ADP Jobs Preview: A rebound that could not matter

- US private sector job creation is expected to rebound to 150,000 in October.

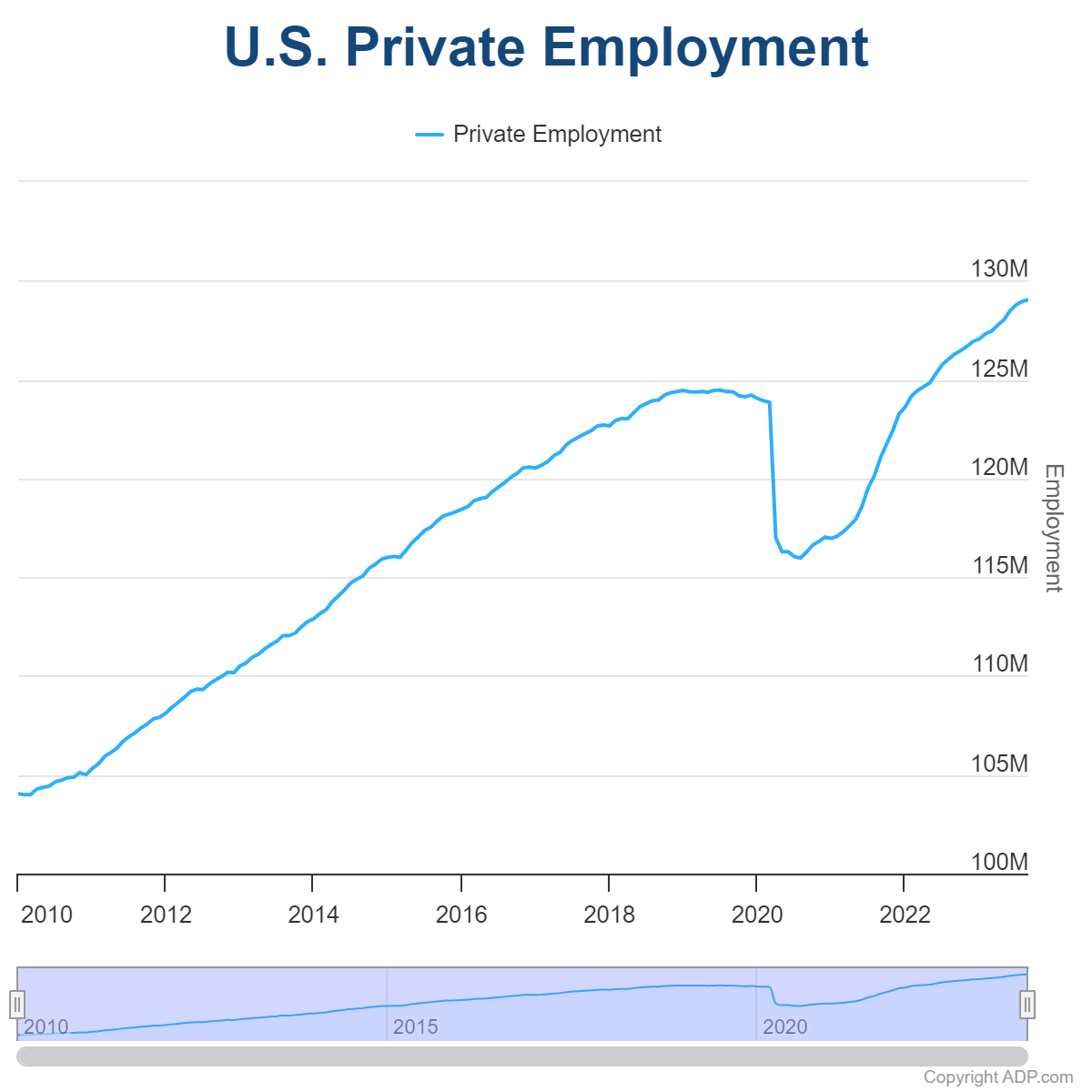

- The previous ADP report came below expectations, recording a gain of 89,000 jobs, marking the slowest growth since January 2021.

- The US Dollar remains firm, supported by US data, but unable to make new highs.

On Wednesday, at 12:15 GMT, Automatic Data Processing (ADP) will release its employment report for October. According to market consensus, US private payrolls are expected to increase by 150,000. If the actual reading aligns with this forecast, it would indicate a rebound from the gain of 89,000 recorded in September, which was the slowest growth seen since January 2021. In August, the increase in private payrolls was 180,000. The last two reports have shown a slowdown compared to previous months, with numbers below the average for 2023.

More employment data is scheduled for release during the week. The September JOLTS Job Openings report and the ISM Manufacturing Employment Index will follow the ADP report on Wednesday. On Thursday, the weekly Jobless Claims figures will be analyzed, and on Friday, the crucial official employment report will be released. Expectations for Nonfarm Payrolls are for an increase of 180,000 jobs, which, if met, would be the smallest increase since June 2023 and below the average of the past 30 months.

Overall, labor market indicators point to a softening market that remains tight, allowing the Federal Reserve (Fed) to raise interest rates further if it deems it necessary. The job market itself is not pressuring the Fed to tighten monetary policy. Data released on Tuesday showed that the Employment Cost Index (ECI) increased by 1.1% in the three months ending in September. While the number remains above pre-pandemic levels, it is trending lower. Wage inflation appears to be slowing down, but as it remains above the long-term trend, together with inflation above target, it keeps the Fed cautious and uncertain about tightening monetary policy further.

The Federal Reserve will announce its decision on Wednesday, and no change in interest rates is expected. The ADP number is unlikely to change that outcome, nor will the ISM report or the ECI. Therefore, the market impact of these figures could be limited but still create volatility ahead of the Federal Open Market Committee (FOMC) statement.

Last month, the ADP report triggered a modest market reaction that did not last. Although figures came in below expectations, the US Dollar was not affected. Despite a softer labor market, the economy remains robust and, more importantly for the market, performs stronger than its European neighbours and Japan.

Technical DXY: More consolidation on the cards

Less than a month ago, the day before the ADP September report, the US Dollar Index (DXY) peaked at 107.34, its highest level since November 2022. Then DXY underwent a correction, dropping as low as 105.35 (Oct 24 low). Overall, it is moving sideways, holding onto most of the gains from the July-October rally, hovering around 106.00.

US economic data and a deterioration in risk sentiment have contributed to keeping the correction limited. Domestic data not only came in above expectations but also showed surprising positive numbers, such as last week's 4.9% Q3 GDP growth. US yields have pulled back but remain at levels not seen in years, supporting the Greenback. The expectation of longer-lasting higher interest rates, rather than more rate hikes, has been a crucial factor.

The US Dollar Index chart indicates more consolidation ahead, as it offers no clear directional signs. The 20-day Simple Moving Average (SMA) is trending south, while technical indicators show contradictory signals. The DXY has a key support level around 105.50, which is a horizontal level and also the 23.6% Fibonacci retracement of the 99.58 - 107.34 rally. A consolidation below that level would suggest further losses. On the upside, a decisive break above 106.70 is needed to put the DXY on the road to retest the cycle highs.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Matías Salord

FXStreet

Matías started in financial markets in 2008, after graduating in Economics. He was trained in chart analysis and then became an educator. He also studied Journalism. He started writing analyses for specialized websites before joining FXStreet.