4 Gold mining stocks for investors seeking Gold exposure

4 Gold Mining Stocks For Investors Seeking Gold Exposure

Gold has been on a constant rise since the COVID-19 pandemic heightened the fears of a recession. While gold experienced a brief dip along with stocks at the beginning, it has recovered nicely. This has led to many investors wanting a higher level of exposure to gold.

Owning gold mining stocks can be a great way to gain exposure to gold. While there are numerous ways to hold gold, many of them have their shortfalls. For example, buying bullion will not only require a lot of cash upfront, but storing it will be a hassle as security would be a paramount issue.

Gold mining stocks allow you to not only invest as little or as much as you want, but you also have the peace of mind of knowing that your investments are safe from physical threats (e.g. theft). With over 300 gold mining companies currently trading on the stock exchange, you have ample options for which markets and areas you want to have exposure to.

However, the returns on gold mining companies depend on a lot of things. Of course, the price of gold correlates with the stock price of mining companies over the long term. That is not all, though. Their returns also depend on how efficient their management is, how they cut costs, their reserves, risk management, and exploration activities.

As such, we will be taking a look at 4 companies that you should be looking to invest in. We will explore what separates them from the rest, and why they should be the ones to receive your money.

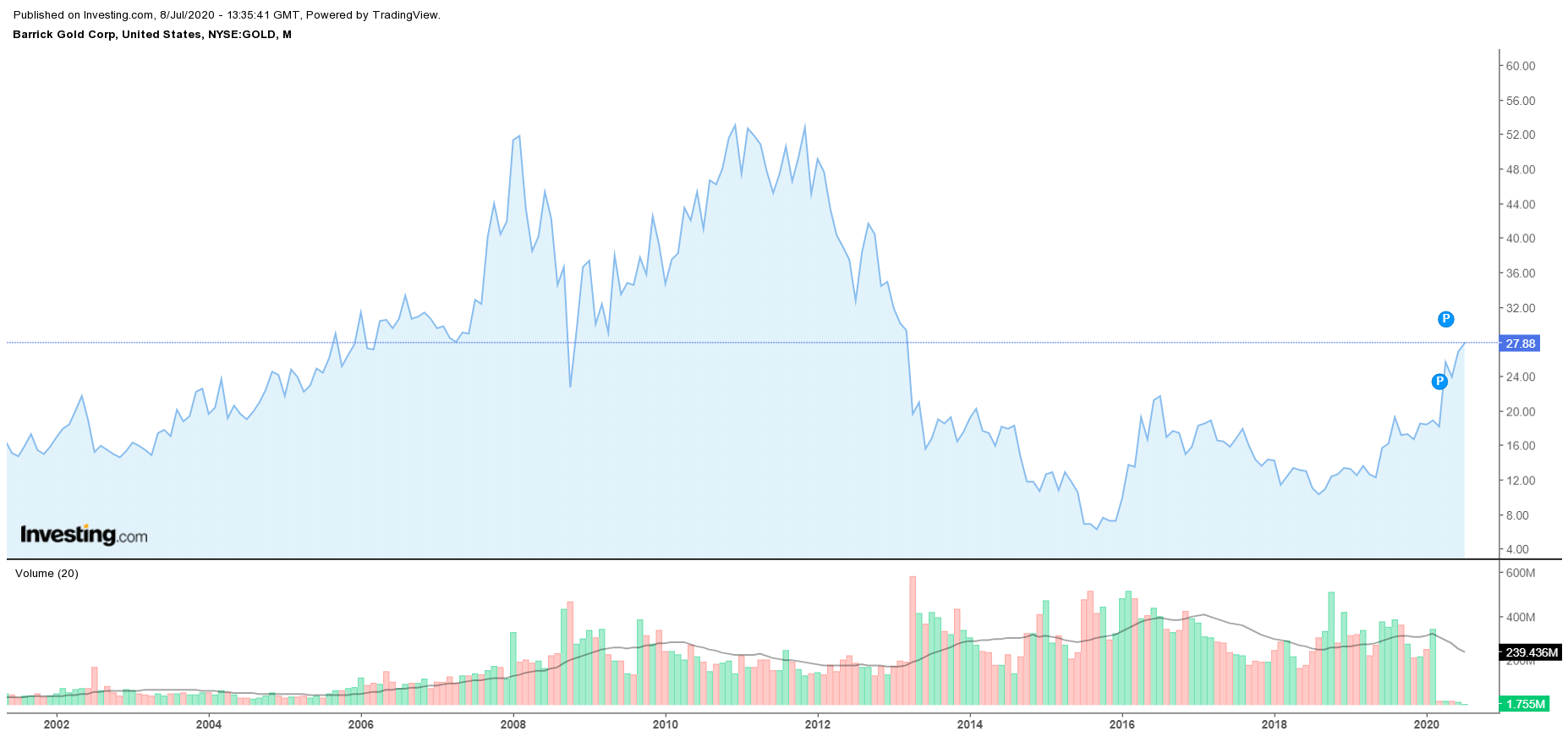

Barrick Gold (NYSE: GOLD)

Barrick is one of the oldest gold corporations on the planet, which should be obvious because their ticker symbol is GOLD. They operate all over the world, with some of their largest mines being in the US, Canada, Argentina, and Congo. With a market cap of over 47 Billion at the time of writing, this is a stock that is great for value-based investors.

