![]() ING Global Economics Team

ING Global Economics Team

ING Economic and Financial Analysis

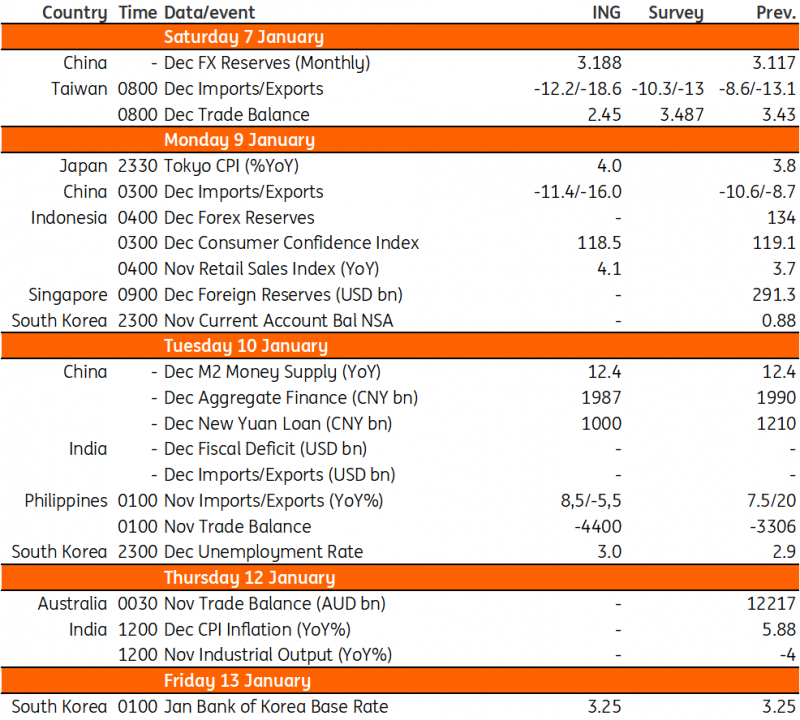

Next week’s data calendar features China's growth numbers, inflation readings from Australia and India, plus a key central bank meeting.

Inflation finally on the downtrend?

The new monthly Australian inflation series should show a further small decline in the inflation rate to 6.8% year-on-year, down from October’s 6.9% rate – still too high for the Reserve Bank of Australia to stop tightening, but moving in the right direction.

And in India, further falls in food prices and stable gasoline should bring the price level down by 0.1/0.2% month-on-month, although similar falls last year mean that the inflation rate could hold up at around 5.9%YoY for a second month – still, within the Reserve Bank of India’s target range and indicating that we may be closing in on peak rates.

China activity and loan data due in the coming days

China will announce loan data between 9 and 15 January and activity data and GDP data between 10 and 27 January. Loan growth should have slowed in the last month of 2022 even after the People's Bank of China cut the required reserve ratio (RRR) to absorb liquidity. The impact of the RRR cut in December should be reflected in loan growth data for January and support economic activity post-reopening.

China also reports activity data and we expect retail sales to face a deeper contraction on a yearly basis. Meanwhile, industrial production could turn from positive growth to mild contraction in December. This suggests that growth was supported mainly by fixed-asset investments for the period. As a result, GDP growth for the fourth quarter of 2022 should fall into a slight year-on-year contraction.

BoK could surprise with a pause

Bank of Korea (BoK) will meet next Friday. The market expects a 25bp hike, but we maintain our minority view that the BoK will likely stand pat this time. Since the last meeting, both inflation and inflation expectations decelerated quite meaningfully while the Korean won stabilised under the 1300 level despite a widening yield gap between the US and Korea.

The BoK is expected to use the rate hike card more carefully as there is little room left to raise interest rates in this cycle given sluggish exports and economic activity. However, given the recent rise in gasoline and power prices, upside risks remain high and thus the BoK should retain a hawkish tilt despite the pause.

Philippines exports likely to reverse recent surprise gain

Exports are expected to revert to contraction following a surprise jump in the previous month. Electronics form the bulk of outbound shipments from the Philippines and given slowing global demand we could see the overall exports sector fall back into the red. Imports on the other hand should continue to expand, resulting in the trade deficit widening to roughly $4.4bn.

Key events in Asia next week

Source: Refinitiv, ING

Read the original content: Asia week ahead: Inflation reports from Australia and India and Bank of Korea meeting

Content disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/content-disclaimer/

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains near 1.0400 after US inflation data

EUR/USD holds its ground and trades in positive territory near 1.0400 on Friday. The weaker-than-forecast PCE inflation data from the US and the improving risk mood makes it difficult for the USD to find demand, supporting the pair heading into the weekend.

GBP/USD climbs to 1.2550 area on renewed USD weakness

GBP/USD extends its rebound from multi-month lows and trades near 1.2550. The US Dollar stays on the back foot after softer-than-expected PCE inflation data, helping the pair edge higher. Nevertheless, GBP/USD remains on track to end the week in negative territory.

Gold rises above $2,620 as US yields edge lower

Gold extends its daily rebound and trades above $2,620 on Friday. The benchmark 10-year US Treasury bond yield declines toward 4.5% following the PCE inflation data for November, helping XAU/USD stretch higher in the American session.

Bitcoin crashes to $96,000, altcoins bleed: Top trades for sidelined buyers

Bitcoin (BTC) slipped under the $100,000 milestone and touched the $96,000 level briefly on Friday, a sharp decline that has also hit hard prices of other altcoins and particularly meme coins.

Bank of England stays on hold, but a dovish front is building

Bank of England rates were maintained at 4.75% today, in line with expectations. However, the 6-3 vote split sent a moderately dovish signal to markets, prompting some dovish repricing and a weaker pound. We remain more dovish than market pricing for 2025.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.