US durable goods orders and consumer confidence dropped, RBNZ keeps rates steady, Bitcoin to 65K USD

Previous week's events (Week 26.02-01.03.2024)

Announcements

Crypto

Bitcoin jumped surprisingly since the 26th Feb, reaching currently near 65,000 USD. The Crypto market in general saw huge gains as all Crypto with the highest market cap moved to the upside.

Recent analysis shows that there is a surge of funds into bitcoin ETFs. Another factor that explains the bullish phenomenon is the upcoming “halving event”

U.S. Economy

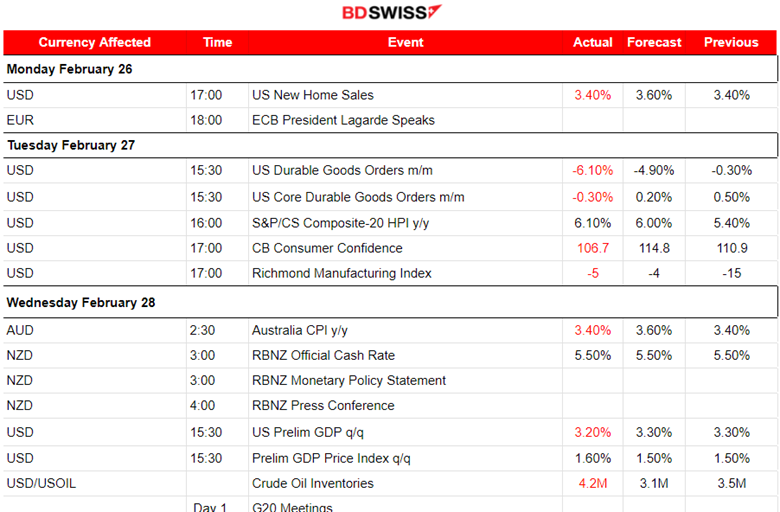

Reports on the U.S. durable goods figures show that orders fell by the most in nearly four years in January, while business investment in equipment appeared to have eased, signs that the economy lost momentum at the start of the year.

The report on consumer confidence shows that Americans are quite concerned about the economy’s outlook, especially the labour market, and the upcoming presidential election resulting in confidence retreating after three straight monthly increases. The Conference Board (CB) showed its consumer confidence index slipped to 106.7 this month from a downwardly revised 110.9 in January.

Interest rates

RBNZ

The RBNZ decided to keep the cash rate steady at 5.5% and trimmed the forecast peak for rates, catching markets by surprise. The RBNZ’s statements triggered a selloff in the New Zealand dollar and a rally in bonds.

The bank lowered its forecast cash rate peak to 5.6% from a previous projection of 5.7% – toning down its hawkish stance and effectively reducing the risk of further tightening.

The RBNZ’s statement reflected the need to keep policy restrictive for a while in order to bring inflation below the top-end of its 1% to 3% target band.

Inflation

US

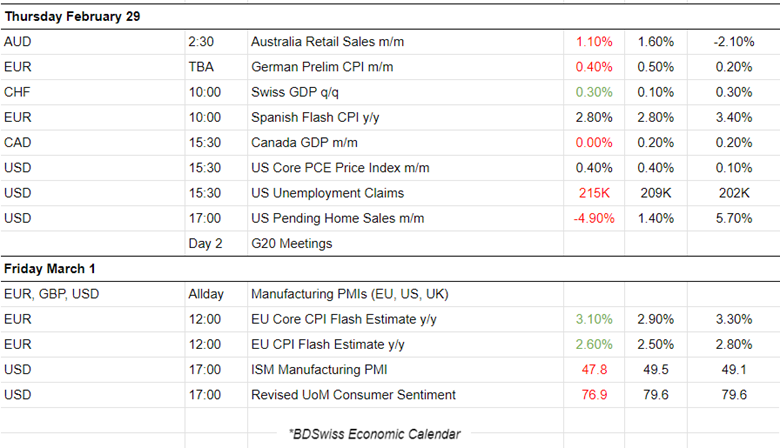

The personal consumption expenditures price index (PCE) excluding food and energy costs increased by 0.4% for the month and 2.8% from a year ago, as expected.