It has risen over 70% in the last 12 months, yet its PE ratio is still conservative at 11. With cash reserves of over $3 Billion, Barrick is a conservatively run company that does not take too many risks. This is ideal for investors seeking stable, gradually increasing returns. The company’s debt profile is also spotless (Debt/FCF ratio is just 3.07, while the Quick Ratio is 1.8). The company also pays a stable dividend that should tide you over until you experience returns in its stock price.

In 2019, Barrick merged with Randgold. This allowed Barrick to expand its operations on the African front. Barrick will almost certainly be using its massive resources for further exploration in Africa, as the continent is still largely untapped due to its vast size.

Over the last few years, Barrick has been expanding its operations in the US. One of their biggest projects is in the Nevada Gold Mines. It is a joint project in which Nevada owns 61.5% of the mine and Newmont Corporation (another company we talk about) owns the rest.

The mine seems to be doing incredibly well. According to Barrick, the mine exceeded all of their expectations during the first year of its operation. As Barrick continues to expand its operation in Nevada and Africa, and provided that the price of gold continues to rise, we should see strong returns for Barrick in the next few years. In fact, some analysts are claiming that its price could go over $50, as it was trading at over $50 last time the gold prices were as high as they are today.

Barrick was one priced in the mid $50s. If the current bull run of gold continues, chances are that it could return to that value.

