Another difficult year for retail, with Tesco and M&S standing out

The UK retail sector has faced plenty of challenges over the last few years navigating the lockdowns of the Covid pandemic, only to be hammered again by the impact of Russia’s invasion of Ukraine as the costs of carrying out business soared.

2022 saw big share price falls in the likes of Next, which slipped to 30-month lows, along with Marks & Spencer, while Primark owner Associated British Foods saw its share price fall to its lowest level since 2012, after headline inflation peaked at a 40-year high of 11.1%, in the month of October.

These lows proved to be a significant turning point for a lot of these retailers given the pessimism surrounding the cost of living, with UK consumer confidence sinking close to record lows of -49.

Given that backdrop the Bank of England was predicting that the UK was on the cusp of a 2-year recession, as consumers faced a perfect storm of sharply rising rates, and an energy price cap that had seen a big rise from the previous one.

Since those series of low points in October 2022 the picture for the UK retail sector has improved quite considerably even allowing for the fact that over the past 2 years, we’ve seen some notable retail collapses, while the fall in energy prices to more bearable levels has helped on the margins.

In its latest report published last month, the Centre for Retail Research said that the retail sector had been in a near state of “permacrisis” since 2009, with 790 store closures in 2023 alone. This trend of store closures and business failures has continued into 2024, with another 602 store closures so far year to date and 33,000 job losses on top of the 37k seen in 2023.

Despite these dire statistics there have been pockets of the retail sector that have managed to outperform despite the increasing burdens being imposed on it, not only by a changing retail dynamic in the form of online sales, but also increased costs as well as higher taxation.

The recent budget from the new UK government saw multiple retailers claiming that the new measures on the minimum wage, as well as changed national insurance thresholds would add millions of pounds to their costs.

We’ve also seen it in the form of increased cost provisions in the latest trading updates from the likes of Tesco, Sainsbury, as well as Next, Kingfisher, Frasers Group and JD Sports.

UK retail sector YTD

Source: CMC Markets

As can be seen from the above graphic, the likes of boohoo group and ASOS who performed well during the pandemic, due to their online presence have struggled to adapt struggling throughout 2023 and have continued to do so throughout this year as well.

The weakness of both companies has allowed the bigger players like Mike Ashley’s Frasers Group to gain a foothold, with a view to shaking up the performance with Ashley currently involved in a serious disagreement with Boohoo management over how the business is run.

The rest of the sector and the FTSE 350 General Retail Index were looking good for some solid gains this year, up around 12.5% by mid-September.

Since then, however, the wheels have come off a touch with the index giving back those gains, with weakness in the likes of JD Sports, Frasers Group and Primark owner Associated British Foods sliding back.

Next shares also came under pressure in the aftermath of their September update, but that was only because the shares briefly put in a fresh record high, after the retailer issued yet another guidance upgrade to sales and profits, with the sell off probably put down to some natural profit taking.

While the rest of the sector is struggling it is Next, alongside Marks and Spencer which is helping to keep the retailers index afloat with further strong gains this year on top of the strong performance in 2023.

It is clear that the deteriorating economic outlook, as well as the decline in business and consumer confidence in recent weeks has undermined a lot of the early year momentum, we carried over from 2023 for a lot of the retail sector, with multiple warnings that the recent budget increases on National Insurance and the minimum wage, could well have the unintended consequences of accelerating automation and the shedding of jobs.

The bigger question is what happens next, and it is hard to see too many silver linings unless you’re in food retail, which brings us to M&S which has a foot in both camps so to speak.

Marks and Spencer looks set to be the best performing retail stock for the second year in succession, the shares taking out the 2022 peaks at the end of last year, and in November briefly pushed through the 400p area for the first time since May 2016.

The turnaround plan which started under previous CEO Steve Rowe has gone from strength to strength under Stuart Machin, with the restoration of the dividend last year a key milestone.

In its latest H1 report, profits before tax rose 20.4% to £391.9m from £325.6m, with food sales as well as general merchandise contributing to the revenue and profit uplift.

Statutory revenue rose to £6.48bn, a 5.7% increase on the previous year with both the food business and the clothing business seeing improved margins.

In Food operating profit margin increased to 5.1% from 4.1% while market share increased 30bps to 3.7%. Over in clothing it was a similar story with operating profit margins steady at 12%, while market share was up 90bps to 10.3%.

The transition in this business has been remarkable in so much that food now accounts for nearly two-thirds of revenue at £4.17bn, with clothing at just over £2bn, highlighting how important the food side of the business has become to the business as a whole.

On the outlook CEO Machin said the business was on track to deliver £500m in savings by FY28, while issuing a cautious outlook, due to persistent cost inflation, a trend that is expected to persist in H2.

Next PLC is also doing well and has had another strong year, coming off the back of a strong 2023 when it raised its full year profits guidance four times, the challenge in 2024 was always going to be to repeat the trick at a time when cost pressures are likely to be at the forefront of customers minds.

Nonetheless while 2024 has seen its UK business growth remain flat at 1%, the overseas business has performed much better with growth of 22.8% which helped push H1 total group sales up by 8% and full price sales up by 4.4%. H1 total group sales were £2.95bn, while profits before tax came in at £452m.

