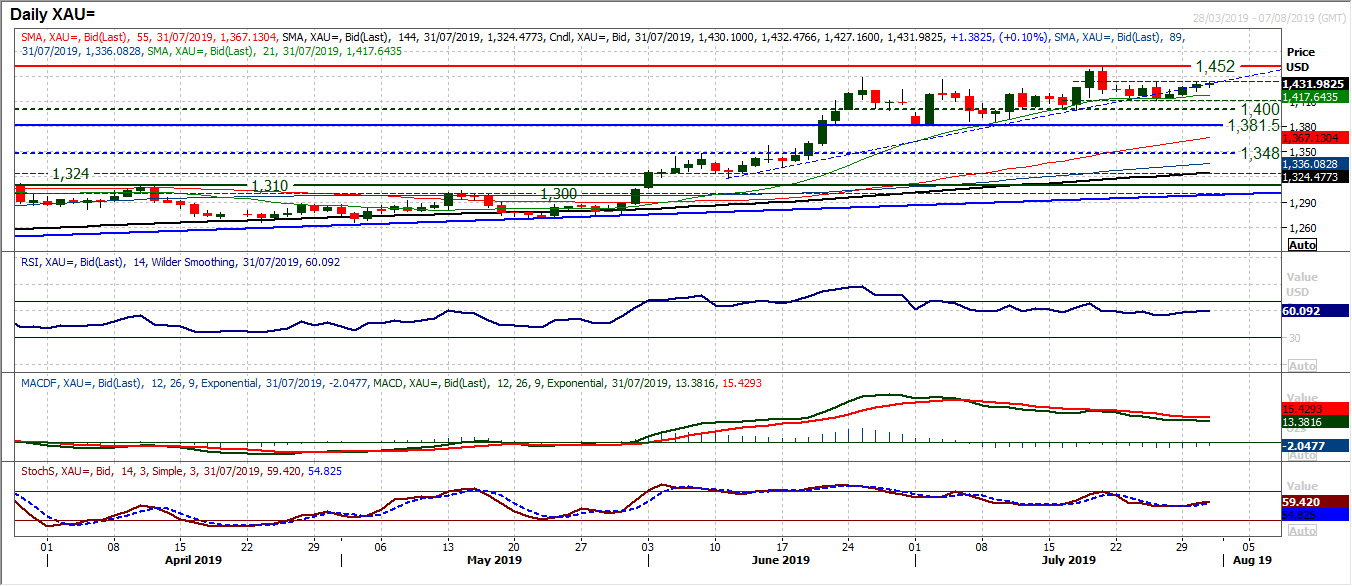

Although the consolidation between $1411 and $1433 continues in front of the Fed, the past few sessions have again suggested that the bulls are building again. There is still a sense of an underlying appetite to buy gold which is helping to maintain support. Holding consistently above the once more rising 21 day moving average (today at $1417) is something to increase the positive aspect to the chart. Momentum indicators have been slipping back in recent weeks in a move which we believe is helping to renew upside potential, but now they are beginning to stabilise and look higher again. We continue to expect gold to be pushing higher and a close above $1433 would re-open the multi-year high at $1452 again. It would also increase the potential that $1411 becomes a higher low and key support. We will know much more tonight after the Fed, but the bulls are positioning for their next run higher.