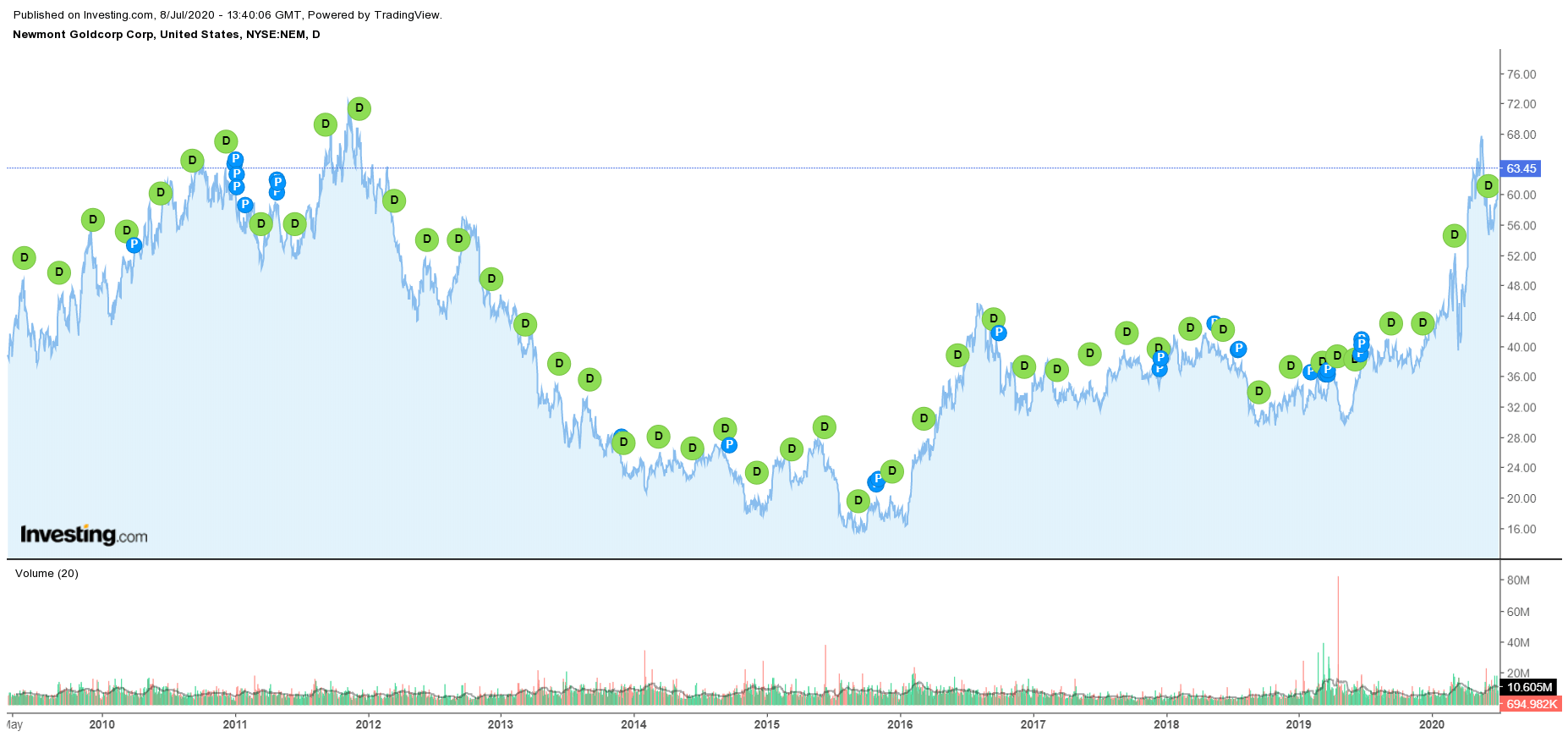

Newmont Corporation (NYSE: NEM)

Newmont is a company that is quite similar to Barrick and supplies another great way to gain exposure to gold. It is based in North America, has a market cap of just over $50 Billion, is conservatively run, and seems to be undervalued right now. For conservative investors who value a company that pays a constantly growing dividend and has been performing really well as of late, this is an ideal company.

Newmont has a slightly higher PE ratio of 13.94. However, that is probably because of its larger dividend, which has a forward yield of 1.6%. Newmont, just like Barrick, does not have a lot of debt. Their Debt/FCF ratio is 3.52, and the total debt to equity is 30.17% at the time of writing.

Even when compared to other gold companies, Newmont is run very efficiently. The company has a net margin of 30.66%. With cash reserves of nearly $4 Billion, it is no surprise that Newmont has risen over 60% in the last year.

Due to massive entry barriers and gold exploration slowing down in recent years, we are seeing consolidation in the gold industry. Just like Barrick, Newmont acquired Goldcorp last year in a deal worth $10 Billion. That, along with their joint venture, in Nevada, should help Newmont increase their returns in the next few years.

Newmont is slightly riskier than Barrick. However, it does offer a dividend that is a lot higher and has a history of consistent growth. The company also repurchased $300 Million worth of its shares recently, further proving that the gold mining industry will probably be slowing down. If that happens, the competition will be scarce, and bigger companies should be able to easily capitalize off of the rise in gold prices.

For investors who are willing to risk a little bit in order to increase their returns, Newmont is the perfect company.

Newmont has paid a dividend even through the worst of times. The size of the dividend seems to correlate with their profits, so an increase in gold price should also increase the dividend.