PCE, including the volatile food and energy categories, increased by 0.3% monthly and 2.4% on a 12-month basis, also in line.

Personal income rose 1%, well above the forecast of 0.3%. Spending decreased by 0.1% versus the estimate for a 0.2% gain.

Initial jobless claims totalled 215K for the week ended Feb. 24, up 13,000 from the previous period and more than the 210,000 estimate.

Eurozone:

Eurozone’s inflation saw a drop last month but underlying price growth remained stubbornly high. This might hold elevated rates for longer.

Inflation across the 20-nation Eurozone fell to 2.6% in February from 2.8% a month earlier, just shy of expectations for 2.5%, data from Eurostat. However, crucial core figures only declined to 3.1% from 3.3%, missing expectations for 2.9% and holding uncomfortably above the ECB's 2% target.

The ECB has kept its deposit rate at a record high of 4% since September.

Markets now see around 90 basis points of rate cuts this year with the first move coming in June, a date that has been mentioned by a host of policymakers, too, as a reasonable start for rate cuts.

Currency markets impact – Past releases (Week 26.02-01.03.2024)

Server Time/Timezone EEST (UTC+02:00).

-

Reports for the durable goods orders for the U.S. on the 27th Feb were released. They marked the largest drop in nearly four years in January. A 6.10% decline, way more negative than expected. There was no major impact recorded in the market.

-

The CB consumer confidence report recorded a drop. U.S. consumer confidence soured in February for the first time in three months according to the survey. The survey’s index fell in February to 106.7, down from a reading of 110.9 in January. The market reacted with a moderate USD weakening at the time of the release.

-

Australia’s inflation remained steady in January according to the report on the 28th Feb, below economist expectations of a bounce. The market reacted with AUD depreciation but experienced only a light shock at that time. The AUDUSD only dropped significantly soon after when the USD experienced heavy appreciation.

-

The Reserve Bank of New Zealand (RBNZ) left the official cash rate unchanged at 5.5% and says risks to the inflation outlook are now ‘more balanced’ but there is a limit to the ability to ‘tolerate upside inflation surprises’. The NZD depreciated heavily and the NZDUSD dropped more than 70 pips since the time of the decision release.

-

Canada’s preliminary GDP figure, for the last quarter, was reported lower beating expectations. Real gross domestic product (GDP) increased at an annual rate of 3.2% in the fourth quarter of 2023, a slight downgrade from the government’s initial estimate. The market did not react significantly at the time of the release but the USD weakened slightly after that.

-

Australia’s retail sales report, released on the 29th Feb, showed growth of 1.10% but this was less than expected. No major impact was recorded at the time of the release, however, the AUD surprisingly appreciated against the USD and other currencies, soon after the release.

-

Canada’s GDP report showed that the real gross domestic product (GDP) was essentially unchanged in December, following two months of growth. The market did not react heavily to the news, no special effect on CAD. However, the USDCAD dropped heavily due to the U.S. PCE report causing the USD to depreciate heavily.

-

The U.S. core PCE price index, a measure of inflation, fell to the lowest rate since early 2021, reports said yesterday at 15:30. Investors, home buyers and consumers alike are looking for interest rate cuts after this supporting evidence of further inflation cooling. The market reacted with USD depreciation after the release and that did not last long. The dollar soon after appreciated heavily.

-

U.S. unemployment claims were reported higher than expected at 215K in the week ending February 24. This is however not a significant increase considering the volatility of these figures every week. In general, the labour market is not actually cooling, it is quite tight.

-

The U.S. pending home sales fell by the most since August as borrowing costs remain high. Elevated mortgage rates kept a lid on housing demand.