Because of this outperformance Next says it expects to see full year profits rise to almost £1bn, with an expectation that full year group sales will increase by 6.6%, and full price sales by 4, with the result that we briefly saw the share price push up to new record highs, helped by a seemingly unerring ability of this retailer to consistently update its guidance.

All eyes will now be on the next update for Next which is due in the first full trading week of 2025, when we will get an insight into whether we’ll a 9th successive quarterly upgrade of its sales and profits target.

For the rest of the sector, it is looking like more of a struggle with both Frasers Group and JD Sports seeing share price losses of in excess of 25%.

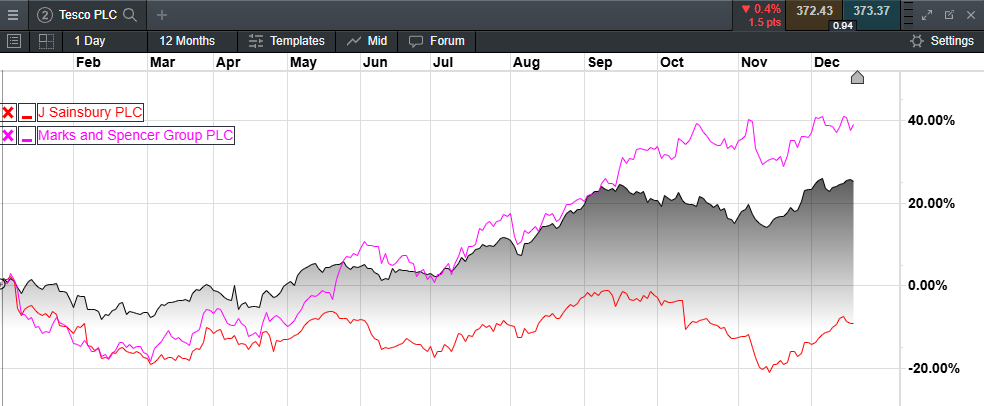

As far as food retail is concerned the UK food sector continues to be dominated by the big two of Tesco and Sainsbury, with Asda coming in third, although there is a contrast to how both Tesco and Sainsbury have performed this year.

The likes of Aldi and Lidl continued to eat into the market share of both with these two minnows continuing to expand and now accounting for a combined 18.1% of the UK market combined, according to recent Kantar data.

Sainsbury and Tesco share price performance YTD

Source: CMC Markets

At its most recent trading update Sainsbury H1 profits saw an increase of 3.7% to £503m, with Q2 like for like sales up by 4.2%, pushing the H1 number up to 3.4%.

The supermarket maintained its full year guidance, of underlying operating profit of just over £1bn, with growth of between 5% and 10%, however adopted a rather downbeat tone warning that the recent budget would £140m to its tax bill in the next tax year, while also warning the tax changes would likely be inflationary.

The interim dividend was kept unchanged at 3.9p per share, with the shares still unable to reverse the sharp losses seen in October on reports that the Qatar sovereign wealth fund sold £306m of its long-held stake in the business, reducing its 14% holding to below 5%.

Tesco shares have once again done well this year building on their gains in 2023, with the UK’s biggest supermarket seeing gains of over 200% since the end of 2022, and pushing to their best levels since 2014.

When Tesco reported in October H1 group sales were up by 3.5% to £31.46bn, helping to drive a 15.6% increase in adjusted operating profit to £1.65bn.

H1 revenue across all the businesses saw an increase in revenues to £34.77bn, and H1 profits rose by 13% to £1.6bn, with Tesco Bank adding £94m in adjusted operating profit. H1 profits after tax rose by 13.1% to £1.05bn.

Tesco also raised its guidance for adjusted full year operating profit by £100m to £2.9bn, while pledging to complete the £1bn share buyback by April 2025. The sale of the banking operations to Barclays for £700m is expected to be done by the end of this year, with the majority of the proceeds being used to buyback more shares in the months ahead.

In the most recent Kantar survey both supermarkets outperformed the wider market, helped by the Nectar and Clubcard pricing they have succeeded in keeping the likes of Aldi and Lidl at bay, who appear to be cannibalising the likes of Asda and Morrison in terms of market share, with Asda now holding 12.5%, compared to a few years ago when it was neck and neck with Sainsbury.

If there was one thing to take away from the recent Kantar survey it appears to be that consumers still have the appetite to go out and spend with the number of shopping trips hitting a 4 year high of 480m, with October 2024 being the busiest month since March 2020, when everyone was loading up on toilet roll.

Nonetheless we still don’t appear to be back at pre-covid levels yet, and with the recent concerns about higher costs, as well as rising evidence of a consumer slowdown it could well be some time before we do.

The inflation outlook continues to look uncertain with any new rate cut from the Bank of England unlikely to come much before the end of Q1 next year.

To conclude the economic outlook for 2025 remains very uncertain with various economic forecasters predicting an immensely challenging economic outlook.

There are reasons to be optimistic however with close to its lows, and if we do see further rate cuts that is likely to be a welcome relief for household finances, and mortgage rates especially.

Author

Michael Hewson MSTA CFTe

Independent Analyst

Award winning technical analyst, trader and market commentator. In my many years in the business I’ve been passionate about delivering education to retail traders, as well as other financial professionals. Visit my Substack here.