WTI Oil

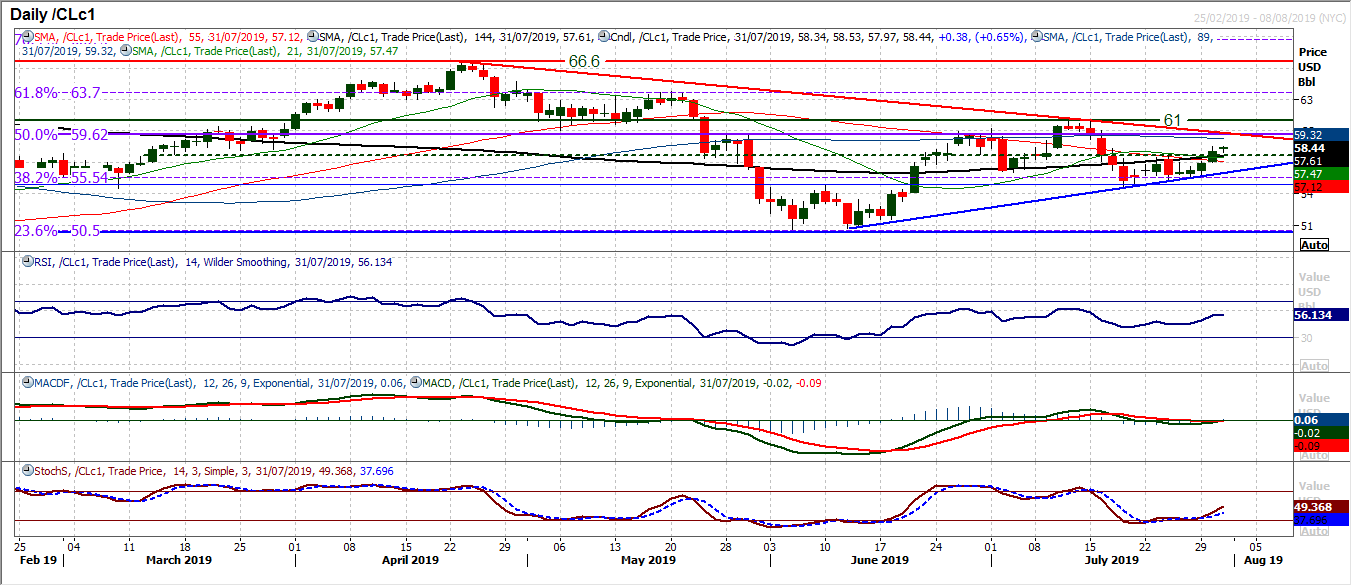

The near term outlook for oil has picked up considerably in the past few days. After spending much of last week stuck in consolidation, a couple of decisive positive candlesticks has really breathed some life into the market. Yesterday close above near term resistance at $57.65 is seeing the market pulling higher back towards the 50% Fibonacci retracement (at $59.60) once more. This Fib level marked the beginning of a resistance band $59.60/$61.00 that capped the June/July rally, but is open once more. Momentum is certainly going with the move, with the RSI back above 50, Stochastics improving decisively and the MACD lines threatening a cross back higher. The hourly chart reflects the positive momentum, with support in the band $57.30/$57.65 as intraday weakness now becomes a chance to buy for a test of $59.60/$61.00.