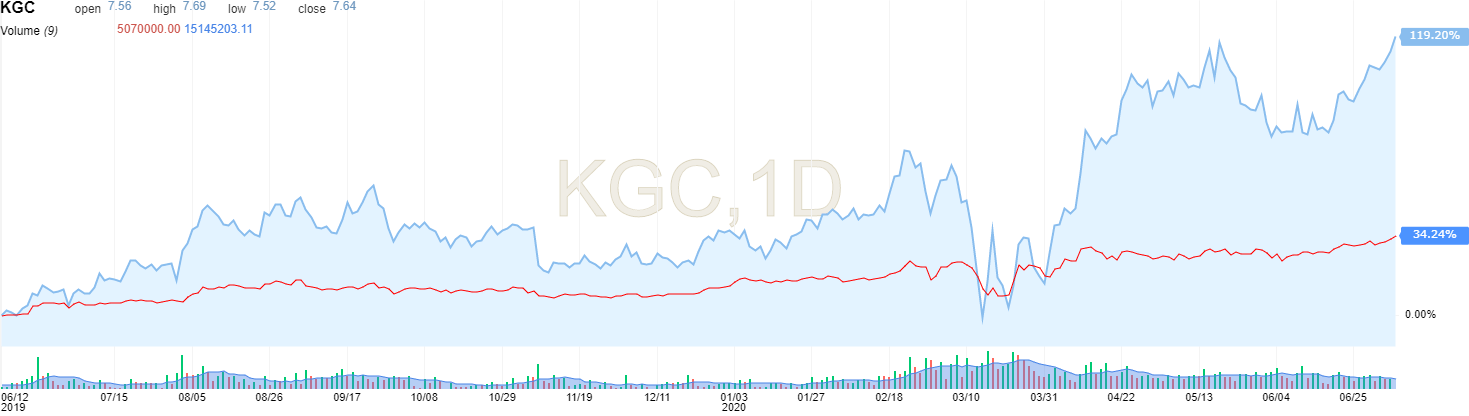

Kinross Gold Corporation (NYSE: KGC)

Compared to the previous two companies on this list, Kinross is a riskier bet. However, we stated that the gold mining industry has been consolidating. Due to this, there are only a few major players left, leaving you with few options if you are risk-averse (and a lot of you are pursuing risk). Kinross still seems like a decent investment, although it banks on gold prices rising for the foreseeable future.

The company has a market cap of just under $10 Billion along with a PE Ratio of 11.99. However, Kinross has taken a lot of debt relative to other companies. The Debt/FCF ratio is a staggering 21.70. This may be understandable for a Silicon Valley startup, but it is definitely very high for a gold mining company.

However, it does have a high quick ratio of 2.0, and cash at hand of $1.16 Billion. Considering the fact that it is less than one-fifth the size of Newmont, this means that the company is more than capable of meeting all of its short-term obligations.

Due to its smaller size, Kinross is perfect for those who have a slightly larger appetite for risk but still want exposure to gold. This is evident in their performance, as the stock has risen 94% over the last 52-weeks.

However, potential investors must be wary of their debt profile and how their performance is tied to the gold price. A rising gold price should allow them to be profitable and achieve a high amount of growth. On the contrary, a normalization of the economy and a fall in gold price would almost certainly be disastrous for Kinross in the long run due to their debt profile.

Kinross reacts quite aggressively to gold prices. Just look at how it moves against gold futures. If the prices continue to rise, you should expect the stock price to rise to nee heights.

