Key points

-

The announcement of Biden not seeking re-election injects higher uncertainty into the US presidential race, leading to increased cross-asset volatility as markets become more attentive to political narratives and campaign developments.

-

The US dollar may face downside pressure due to renewed focus on US macroeconomic factors and Fed policy. Trump Trades could also be at risk of an unwind.

-

Key catalysts to watch for Harris’s nomination to translate into electoral success and market stability include her first address, achieving internal Democratic alignment, her performance in debates, selection of a VP candidate, swing state polls, and her campaign’s effectiveness in energizing supporters and attracting women voters.

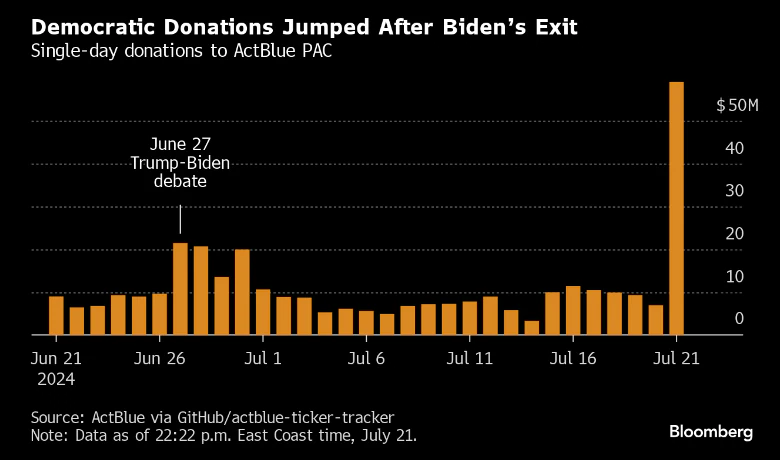

In a not-so-surprising move, President Joe Biden has announced he will not seek re-election in 2024 and has thrown his support behind Vice President Kamala Harris to become the Democratic nominee. Democratic State Party Chairs and leaders have come out in broad support for Harris’s nomination, and campaign donations also jumped higher in the immediate hours after the announcement.

This changes the stakes for the US presidential election, which was seemingly tilting in broad favor of the Republican Party and former President Trump after a series of events over the last few weeks, including the dismal performance of President Biden at the first debate, questioning his health, an assassination attempt on Trump, and a united front from his party at the Republican Convention last week.

But markets now have to brace for a more competitive race. Some of the Trump Trades could unwind, but not all. Some parts of the market could also be concerned about the odds of the first-time presidential candidate Harris to beat Trump. Let us assess what this closer race could mean for the markets:

-

More uncertainty, higher volatility: The race for the White House could become much more open in the run upto November, compared to the Republican “Red Wave” that started to be expected in the last week. Political narrative will come to the fore as a market driver, and markets will turn much more attentive to campaign headlines and polls. This could mean higher cross-asset volatility because of the uncertainty that has been injected into the election.

-

Softer US Dollar: The haven characteristic of the US dollar could take a backseat, and the greenback could go back to focusing on the US macroeconomic and Fed policy play. The Fed is in a blackout period this week ahead of its July 31 policy announcement, which means we won’t get updates on committee views that could fuel further rate cut speculation. Focus will therefore be on the PCE print due later in the week to assess whether disinflationary trends continue, and the Fed could potentially be more open about the possibility of a September rate cut. This could bring downside pressure on the US dollar.

-

Broader US indices focus on Fed and earnings: While volatility is spooked, policy direction could remain little different under Harris or Trump when it comes to fiscal spending. This means tech stocks and broader US indices could bring the focus back on key earnings that kick off this week, as well as the Fed rate cut expectations. Any dips in US tech stocks could continue to attract buyers if earnings and guidance continue to come in above expectations. Small cap stocks, that had a run higher amid expectations of tax benefits under a potential Trump presidency, could see some profit-taking and focus will be on the scope of soft-landing as well as earnings announcements.

-

Trump trades could unwind: Specific Trump trades, such as higher defense and energy stocks or declines in clean energy, could face bigger risks of an unwind. There could also be a temporary sense of relief in non-US markets, particularly those in China and Europe amid a weakening threat of tariffs. Trump company names such as Trump Media and Technology (DJT) could also see some pullback after 13% gains last week.

-

Bonds face more of the same: Fiscal restraint is unlikely, whoever becomes the next US president. This means markets will continue to worry about the ballooning fiscal deficit, and the long-end will likely continue to face selling pressure and the curve could steepen with market aligning on the possibility of a September Fed rate cut that could bring the short-end yields lower.

It is crucial to remember that we are still more than three months away from the US election, and over time, market reactions will depend on each candidate's potential policy changes. What we can be certain of now is the heightened political uncertainty, which may lead to increased volatility for investors.

Key catalysts to watch for Harris’s nomination to translate into electoral success and market stability may include:

-

Harris’ first address scheduled for 11:30am Washington time on Monday, 22 July.

-

Achieving internal alignment and presenting a united Democratic front (Democratic Convention scheduled from August 19-22).

-

Harris’ performance in the second presidential debate against Trump, scheduled for September 10.

-

Selection of Harris's vice-presidential candidate.

-

Poll results in key swing states.

-

Effectiveness of Harris's campaign in energizing existing Democratic supporters.

-

Success of Harris's campaign in attracting women voters.

-

Increase in campaign aid for the Democratic party.

Read the original analysis: Biden out, Harris in: Markets reassess US Presidential race and the Trump trade

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

Recommended Content

Editors’ Picks

EUR/USD holds gains near 1.0900 amid weaker US Dollar

EUR/USD defends gains below 1.0900 in the European session on Monday. The US Dollar weakens, as risk sentiment improves, supporting the pair. The focus remains on the US political updates and mid-tier US data for fresh trading impetus.

GBP/USD trades sideways above 1.2900 despite risk recovery

GBP/USD is keeping its range play intact above 1.2900 in the European session on Monday. The pair fails to take advantage of the recovery in risk sentiment and broad US Dollar weakness, as traders stay cautious ahead of key US event risks later this week.

Gold price remains on edge on firm prospects of Trump’s victory

Gold price exhibits uncertainty near key support of $2,400 in Monday’s European session. The precious metal remains on tenterhooks amid growing speculation that Donald Trump-led-Republicans will win the US presidential elections in November.

Solana could cross $200 if these three conditions are met

Solana corrects lower at around $180 and halts its rally towards the psychologically important $200 level early on Monday. The Ethereum competitor has noted a consistent increase in the number of active and new addresses in its network throughout July.

Election volatility and tech earnings take centre stage

/stock-market-graph-gm532464153-55981218_XtraSmall.jpg)

The US Dollar managed to end the week higher as Trump Trades ensued. Safe-havens CHF and JPY were also higher while activity currencies such as NOK and NZD underperformed.