BRICS expansion and what it means for the US Dollar

The BRICS grouping of major emerging economies is holding its fifteenth summit later this month. Up for discussion: an expansion of the bloc, greater use of local currencies and the possibility of a BRICS currency which may have the potential to challenge the dominance of the US dollar. We'll outline here the key points and link to our major new report.

Would a larger bloc mean faster de-dollarisation?

The BRICS grouping of major emerging economies, Brazil, India, China, South Africa and Russia, is holding its fifteenth summit later this month. Up for discussion: an expansion of the bloc, greater use of local currencies and the possibility of a BRICS currency which may have the potential to challenge the dominance of the US dollar.

Any expansion of the BRICS grouping could determine the speed with which the bloc adopts commercial and financial systems outside of the dollar sphere. Speculation is rife as to how many countries, if any, will join the club – for the first expansion in a decade. In order to evaluate how the political ambitions correlate with underlying economic trends, we take a closer look at the overall evolution of the US dollar’s role in the various areas of the global economy and markets. Here are the observations so far:

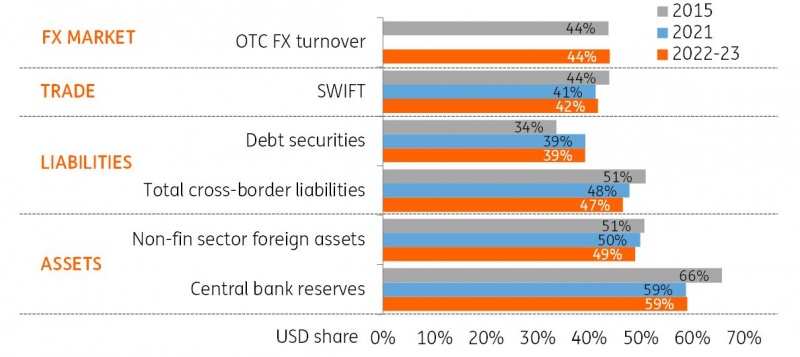

There has been a drop in the dollar’s share of central banks’ FX reserves, but dollar usage has held up very well in commerce, private assets, debt issuance, and generally on the global FX market.

Among the potential dollar challengers, the euro may seem like a runner-up, but its dominance is seen only in Europe. Looking at the BRICS, China’s amplification of renminbi swap lines seems to have helped promote the use of its currency in trade and international reserves, and Russia’s geopolitical aversion to the dollar gave CNY an additional boost, but China’s capital controls and low issuance of panda bonds remain an obstacle.

The rising usage of alternative currencies does not seem to be threatening the dollar but rather increasing the competition among the regional currencies amid fragmentation of the trade and capital flows.

No currency has made any inroads to the dollar’s pre-eminent status as the issuance currency of choice. Having been a major factor in removing sterling’s crown last century, challenging the dollar’s status in the international debt market has to be a central strategy for the young pretenders.

De-ollarisation summary

Source: IMF, SWIFT, BIS, ING

Overall, we do not see any conclusive evidence that the dollar is on the path of structural decline at this point. However, it is still facing challenges stemming from both economics and geopolitics.

The challenge to the Dollar

The war in Ukraine and the freezing of Russian FX reserves in 2022 have prompted much discussion on the ‘weaponisation’ of the dollar, the splintering of geopolitical blocs and ultimately the “inexorable” decline in the use of the dollar – or ‘de-dollarisation’. An integral part of this debate will not only be how those geopolitical groupings develop but also whether other currencies can challenge the dollar’s international role.

The subject of de-dollarisation should gain more traction

We suspect the subject of de-dollarisation might gain some traction this summer when senior leaders of the BRICS nations meet in South Africa on 22-24 August. At the top of the summit’s agenda is the proposed expansion of this geopolitical grouping and perhaps some proposals relating to a common payment system in BRICS currencies. Regarding BRICS expansion, speculation is rife as to how many countries, if any, will join the club – for the first expansion in a decade. The focus here tends to be on countries that have already joined the BRICS-sponsored New Development Bank (NDB). These include countries such as the United Arab Emirates, Egypt, and Bangladesh.

The proponents for accelerated change argue that some of the major oil exporters like Saudi Arabia, Iran and Nigeria might be included, too. Experts, however, warn that friction between China - a proponent of expansion - and the more reticent India makes the subject highly uncertain.

It's all about the speed of any BRICS expansion

Why this is important to the de-dollarisation debate is that the speed of expansion in BRICS could well determine the speed with which this bloc adopts commercial and financial systems outside of the dollar sphere. There are also suggestions that this summit could re-introduce the subject of a BRICS currency.

Far from abandoning their own national currencies, we presume this venture could be pursued along the lines of a new ‘Unit of Account’ – similar to the IMF’s Special Drawing Rights (SDR). For example, the NDB or other commerce being conducted in ‘BRICS’ could require users to hold more of these currencies and potentially gravitate away from the dollar.

The link to de-dollarisation here is that the creation of a BRICS unit of account could increase these currencies’ shares in FX reserves of BRICS users – in the same way that China’s 2015 entry into the SDR basket was meant to increase interest in the renminbi. Away from the speculation over the future of BRICS, our article examines evidence of de-dollarisation seen so far. There are a whole host of scholarly articles on this subject and perhaps one of the best definitions of what makes an international currency is outlined in the chart below. Here, the function of an international currency is assessed through the prisms of both the public and private sectors.

Roles of an international currency

While we find this a useful framework to assess the extent of de-dollarisation, we prefer to examine the challenge to the dollar’s dominance through the three key areas:

-

Trade and commerce.

-

The asset side (store of wealth).

-

The liability side (currency of issuance).

And we go into much more detail about all that in our full report. Click here to download the PDF document in its entirety.

We'll look at why the USD remains the preferential currency for trade and how any BRICS expansion may impact that.

We'll dive deeply into the issue of de-dollarisation and how likely any changes to the status quo are going to be.

And we'll examine the dollar's liability status and its role in the FX markets, among many other important points.

Read the original analysis: BRICS expansion and what it means for the US Dollar

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.