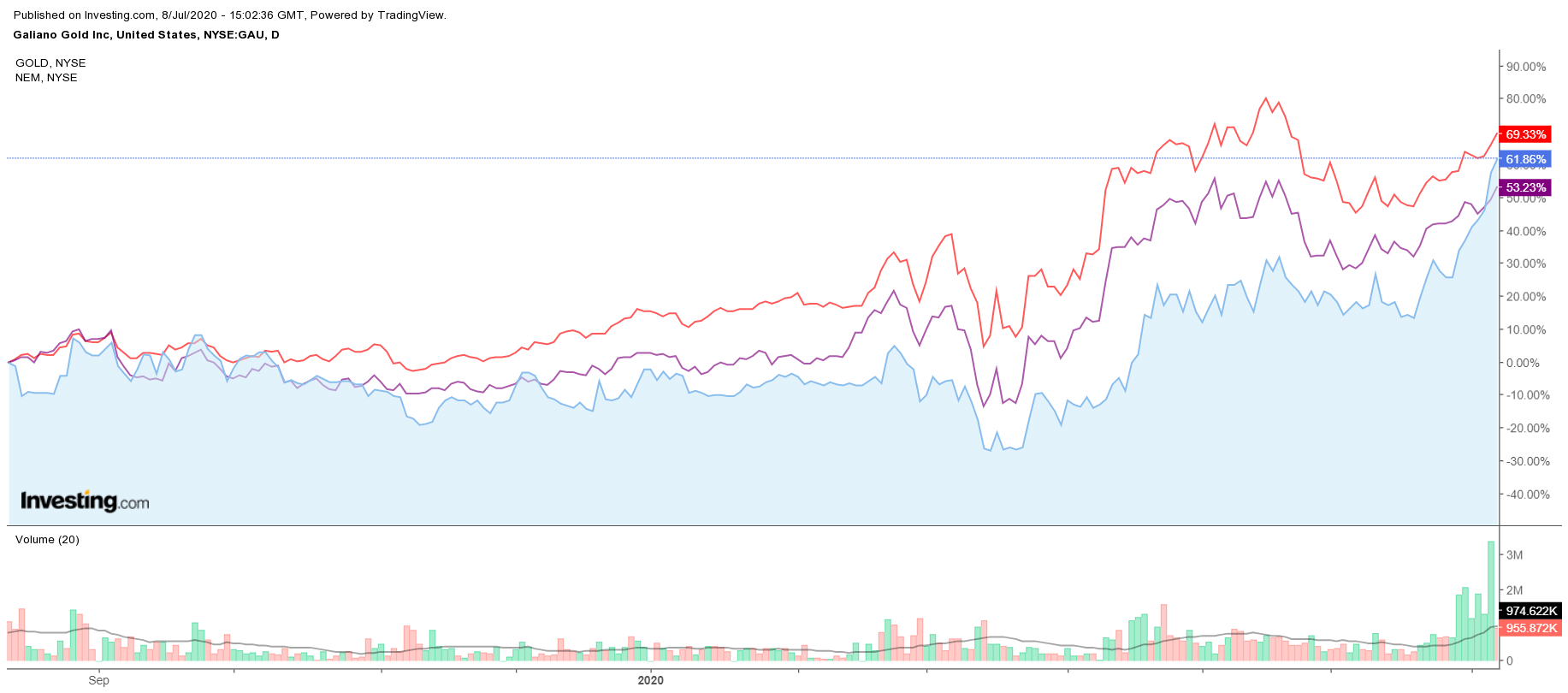

Galiano Gold (NYSE: GAU)

The last company that we are looking at is a stock that has a huge upside potential, but not a lot of downside risk. Galiano, previously known as Asanko Gold, is a Canadian based company currently operating on the Asanko gold mine in Ghana. If I am guessing, I believe that they changed their name because they plan to expand their operations.

While the company is operating at a loss in 2019, it has had a strong start to 2020. The first quarter shows a basic EPS of $0.1, which is double the estimates. Considering the fact that the company is priced at $1.53/share at the time of writing, it is very easy to see why this is such an exciting stock.

To add to that, the company holds over $50 Million in cash ($0.23/share) and has almost no debt to speak of. Since February, we have seen the company rise by over 35%, and its performance for the last 12-months has been a staggering 137.5%. However, there is no reason to believe that the company has reached its full potential.

The Asanko gold mine does not seem to be letting up anytime soon. Still, the company has drawn a $30 Million revolving credit facility so as to have some extra cash on hand in case of an adverse event occurring due to COVID-19. Considering their recent results (the company generated $27 Million of free cash flow in the first quarter), we highly doubt that they will need to use it.

Despite being a much smaller company, Galiano seems to move in tandem with major competitors in the field. Here, you can see that Galiano rises and falls in a similar pattern to both Barrick and Newmont.

Conclusion

From the 4 stocks mentioned above, we have to say that Galiano Gold is by far the most exciting. Priced very reasonably, if gold prices continue to rise, we expect its returns to be much higher than the other 3 stocks on this list.

However, conservative investors looking for safe companies to gain exposure to gold should probably stay away from Galiano. Newmont and Barrick are safe companies with a stable return, making them perfect for those whose first and foremost investment goal is to not lose money. Kinross, on the other hand, lies somewhere in between the two.

Author

Baruch Silvermann

The Smart Investor

Baruch Silvermann is a personal finance expert, investor for more than 15 years, digital marketer and founder of The Smart Investor.