Manufacturing PMIs:

Eurozone PMIs:

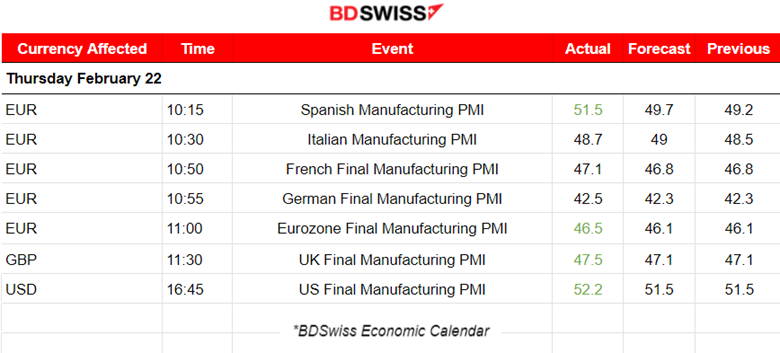

The Spanish PMI was reported to be 51.5, a turn to expansion, with rising new orders and output. Employment growth is also notable. Confidence in the future improved to its highest level for two years.

The Italian manufacturing sector remained in the contraction territory during February with a PMI reported at 48.7 points. Weak demand and lower order numbers caused the reduction of production volumes. Companies increased workforce levels during that time though.

The French production downturn continued falling at its weakest since January 2023. The reported PMI was just 47.1 points, at least an improved one, as contractions in output and new orders cooled significantly. Slower declines in purchasing activity and employment were also recorded.

The German manufacturing sector is worsening. The reported PMI is very low, at 42.5 points indicating that the Eurozone’s largest economy is having a good hit as rates of decline in manufacturing output and new orders have quickened.

The Eurozone manufacturing sector shows signs of recovery even though contraction of the sector continues. New orders and purchasing activity signalled lower rates of decline in close to a year in February. Production levels decreased midway through the first quarter, the rate of contraction held steady though.

UK PMI:

The U.K. manufacturing sector downturn continues. Weak demand and the Red Sea crisis were playing a significant role in the contraction. Disruption in production and vendor delivery schedules due to the Red Sea crisis created difficulties in delivering, driving up costs. Demand also remained weak, with new order intakes falling at the fastest rate since last October.

U.S. PMI:

In the U.S. the manufacturing conditions improve at the fastest pace since July 2022 according to S&P Global’s report. The sector experienced a quicker pace of improvement. A renewed increase in production and a quicker rise in new orders. The reported PMI figure is relatively high in expansion territory, with 52.2 points.

-

The ISM manufacturing PMI report though has shown different results. A PMI reported in contraction, at 47.8 points. Surprisingly low numbers contradicting the bulk regional manufacturing reports. The ISM manufacturing survey fell to 47.7 in February. The details show production contracted at its fastest rate since last July while new orders dropped back into contraction territory, while the employment component dropped.

-

The annual inflation estimate was reported at 2.6% in February 2024, down from 2.8% in January according to a flash estimate from Eurostat. The core figure was also reported lower, but higher than expected. The EUR depreciated at the time of the release with a moderate shock occurring. EURUSD dropped nearly 20 pips during that time.

-

The February UMich final consumer sentiment was reported lower, 76.9 vs the expected 79.6. Year-ahead inflation inched up from 2.9% in January, to 3.0% in February. For the second straight month, short-run inflation expectations have fallen within the 2.3-3.0% range.

Forex markets monitor

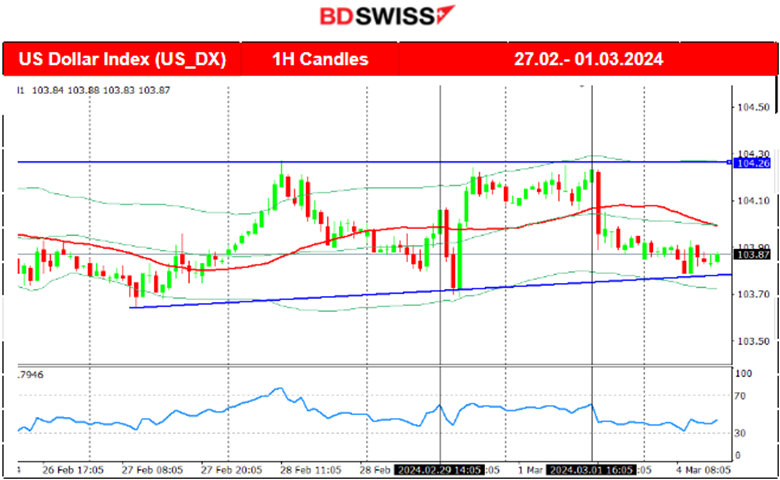

Dollar Index (US_DX)

The dollar index moved sideways with high volatility last week, not showing any significant weakening as expectations regarding interest rate cuts remain stable with high borrowing costs to be longer than expected. This might change next week with the labour data releases and Fed’s Powell statements. Consumer confidence dropped and orders for durable goods as well. However, the USD remained strong, always retracing to the 30-period MA during this period.

