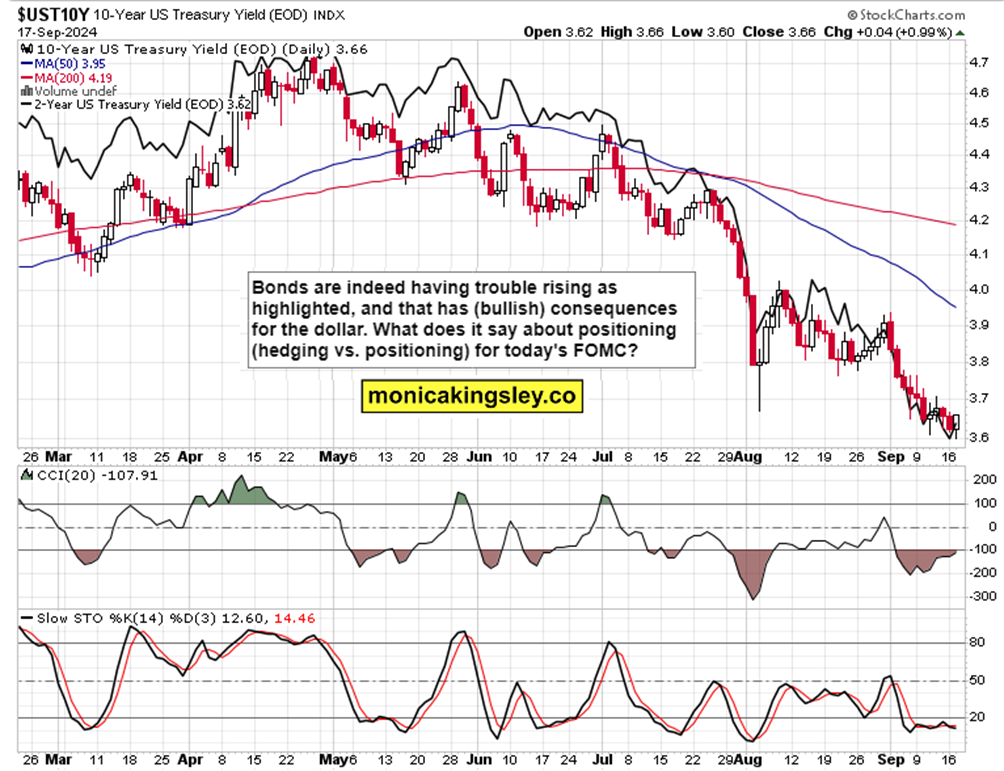

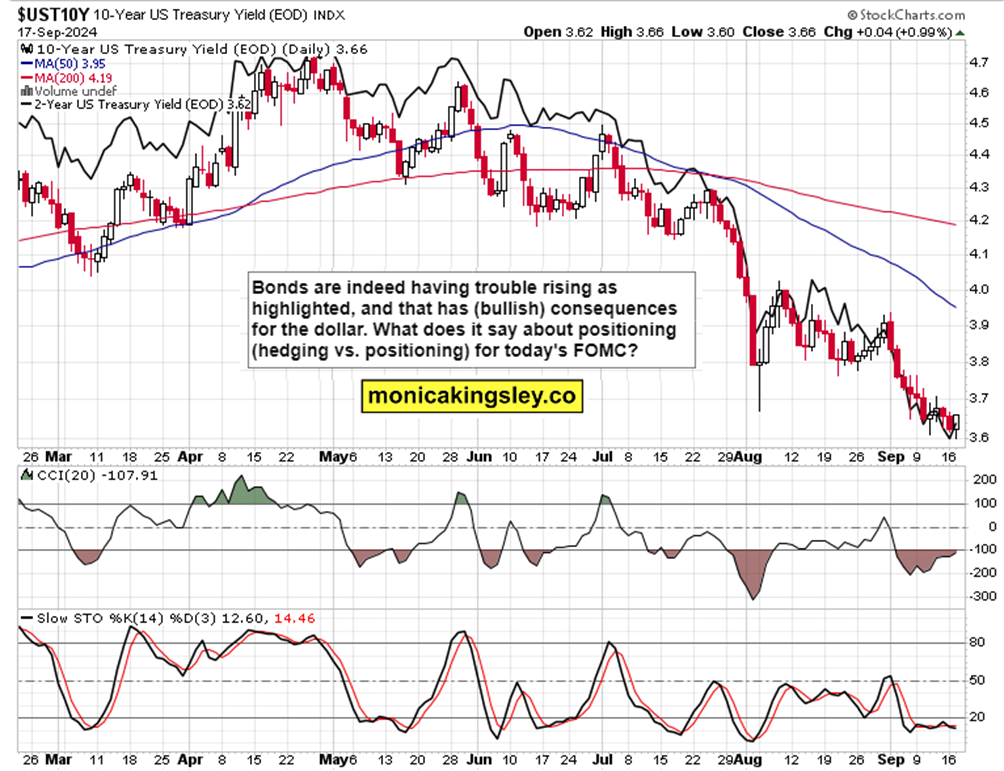

50 bps to start with

S&P 500 gave a little preview of FOMC volatility, with first the upswing to capitalize on for clients, and then a sharp intraday decline I warned clients about too. The same concerns interest rate sensitive plays watchout for buying climax (plain rejection to go up) followed by decline.

Macroeconomically, that was justified by good retail sales figure lifting up 25bp cut odds – subsequently countered by 50bp trial balloons by select public speakers. The uncertainty about 25bp vs. 50bp cut is immense, and the real question being what‘s the prevailing expectation now, and I‘m leaning towards it being 50bp in the end. Reassuring 50bp cut to start with, markets are being convinced.

Quoting Sunday‘s analysis and developing the thoughts much further for clients in the premium sections (plenty of Telegram and Twitter coverage follows):

(…) Will we get the reassuring 25bp cut that I had been a fan of, or is the new favorite of 50bp the reassuring one (no asleep at the wheel) now? Given what I see happening in various sectors and even individual names, I have an answer below for clients.

… the put to call ratio...just so, so complacent…

… positioning for a bullish outcome... is actually so strong that the ratio of stocks trading above various moving averages, is at levels associated with local tops being formed. Caution is warranted as volume is picking up.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.