All eyes are back on central banks and the loosening of conditions everywhere

Outlook

All eyes are back on central banks and the loosening of conditions everywhere. On top of China’s new cuts, in Sweden, the Riksbank cut by 25 bp as expected and hinted rates will fall some more, maybe even by 50 bp. Tomorrow it’s the Swiss National Bank. Emerging markets are on the rise as the advanced economy banks cut. In the US, the “bad” Conference board consumer confidence survey was taken as the trigger for bettors to go for another 50 bp cut. And yesterday’s lousy eurozone data has pushed up the probability of an Oct rate cut by the ECB to 60% (Bloomberg).

Rate cut mania is starting to get into full swing.

As noted above, the latest mini-panic is the Conference Board consumer confidence survey showing a bigger drop than expected. August was revised from 103.50 to 105.6, so the fall in Sept to 98.7 looks even bigger. Disregarding the big revision is error number one. Then there’s the simple fact that consumers do not know enough about the economy to voice an informed opinion. These are the same people who are undecided about voting for Trump.

Second, the survey was taken before the Fed’s recent big cut. Third, the survey is full of inconsistencies. There is rising worry about the job market—but a higher percentage plan to buy a house in the next 6 months. There was a small increase in the share of consumers intending to buy cars, refrigerators and clothes dryers over the next six months, too.

A critical component is the “Labor Differential Index,” which is the gap between the number of respondents who say that jobs are plentiful vs. those that say jobs are hard to get. Respondents say jobs are harder to get. On what basis are they saying that? How do they know?

Analysts have taken the report apart seventeen different ways, but we say it’s waste of time. If the survey had been taken after the big rate cut, it would have come out entirely different. This is, of course, the other problem with surveys, on top of having qualified people to survey in the first place—they change all the time. And on the subject of qualifications, even the big economist surveys by the likes of Bloomberg and Reuters are wrong as often as right, sometimes by vast amounts.

The real lesson here is that markets have become addicted to panic rush and manufacture panic where none is called for. This can be dangerous, as we saw it the yen carry trade freakout in early August. See below.

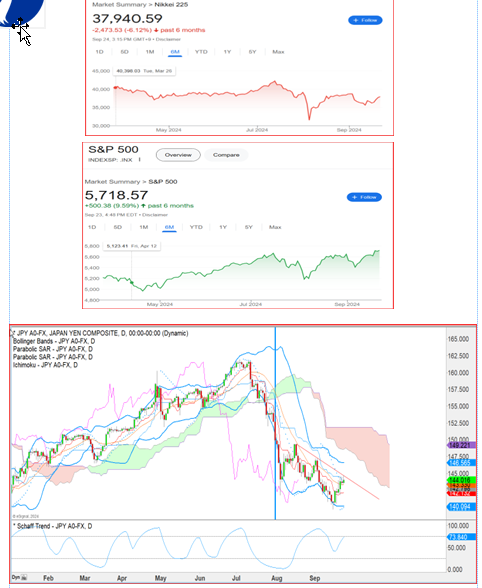

Japan is about to get a new top-party leader and government, but this should not have any effect on the BoJ. One of the hardest things to understand in many years is what the hell Japan is doing. The BoJ ended zero rates and hiked a tiny amount at end-July. It also announced it would cut in half its bond-buying. This set off a frenzy of carry-traders jumping ship and reached as far as the S&P, which fell from 5522.30 on 7/31/24 to 5186.33 on Aug 5 (6%). The Nikkei fell from 39,101.82 to 31,458,42 over the same 5-day span, or 20%. Other equity markets tagged along.

This was only the second rate change since 2007—in March, the BoJ had raised rates from zero to a range of zero to 0.10%. The July change took the range from 0.10% to “around” 0.25%.

As we wrote at the time as the postmortem was being conducted, nobody knows how big the carry trade might be. Reuters wrote “Using the narrowest definition of a pure currency carry trade, analysts point to the $350 billion of short-term external loans by Japanese banks as one estimate of yen-funded trades in the world.

“That number could be an exaggeration if some of those loans are commercial transactions between banks or loans to foreign businesses needing yen.

“But it could be also understating the actual size of yen carry trades because there could be billions of yen the Japanese themselves have borrowed to invest in markets at home.

Actual positions could be amplified because of how hedge funds and computer-driven funds use leverage.

“Add to that the massive investments Japanese pension funds, insurers and other investors have made abroad. Japan's foreign portfolio investments were 666.86 trillion yen ($4.54 trillion) at the end of March, Ministry of Finance data shows - more than half in interest rate-sensitive debt assets, albeit most of it long term.”

Can we assume that the S&P, Nikkei and other asset classes got hit with unwinding? Note that the US 10-year yield fell from 4.1050 on July 31 to 3.7830 at the close on Aug 5, the lowest of the year at the time. The subject of contamination fell into the mud and has not been brought up again.

As for the dollar/yen, it was already falling when the rate hike news was announced indicating (probably) that some market players saw it coming. The vertical line on the chart is the rate hike announcement date. The dollar fell a little more for a few days, bounced, and then resumed to an even lower low (139.58 on 9/16/24). Quite a journey from the highest high only about two months earlier at 161.76 (7/11/24).

We can note it was widely assumed that the BoJ intervened during this period, something borne out by now-redacted BoJ data (thanks to a Reader for the report).

The BoJ was shocked that it had triggered such a wild response and was being blamed for causing global market uproar. It all but bowed in apology. Yesterday the story came out that the BoJ intends to stay the course but is in no hurry and will spend time looking at prices, markets and what’s going on in other countries. The bank will raise rates if inflation does rise, as expected, but Gov Ueda is in no hurry.

This whole thing is remarkable. Why is everyone not talking about it? The first answer is that we do not understand financial market contagion. Ever since Long-Term Capital, where Nobel prize winning economists made an enormous error of judgment that took a small issue into a global crisis needing a central bank bailout, we have made no real progress on the subject of contagion.

This leads us right back to that fickle thing, market sentiment. It is made up of reasonable economic projections, sensible interpretation of historical comparisons, wishful thinking, crackpot theories, chart interpretation and misinterpretation, and a dozen other things well past logic.

So, what’s next? Well, the law of currencies tracking the change in relative interest rate differentials would indicate that the yen returns to the 150-160 level as the BoJ stays its hand to avoid losing face a second time. That’s assuming the carry traders have returned in force, and we have no evidence of that. This is so even as the Fed intends to cut some more but the yield curve has de-inverted and the drop in short-term rates is fairly slow. As of yesterday, the 1-month money market rate was still 4-4.5%. This is a whole lot better than 0.25% in Japan, if less than before. So far.

Forecast

Risk appetite tends to soar when everybody and his brother is cutting interest rates (and interpreting data to confirm the bias for more and bigger cuts). We could hit a brick wall when we got both US and Japanese (Tokyo) inflation on Friday. The core PCE is expected up a few points, which might moderate rate cut mania. This does not necessarily mean respire in the attack on the dollar, though. Sentiment is firmly in that camp even when not warranted. We might get a minor pullback from overbought conditions in some places (AUD).

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat