Bank of Japan pauses but signals normalisation will continue

The Bank of Japan unanimously decided to keep its policy rate unchanged at 0.25%. Amid growing confidence in achieving its sustainable inflation target, the BoJ will closely watch the impact of FX movements on inflation. The timing of the next hike remains uncertain, but we see a chance of a hike in December.

Statement shows BoJ confidence in 2% inflation target, importance of FX moves on prices

In the statement, the BoJ assessed that the economy has recovered moderately, benefiting from accommodative financial conditions. On the price front, services prices increased but the effects of the pass-through of cost increases led by past rises in import prices waned and inflation expectations rose moderately.

In terms of the outlook, the BoJ expects the economy to grow above its potential, supported by moderate growth in the global economy and an improvement in consumption driven by solid income growth. In addition, underlying CPI inflation is expected to increase gradually, and inflation is likely to remain broadly in line with the price stability target.

In our view, the most interesting comment in the statement was presented at the end. It read, “With firms' behaviour shifting more toward raising wages and prices recently, exchange rate developments are, compared to the past, more likely to affect prices”. This means that FX movements have become more important to the BoJ when deciding policy. We believe this means that the virtuous cycle between income growth and consumption will eventually increase the resilience of consumption to inflation, giving firms more flexibility to set prices to reflect changes in input prices, including the impact of exchange rate movements.

The overall message of the statement was supportive of the continuation of policy normalisation, but it didn't give a clear indication of the pace of normalisation.

Governor Ueda suggests rate hike is NOT imminent

During the press conference, Governor Kazuo Ueda reiterated that the BoJ will continue to adjust the degree of easing if the price stability outlook is achieved and the economy improves in line with the BoJ forecast. In saying so, he clearly left the door open for further rate hikes in the future. However, he did not seem to suggest that there was any reason for the BoJ to rush into a rate hike. The BoJ will continue to assess the impact of two rate hikes this year, while upside risks to prices from yen weakness have eased. It has no timetable for the next hike, but he has a strong interest in October’s service prices and mentions the outlook for wages next year. This is in line with our view that October inflation will be the key to gauging the timing of the BoJ’s next rate hike.

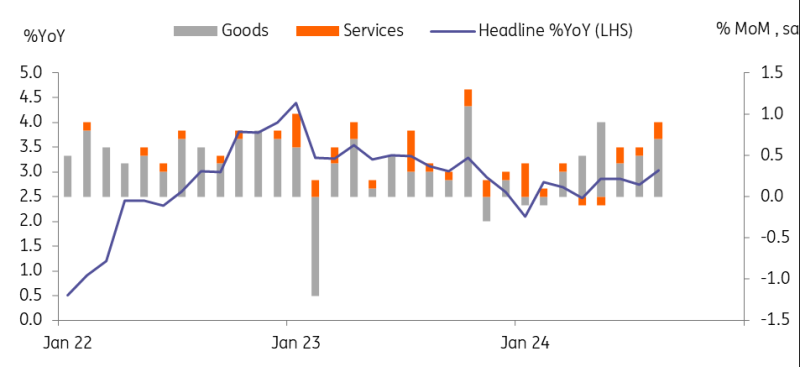

August inflation came in line with market view

Headline inflation rose 3.0% year-on-year (vs 2.8% in July) and core inflation excluding fresh food also rose 2.8% YoY (vs 2.7% in July). The pickup in August was already signalled by earlier Tokyo inflation data due to base effects related to the utility subsidy programme, thus it was not market-moving or would not have had much impact on the BoJ's policy decision. Fresh food prices rose sharply to 7.7% probably due to severe weather conditions and utility prices jumped to 15.0%. On a monthly basis, consumer prices rose 0.5% month-on-month, seasonally-adjusted, in August (vs 0.2% in July) with both goods and services prices increasing by 0.7% and 0.2%, respectively. We found it encouraging that service prices rose for the third month in a row, which supports a sustainable inflation trend.

Over the next few months, the restart of the utility subsidy programme in September and the usual price increases in October may cause inflation figures to fluctuate. In September, inflation is expected to ease quite meaningfully to the mid-2% range as the government re-introduces the temporary energy subsidy programme for the summer. October is typically the month for second-half price increases, so it is worth looking at whether the recent solid wage growth and corporate earnings have changed companies' price-setting behaviour.

Service prices continued to rise in August

Source: CEIC

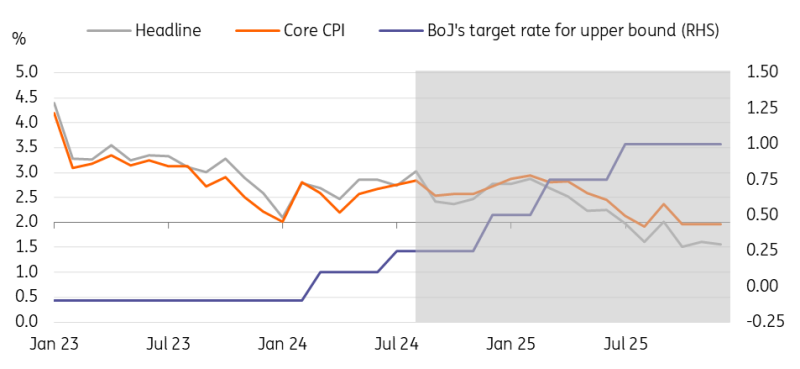

BoJ outlook

Having listened to Governor Ueda’s remarks and read the statement, we believe that the BoJ is in no hurry to raise rates, but the option of a December hike is still on the table. The recent JPY appreciation has clearly eased the BoJ’s concerns about the negative impact of rising import prices, so the probability of an October hike is quite low. However, demand-driven price increases are expected in the coming months, and this will be confirmed in the October inflation data. Thus, the BoJ will take a wait-and-see approach for a few months to analyse inflation developments. We believe that the BoJ is concerned about financial market stability as well. While short-term market jitters will not prevent the BoJ from normalising policy, the pace of JPY appreciation and its impact on inflation should be carefully monitored. In that sense, the Fed’s efforts to avoid a recession will work in favour of the BoJ taking its time and responding cautiously. Going forward, the key data developments should be October inflation along with wage growth and household consumption data.

BoJ and CPI outlook

Source: CEIC, ING estimates

USD/JPY corrects higher

USD/JPY has corrected higher on Governor Ueda's press conference. Probably two factors have driven that move: the first is the sense that the BoJ is in no hurry to deliver the next rate hike and still assesses financial markets as unstable. The second was Governor Ueda's comments that upside risks to prices from yen weakness were fading - suggesting that the BoJ was a little less sensitive to USD/JPY strength than it had been earlier this year. As we write this, USD/JPY is up some 1.2% since Governor Ueda started speaking.

Yet we think the medium-term USD/JPY trend is down. Global interest rates (with a few exceptions such as in Brazil) are converging on the low interest rates in Japan. US exceptionalism is waning and the Federal Reserve has started a front-loaded easing cycle. A BoJ hiking cycle is certainly a bonus, but not a necessity for a lower USD/JPY. And we think the yen offers investors some protection should US hard landing fears materialise and hit equity markets.

We doubt USD/JPY holds any gains over 145 near term and remain happy with a year-end target at 140 - with risks to the downside.

Read the original analysis: Bank of Japan pauses but signals normalisation will continue

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.