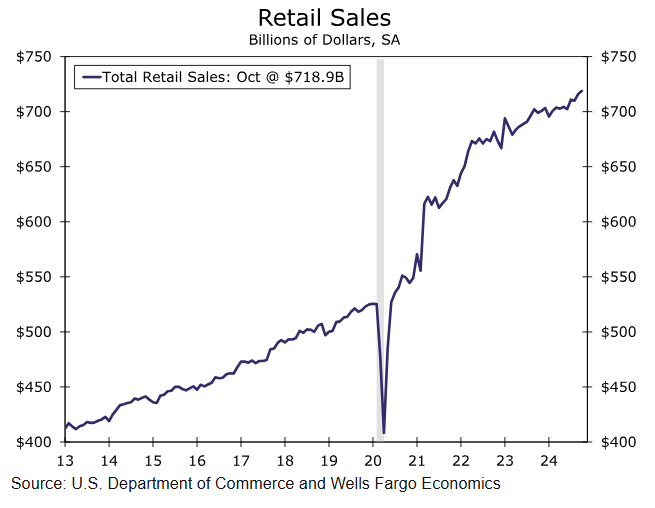

A solid October for Retail Sales and upward revisions

Summary

Giddy up Jingle-horse, retailers reported another better-than-expected month in October even as September's sales numbers were revised sharply higher. An otherwise lackluster year for retailers is gaining some last-minute momentum just as Holiday Sales get underway in November and December.

Solid October on the heels of an even better September

It was another better than expected month for retailers in October, a feat made even more impressive by the fact that revisions doubled last month's increase (chart). The initially reported September increase of 0.4% was lifted to 0.8% in the revision. The 0.7% gain in September control group sales, a proxy for personal spending in the GDP report, was revised to a 1.2% surge. That makes September the strongest month of 2024 for core spending and notches the biggest monthly pop since January 2023.

On that basis, the scant 0.1% giveback in control group sales is not terribly disconcerting. The strong finish to Q3 put PCE spending on track for a decent finish in the home stretch. Our forecast for Q4 consumer spending is 2.0%, and today's retail sales figures point to some upside risk.

Eight of the thirteen categories of stores boasted better sales in October (chart). Despite Prime Day occurring during the month, ecommerce saw only a modest gain of 0.3%. Even so, the category is still up 9.4% over the past year, the most of any category.

Going out to eat is so expensive, let's do more of it

Electronics and appliance stores saw a 2.3% gain, the biggest increase in October sales of any store type. Sales at these stores are still down slightly from a year ago. The next largest gainer was autos and auto parts sales.

Prices are still high even if inflation is not. Still, the moderation in the pace of price growth is allowing consumers to ratchet up spending in some fun categories even as they continue to scale back in others. Grocery bill prices jumped 0.4% in September, but advanced just 0.1% in October according to the CPI report released this week. The 0.1% nominal gain for grocery store spending in today's report for October suggests most shoppers are going home with about the same amount of stuff, they are just not having to shell out as much additional money as they did in September.

Food away from home inflation remains elevated relative to its pre-pandemic pace, but has cooled off over the past year. In fact the year-over-year increase in the cost of going out to eat is 3.8%—the smallest one year change since the spring of 2021. Spending at bars and restaurants jumped 0.7% in September. That takes the year-over-year gain in this category to 4.6%. People may not love how much it costs to go out to eat, but their bar and restaurant spending is growing faster than prices are.

Author

Wells Fargo Research Team

Wells Fargo