Asia week ahead: Central bank decisions set to dominate

Central bank decisions will dominate the week ahead in Asia, with policy announcements from the Bank of Korea, Bank Indonesia and People’s Bank of China.

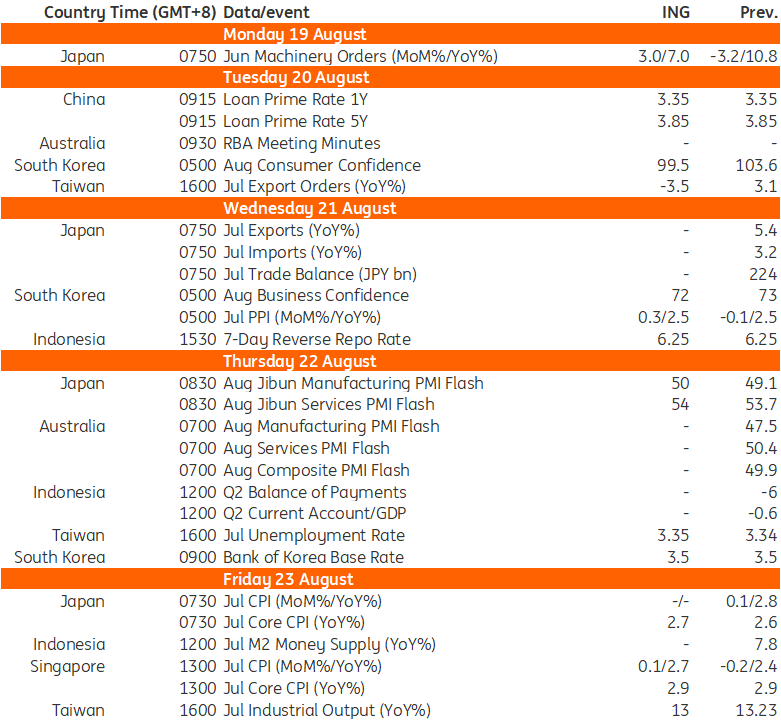

China: Quiet after the data storm

It is a quiet week ahead for China after it recently concluded its major monthly data releases. There will be an announcement on the loan prime rates on Tuesday. No change is expected after the MLF and 7-day reverse repo rates were left unchanged so far in August.

Taiwan: Export orders to slide back into contraction

Taiwan will release its export orders and industrial production data in the upcoming week. Export orders will be released on Tuesday, and we are looking for year-on-year growth in July to decline back into contraction of around -3.5% as base effects turn less supportive in the second half of the year.

Industrial production data for July is scheduled for release on Friday. Here we expect YoY growth to remain in the low teens. This growth will likely moderate in the months ahead. Taiwan also publishes its unemployment rate on Thursday, which has been stable at 3.3-3.4% over the past year.

Korea: BoK meeting - no change but views on housing and debt will be important

The Bank of Korea will meet on Thursday for its policy decision meeting, and the market expects no change. But the meeting will nonetheless be closely watched to see what the BoK thinks and communicates to the market about the recent rise in household debt and house prices.

Survey data for consumers and businesses should be soft, reflecting recent market volatility and heightened uncertainty on the policies of major central banks.

Japan: Flash PMIs and inflation to rise

The flash PMIs should improve due to a positive outlook for service activity despite the recent volatility in the JPY and the sharp drop in equity markets. Rising semiconductor and auto exports and core machine orders data also hint at a rise in manufacturers' sentiment. Meanwhile, inflation is expected to reaccelerate in July, which was already suggested by Tokyo’s earlier inflation data.

Rest of Asia and Australia

On 20 August, we will see the minutes of the August Reserve Bank of Australia meeting, in which we will get a glimpse of just how close the RBA came to hiking. Our guess? Quite close.

Indian PMI data for August will continue to run strong. 60.2 is our forecast for services and 58.0 for manufacturing. Both could be slightly lower than the July figures but remain consistent with ongoing strong growth.

Bank Indonesia is meet to set its rates policy on 21 August. While there is no expectation for a rate cut, the recent strength in the IDR exchange rate and recent BSP rate cut may make easing a more realistic prospect than the unanimous consensus suggests. Inflation remains under control and a rate cut isn’t unthinkable. It remains more likely that the first cut will come after the Federal Reserve has started to ease.

In Singapore, CPI inflation for July will likely show a slight increase from 2.4% YoY in June to 2.7% in July, interrupting its erratic trajectory lower. The core rate, currently 2.9% YoY, is probably of more interest to rate setters at the Monetary Authority of Singapore.

Key events in Asia next week

Source: Refinitiv, ING

Read the original analysis: Asia week ahead: Central bank decisions set to dominate

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.