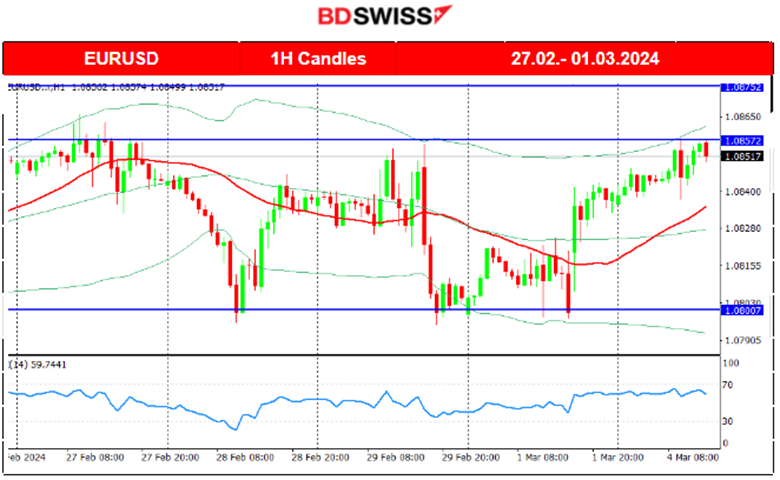

EUR/USD

The EURUSD path is greatly affected by the USD since the USD is usually the main driver. The European Central Bank expressed their intentions many times in regards to interest rate policy highlighting the fact that they are keeping interest rates high as long as needed until inflation is lowering with the desired pace, towards target. The EUR is currently not affected much by the news. The recent CPI Flash estimates figures on Friday showed that inflation in the Eurozone eased to 2.6% in February, but both the headline and core figures were higher than expected. Only a small impact was recorded in the market. However, in regards to U.S. related releases, we see that the market is quite sensitive to them, thus the big deviations from the mean. The pair is moving more to the upside currently as the USD weakens.

Crypto markets monitor

BTC/USD

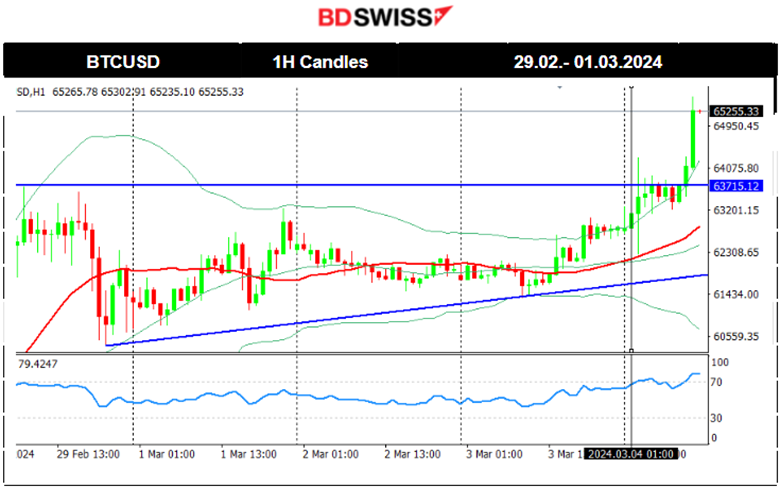

Bitcoin continues to the upside as it breaks more and more resistance. The largest crypto passes 65,000 USD for the first time since Nov. 2021. It is driven by expectations of exchange-traded funds’ robust demand and the upcoming halving event. It noted an Incredible demand from the U.S.-listed Bitcoin ETFs, which began trading on Jan. 11. Bitcoin has jumped about 186% in the last 12 months.

