Breakout consolidation

S&P 500 breakout or fakeout? I was in favor of breakout and its retest Friday. Not even debt ceiling resolution stumble or Powell talking about not needing to raise rates too much given the commercial lending stress (tightening) or Yellen bringing up more consolidation ahead in the banking sector.

Let‘s keep it technical, quoting Friday‘s analysis:

(…) The key thing that changed, is that we‘re dealing with a breakout now – above both 4,188 and 4,209. Unconfirmed for now, so let‘s examine its odds to answer that „breakout or fakeout“ question.

First, neither daily volume nor market breadth changes stand in the way of either ES or NDX.

Seconds, bonds held up in the risk-on mode well, and the low HYG volume wasn‘t met with poor price action while yields rose.

Third, XLI strongly refused the daily downswing, XLF pulled out a nice daily consolidation, and Russell 2000 as the greatest underperformer behind KRE, rose within its practically horizontal range.

This makes me think that S&P 500 is likely to consolidate the breakout rather than come crashing down. Unless Fed speakers today „surprise“ with further insistence on no rate cuts any time soon (quotation marks are ironical as they wouldn‘t relent – both 3m and 10y yields registered strong increases yesterday, and Jun 25bp rate hike odds went up considerably) – that‘s the most probable factor to drive an ES breakout today apart from typical opex day volatility.

Not even the heavily bought into tech and semiconductors flash warning signs for S&P 500 as the rotations yesterday have been shown to be strong, and this kind of performance doesn‘t usually disappear within a day.

USD isn‘t standing in the way – earlier calls for 101 to hold, and greenback relief rally are working out fine, now over 103 and in need of consolidation after the reflexive „debt ceiling resolution“ (not yet, but the interim positive signs won‘t disappear today) rally.

The extent of opex day volatility is the key variable today – together with the Fed speakers comments revealing what the broad rally yesterday was made of (strength of foundations and rotations). Odds are good for a no meaningful setback.

The breakout will succeed even if I‘m looking for a bit more (shallow) weakness first. Tech and semiconductors continue doing well – a little consolidation with an improvement in (still divergent) Nasdaq breadth, resulting in making Big Tech stocks vulnerable to a brief pullback Monday or Tuesday. Value was hit, but not on high volume – the positive rotational tendencies beyond industrials, energy and financials at expense of defensives (utilities and staples) continued. The discretionaries to staples, financials to utilities, or stocks to long-dated Treasuries, all confirm the appetite (to last a few weeks more) to go higher following breaking the long S&P 500 range.

The breakout retest though looks still undone to me, and it‘s due to the faltering strength of daily rotations Friday, incl. the above mentioned Big Tech. 4,188 should be still revisited next week – this is not yet the time of tech falling to force much, much lower prices and snowballing. More debt ceiling fears should be the catalyst, but I‘m looking for a weak entry into Monday even without dramatic headlines.

After a successful retest of the breakout, in other words putting in a short-term bottom, stocks would continue higher – but this isn‘t the case of sky is the limit, whether Fed hikes in Jun or not.

Unemployment claims would pick up, core inflation not decelerate fast enough, retail sales and bank lending would remain underwhelming, and yields would make a peak before heading lower again to reflect darkening economic prospects. It‘s only when they come down that they would clear the real estate market, which means that 2H 2023 is pointing down for both residential and commercial real estate.

LEIs remain in steep decline mode, and after all data revesions are completed, it seems to be the case that recession is starting Jul, Aug or Sep – yes, that‘s my Q3 call. The Fed hasn‘t yet pivoted, and the 2-y to Fed funds rate spread is almost 1% now. Very clear signal from bonds that real economy is in trouble, which however doesn‘t stand in the way of stock market gains in the weeks to come.

The downleg has only gotten delayed, and I have question marks whether 3,800 will be broken in the summer (and usually the turbulent month of Sep) – 3,865 seems a more conservative target, but the bulls improved their lot significantly as I acknowledged following Wednesday‘s financials move.

How about next week‘s key data – what do they mean for markets?

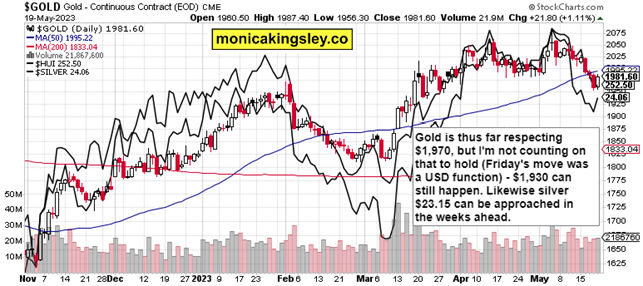

Gold, Silver and Miners

Precious metals were driven by the rate hiking reappraisals when Powell on Friday undid all the 25bp odds made by prior Fed speakers in the week. The correction isn‘t over for me, and targets stretched to the bearish side, are given in the caption.

Crude oil

Crude oil is out of the woods – no matter the upcoming recession, the May lows won‘t be broken. Slow grind higher accompanied by renewed good performance in oil stocks (in spite of solid dividends, had been lagging since stellar 2022), awaits beyond the weeks ahead.

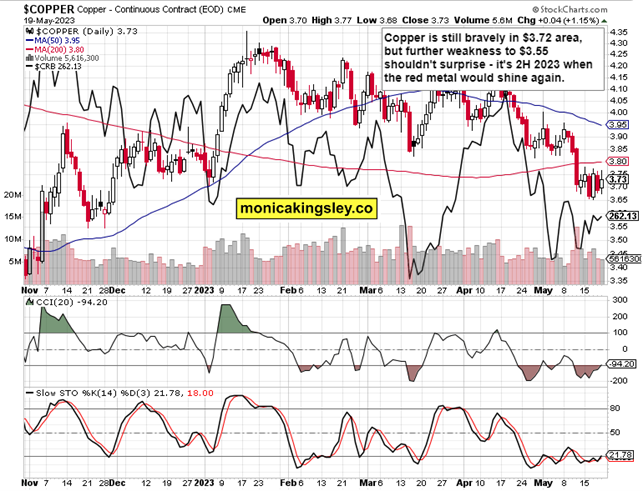

Copper

Copper wouldn‘t be immune in the short term – data out of China are mixed, and commodities do and would suffer in the environment of weakening inflation, which for all the core resilience would continue weakening. So, bullish fundamentals of physical stockpiles would be clashing in the weeks ahead with slowing real economy before commodities pick up vibrantly again in 2H 2023.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.