Australian Employment Preview: Will labor market upturn save the aussie?

- Australia to add 35K jobs in August, Unemployment Rate to steady at 3.4%.

- RBA’s Lowe said further rate hikes required but not on a pre-set path.

- Another dismal Australian jobs report could trigger a fresh downside in AUD/USD.

Australia surprisingly shedded jobs in July but that failed to dissuade the Reserve Bank of Australia (RBA) from delivering on the third straight half-point hike earlier this month. AUD/USD, however, was unable to find any comfort amid dovish hints from Governor Philp Lowe.

Australia’s labor market may witness an upturn in August, the latest employment report due to be published by the Australian Bureau of Statistics (ABS) is likely to show this Thursday. Will it revive aggressive RBA tightening bets and rescue AUD bulls?

Jobs creation amid dovish RBA

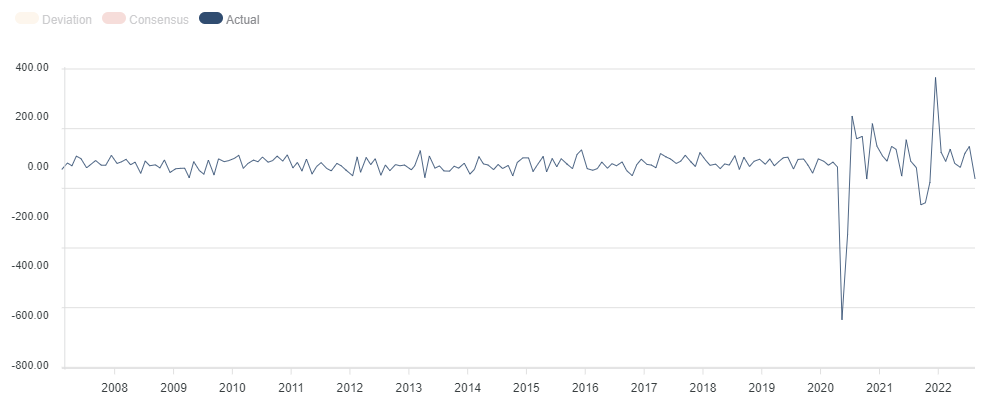

Having witnessed an unexpected slump in the employment sector in July, the Australian economy is expected to see 35K jobs created in August. The Unemployment Rate is likely to stay unchanged at a 48-year low of 3.4%. The Participation Rate is forecast to have risen to 66.6% last month when compared to the previous figure of 66.4%. In July, Full-Time Employment led the decline, dropping by 86.9K while part-time positions climbed by 46K.

Source: FXStreet

Australia’s second-quarter inflation rose 6.1%, the fastest annual pace since 2001 as consumers paid more for everything from fuel to food. The country’s business confidence picked up for a second straight month in August, the latest NAB survey showed on Tuesday.

However, the previous slump in the Australian labor market contributed to a gradual increase in wage growth. The wage price index grew 2.6% in Q2, less than half the pace of inflation, which underscored the cost-of-living crisis. A slowdown in the economic activity amid red-hot inflation prompted the RBA to hike rates by 50 bps in September vs. expectations of a 75 bps increase pre-July employment data.

RBA Governor Lowe said the bank’s board “expects to increase interest rates further over the months ahead but it is not on a pre-set path,” maintaining a language similar to the August statement.

Responding to the Q&A session at the Anika Foundation Fundraiser last week, Lowe said that it is “very possible wage growth does not pick up much further.” Further, RBA Chief hinted at a probable slow down in the bank’s tightening pace after he noted that the “neutral cash rate is at least 2.5%, adding that they are “closer now to estimates of neutral.”

Therefore, the August employment data is crucial to gauging the size of the RBA’s next rate hikes and whether the bank could bring a pause to its tightening cycle.

Australia’s labor market report could offer the RBA the option of returning to quarter-percentage increases.

Trading AUD/USD with jobs data

The Fed-RBA policy divergence widened after Tuesday’s hotter US inflation data, as the upside surprise in the core Consumer Price Index (CPI) and less than expected softening of the headline CPI revived bets of aggressive Fed tightening in the months ahead while dampening speculation of a dovish Fed pivot.

The US dollar rallied hard against its major rivals and smashed AUD/USD to weekly troughs near 0.6750.

Should the employment data surprise to the downside once again, it will squash hopes for a 50 bps October rate hike by the RBA. In such as case, AUD/USD could revisit July lows sub-0.6700.

A big beat on all labor market indicators is needed to rescue AUD bulls, which could fuel a fresh upswing in the pair towards a critical resistance at around 0.6850.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.