Amazon, Alphabet & Stimulus top boost to the equity market

Stock markets extended their rally overnight and yields climbed higher. 10-year rates jumped more than 11 bp in New Zealand after the country approved the first Covid-19 vaccine. The ongoing earnings season is adding support and better than expected revenue estimates from Alphabet and Amazon helped to bolster confidence.

The major indexes climbed back toward recent highs, unperturbed by the threat of six more weeks of winter as Punxsutawney Phil saw his shadow. Treasury yields have lifted 0.9 bp to 1.1%, while JGB rates are up a modest 0.1 bp at 0.05%. The JPN225 gained 1% and the ASX 0.9%, although Hang Seng and CSI 300 are currently both marginally lower after the People’s Bank of China drained some funds from the financial system. The GER30 and UK100 futures are up 0.4% and 0.3% respectively.

The earnings season is in full swing now and so far hasn’t dented the renewed surge in risk appetite and confidence that vaccination programs will help the global recovery to strengthen this year. Wall Street had another very good day yesterday and the move higher in stocks is set to resume today, also helped by hopes of accelerated fiscal stimulus in the US. Against that background any lingering expectations of additional rate cuts in Europe are being priced out, which should keep pressure on core EGBs.

Headlines

-

President Biden and Senate Democrats look to pass the $1.9 tln relief bill via “reconciliation” (51 votes) and bypassing the Republicans.

-

US: New cases of Covid-19 fall for a 3rd week in a row – the first time this has been seen since September.

-

According to IBES data from Refinitiv: More than 80% of reports from USA500 companies so far have surpassed analysts’ earnings expectations, with 97% of reports from technology companies beating.

-

Amazon — Shares of the retailer were up 1% in after-hours trading on the back of quarterly results that beat analyst expectations. Amazon reported earnings per share of $14.09 on revenue of $125.56 billion. Analysts polled by Refinitiv expected a profit of $7.23 per share on revenue of $119.7 billion.

-

The company also announced that CEO Jeff Bezos will move to the role of executive chairman in the third quarter and be replaced by Amazon Web Services head Andy Jassy as chief executive officer.

-

Alphabet — Alphabet shares jumped 6% after the tech giant reported better-than-expected results for the previous quarter. The company reported earnings per share of $22.30 on revenue of $56.9 billion. Analysts polled by Refinitiv expected a profit of $15.90 per share on a revenue of $53.13 billion.

-

GameStop — Shares of the brick-and-mortar video game retailer continued to tumble in after-hours trading on Tuesday following a 60% drop in the regular session. Shares are down more than 70% this week as the short squeeze trade unravels.

-

Amazon, Alphabet, Microsoft and Salesforce are all investing in a $28 billion start-up company that crunches big data.

-

China Caixin services PMI dropped to 52.0 in January from 56.3.

-

Japan Jan Services PMI fell to 46.1 from 47.7 in December.

-

New Zealand Q4 2020 Unemployment rate 4.9% (vs. expected 5.6%).

-

BOJ Deputy Governor Wakatabe watered down expectations of much change from the bank’s monetary policy review due next month.

Forex Market

EUR – decline continues with the asset trading below 1.2100. S1 at 1.2007.

GBP – fell against the USD but remains above 20-DMA. S1: 1.3615, PP: 1.3660, R1: 1.3715.

JPY – lifted to 105.05, as the Yen weakened.

AUD – founds floor at 50-DMA (0.7600).

CAD – tumbled in 4-day range. Currently above S1 at 1.2750.

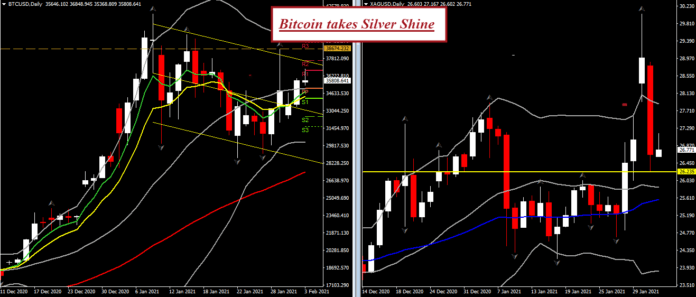

Silver – sharp reversal, filling the week’s gap. CFTC and CME warnings helped to quell price speculation.

USOil – at $55.20 with the move higher due to signs of tightening supply.

Today: Focus mainly on fundamentals which will be a focal point near term with ADP and ISM services reports today, and the jobs report Friday. Also Eurozone inflation data and final readings for Eurozone and UK Services PMIs meanwhile will act as a reminder that for now virus restrictions continue to weigh on overall activity and keep Europe on track for a recession over Q4/Q1.

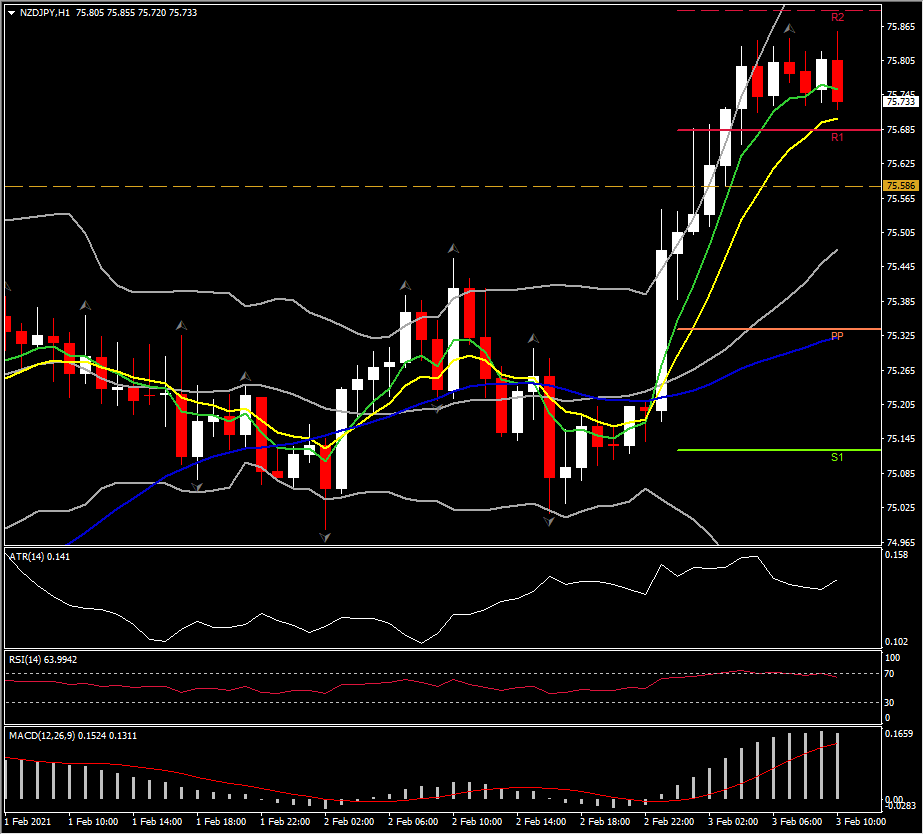

Biggest Mover NZD/JPY (+0.41% as of 08:00 GMT)

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in