Dow Jones Industrial Average

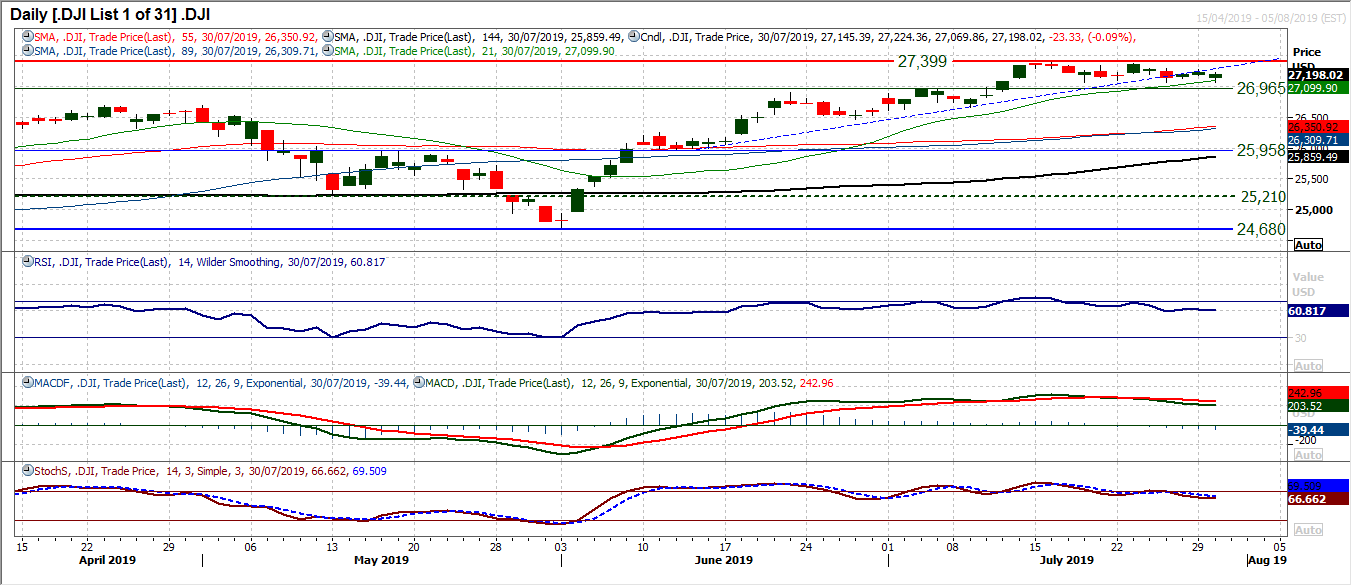

Ahead of such a crucial meeting of the FOMC it should be of little surprise that the consolidation continued yesterday. This is very much a market in wait and see mode. Until the Fed sets its stall out, it will be difficult for Wall Street to take a view. Subsequently, whilst the Dow has broken a six week uptrend, the market is simply consolidating between the low of last week at 27,069 and the all-time high of 27,399. Whilst the support of the breakout at 26,965 remains intact, this is simply a period of wait and see. Momentum indicators remain benign. The MACD lines, that have still got a bear cross, but are flattening, whilst the RSI is steady a shade above 60. Given the lack of real direction from the candlesticks in recent days and the importance of this Fed meeting, there is a lack of direction this morning. We expect the picture to be entirely different in 24 hours. Resistance overhead at 27,298/27,399.

Note: All information on this page is subject to change. The use of this website constitutes acceptance of our user agreement. Please read our privacy policy and legal disclaimer. Opinions expressed at FXstreet.com are those of the individual authors and do not necessarily represent the opinion of FXstreet.com or its management. Risk Disclosure: Trading foreign exchange on margin carries a high level of risk, and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss of some or all of your initial investment and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange trading, and seek advice from an independent financial advisor if you have any doubts.

Recommended Content

Editors’ Picks

EUR/USD holds gains near 1.0900 amid weaker US Dollar

EUR/USD defends gains below 1.0900 in the European session on Monday. The US Dollar weakens, as risk sentiment improves, supporting the pair. The focus remains on the US political updates and mid-tier US data for fresh trading impetus.

GBP/USD trades sideways above 1.2900 despite risk recovery

GBP/USD is keeping its range play intact above 1.2900 in the European session on Monday. The pair fails to take advantage of the recovery in risk sentiment and broad US Dollar weakness, as traders stay cautious ahead of key US event risks later this week.

Gold price remains on edge on firm prospects of Trump’s victory

Gold price exhibits uncertainty near key support of $2,400 in Monday’s European session. The precious metal remains on tenterhooks amid growing speculation that Donald Trump-led-Republicans will win the US presidential elections in November.

Solana could cross $200 if these three conditions are met

Solana corrects lower at around $180 and halts its rally towards the psychologically important $200 level early on Monday. The Ethereum competitor has noted a consistent increase in the number of active and new addresses in its network throughout July.

Election volatility and tech earnings take centre stage

/stock-market-graph-gm532464153-55981218_XtraSmall.jpg)

The US Dollar managed to end the week higher as Trump Trades ensued. Safe-havens CHF and JPY were also higher while activity currencies such as NOK and NZD underperformed.