Brexit Begins [Video]

![Brexit Begins [Video]](https://editorial.fxstreet.com/images/Macroeconomics/Events/ElectionUK/Brexit_scrabble_XtraLarge.jpg)

The Day So Far…

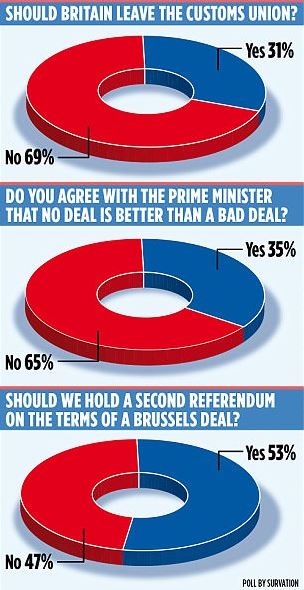

Over the weekend press coverage continues to be dominated by global politics with focus on questioning the fate of UK Prime Minister Theresa May in stark comparison to a jubilant Emmanuel Macron who secured a resounding majority in the French legislative election. Given this lack of major economic data this week I would expect these political themes will continue to be the major driver of financial markets for the foreseeable future. Brexit talks officially kick off today in Brussels and the Queen’s speech on Wednesday will outline the government’s proposed legal programme for the coming year before EU leaders then preside over matters on Thursday and Friday. What has been somewhat surprising in the wake of the UK hung parliament has been the relatively tame response seen in the GBP. Sure inflation is now at multi-year high (2.9%) and investors were caught surprised by the hawkish split in last weeks MPC vote (5-3) but to me the relative calm in the markets is more a response to the inevitability that EU negotiations are likely to end in a much more softer Brexit than what was first envisaged by the Tory government just several weeks ago. Interestingly one of the few polls released since the election shows that Labour now lead the Conservatives by 44% to 41% and when broken down specifically into questions on talks with Europe it becomes even more clear that sentiment has shifted towards remaining in the Customs Union and Single Market.

With Theresa May’s popularity dipping even further following the poor handling of the Grenfell Tower fire my thoughts are that once Britain settles its divorce bill the country will then look to secure a transitional deal which will include access to these key European markets and as such the fate of May seems all but inevitable given her originally mandate was pinned on delivering a hard Brexit. Guessing the timing of her departure with any great accuracy is difficult and one off events (terror attack/fire) can have an immediate impact on public perception and sentiment. Whether she stays or goes I believe makes little difference as I see either situation leading to a softer version of Brexit. The main obstacle to the Pounds recovery then would be in the scenario that rising inflation leaves the Bank of England with no alternative but to hike rates a scenario that would be detrimental to the already squeezed consumer.

The Day Ahead…

Not a great deal to look forward to this afternoon so I would be identifying key technical levels and playing the range accordingly with relative conservatism. Both the DAX and S&P are close to all-time highs despite the late wobble in US retail names on Friday following the fears of a new dominant competitor in the form of Amazon on the high street in the guise of Whole Foods. As such I would be looking for those previous highs to hold firm for the time bring and we prefer looking for pull backs to re-enter long positions. Meanwhile, WTI crude has seen a test of Friday’s high despite US drillers adding rigs for a 22nd consecutive week, the longest stretch in three decades.

We still feel bearish on the prospects of OPEC’s ability to influence prices over the long-term and with US output continuing to climb the oversupplied nature of the market gives us reason to prefer the short for now. Any breach of $44 and the 5th May low of $43.76, opens up the prospect of another leg lower with the obvious target being the November 2016 lows of $42/bbl, a point of which will severely test the nerves of OPEC nations given they have already committed themselves to cuts out to March 2018.

Author

Amplify Trading Team

Amplify

Amplify Trading is a proprietary trading company specialising in the development of new trading talent offering direct experience in financial markets.