Next week's events (04 - 08.03.2024)

Coming up:

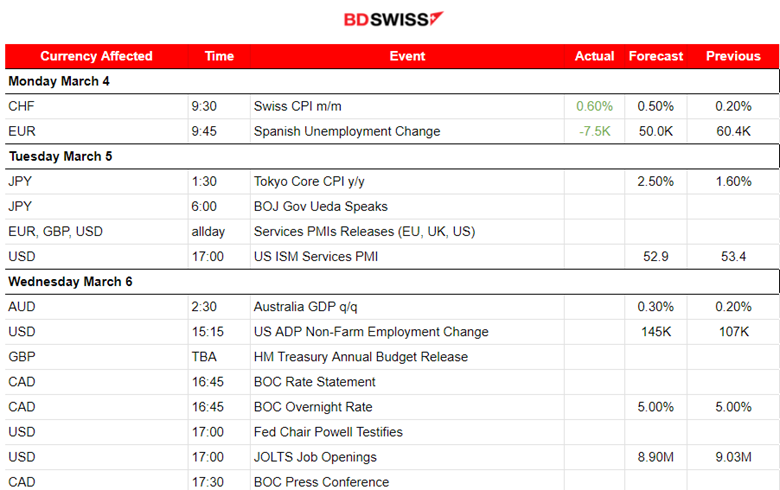

Two Central Bank Interest Rate Policy Decisions, Bank of Canada and European Central Bank.

Services Sector PMI releases completing the whole Business Conditions picture.

Canada and U.S. Labor Data Major Releases. NFP Expected lower.

Within the week statements from the Fed’s Powell will probably shake the markets.

Currency Markets Impact:

-

The Swiss consumer price index (CPI) increased by 0.6% in February 2024 compared with the previous month. Inflation was +1.2% compared with the same month of the previous year. CHF appreciated at the time of the release. USDCHF dropped nearly 25 pips and retracement followed.

-

The Tokyo Core CPI figure is going to be released on the 5th March and it is expected to be higher than previously reported. JPY pairs could see a moderate intraday shock at that time due to the sensitive importance of the data.

-

Services PMIs releases on the same data will take place potentially increasing volatility levels. The ISM Services PMI will probably cause an intraday shock affecting USD pairs. It is in the expansion area. A surprise heavy drop could cause U.S. dollar appreciation.

-

On March 6th, ADP report and JOLTs report, labour data releases, are going to take place affecting the USD pairs. This is a first look at how the labour market is progressing since the beginning of the year. The ADP is for January while the JOLTS job openings figure is reporting for Dec. The ADP Private sector employment is expected to be reported higher indicating a tight labour market view for early this year.

-

The Bank of Canada (BOC) will decide on interest rates on the same date and will potentially affect the CAD pairs. The press conference at 17:30 might cause more volatility pushing the pairs in one direction.

-

Fed Chair Powel will proceed to statements this week twice starting from March 6th. USD will probably be affected much by these and their effect could reach to the stock market as well causing high volatility.

-

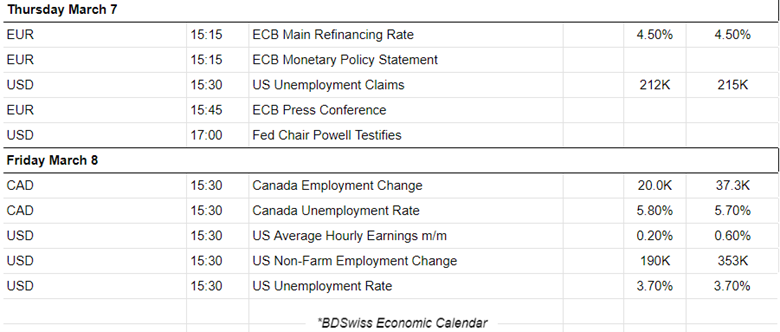

The ECB also decides on rates this week on the 7th of March. Interest rate policy is expected to remain unchanged and potentially cause an intraday shock to the EUR pairs. The press conference starts at 15:45.

-

U.S. Unemployment claims are expected to drop amid tight labour market conditions. However, the drop seems to be only small with the figure remaining close to 200K. Any significant deviation could only mean a light impact on the dollar.

-

The Fed Chair Powel will testify for the second time this week on the 7th of March at 17:00.

-

On the 8th we have the most important scheduled figure releases of the month. Canada’s labour market data releases along with the U.S. releases. Canada is expecting a slower increase in employment but a higher unemployment rate. The CAD pairs will probably be affected greatly by an intraday shock as the releases usually come out with surprises.

-

The NFP report is expected to show a lower figure and a steady unemployment rate suggesting that longer than expected unchanged interest rate policy, no cuts yet, and high inflation, cause cooling. Yet the numbers are high enough and the PMIs are strong for the U.S. to sustain elevated interest rates for longer. The impact on the USD pairs will be great in any case since market participants are expected to respond to the figures with high activity and volume. These figures will play a huge role in determining the future interest rate policy. Indications of strong cooling of the labour market could push the Fed to proceed with cuts sooner than expected.

Commodities markets monitor

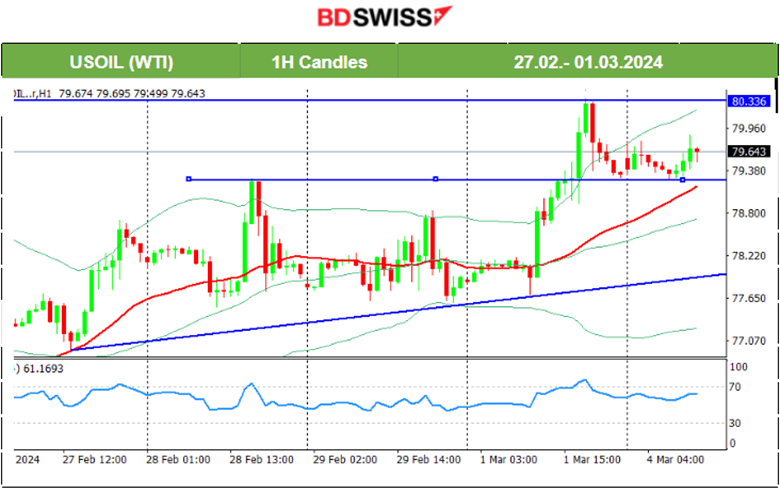

US Crude Oil

On the 28th Feb, the price was clearly on a short-term uptrend, however, after finding important resistance near 79.20 USD/b it reversed to the mean level at 78 USD/b. A sideways but volatile movement followed and that changed on the 1st March. The price jumped high reaching the resistance at 80.3 USD/b before retracing back to 79.3 USD/b. There is no clear signal in regards to where the price is headed. If the uptrend continues as the support remains strong, obviously the price could reach the high, 80.3 USD/b level, once more.

Gold (XAU/USD)

Since the 29th Feb, Gold shows this upside momentum with the price moving quickly and unusually upwards since the demand for metals saw an increase lately. The dollar is also showing weakness. Gold should come down if it passes the 2080 USD/oz support level. That would trigger the retracement. The 2088 USD/oz resistance is actually very important. Looking at the daily chart Bollinger Bands for volatility measure it actually tells us that Gold experienced quite unusual high volatility and movement to the upside. The question is, will the resistance 2088 USD/oz hold this week, causing the price to drop?

Equity markets monitor

NAS100 (NDX)

Price Movement

On the 29th Feb, all benchmark indices surged after the PCE report release showing a lower annual figure that caused the dollar to lose strength at that time. The momentum to the upside was strong enough to cause the index to move quite rapidly and further from the MA on its way up. Retracement followed today reaching the Fibo 61.8. A clear short-term uptrend for now. The RSI remains in the overbought area and if resistance holds, indices could see a drop soon. The alternative scenario is a sustainable jump after the NYSE opening that seems not so probable.

Author

BDSwiss Research Team

BDSwiss

BDSwiss is a leading financial institution, offering bespoke CFD trading and investment products to more than 1.7 million registered clients, in over 180 countries.