2025 outlook: What is next for developed economies and currencies?

As the door closes in 2024, and while the year feels like it has passed in the blink of an eye, a lot has happened. If I had to summarise it all in four words, it would be: ‘a year of surprises’.

Storylines dominating markets in 2024 include global central bank policy easing, inflation, jobs, growth, the US Presidential election, the rapid adoption of Artificial Intelligence (AI), and heightened geopolitical tensions in Europe and the Middle East. The effects of said variables will likely continue to echo through the global economy to varying degrees over the next few years. Anticipation of a strong rebound in China also failed to come to fruition this year, weighed by a property market in disarray (homebuyers losing confidence in an overbuilt economy), global trade tensions, deflationary pressures, and cautious consumers.

Double-digit returns were seen across most major stock indices worldwide, pencilling in all-time highs along the way. The patient investor was rewarded this year – not something many analysts/investors, including myself, foresaw at the beginning of 2024. AI undoubtedly remains in a boom and was a large driver of outperformance, with forecasters expecting this to continue in 2025. According to the US Dollar Index, the US dollar (USD) also outperformed this year, posting three consecutive months of upside into the year-end, and US Treasury yields largely rallied across the curve.

This ‘look-ahead’ post will explore US, European, and UK economies and attempt to offer ways of navigating an exciting – but uncertain – year ahead.

What is on the table for 2025?

- The ‘global cut’

Developed central banks pivoted to an easing bias in 2024, with expectations of further rate cuts on the drawing board in 2025.

- Economic outlook

How have key economies fared in 2024, and where are they likely headed in 2025?

- The ‘Trump era’

How could the Trump Era influence market action next year? Views of less regulation, tax cuts, tariffs, and mass deportations place 2025 in an uncertain light.

- Currency market in 2025?

How are currencies likely to perform in 2025?

What is the fundamental and technical picture telling us?

The ‘global cut’

As the heading implies, 2024 was one of a ‘global cut’.

With the exception of the Reserve Bank of Australia, which held the Cash Rate at 4.35%, and the Bank of Japan increasing its Policy Rate to 0.25% and finally exiting negative rates, most developed central banks embarked on policy easing this year. I expect further easing to continue as central banks unwind from restrictive territory towards more ‘neutral’ ground.

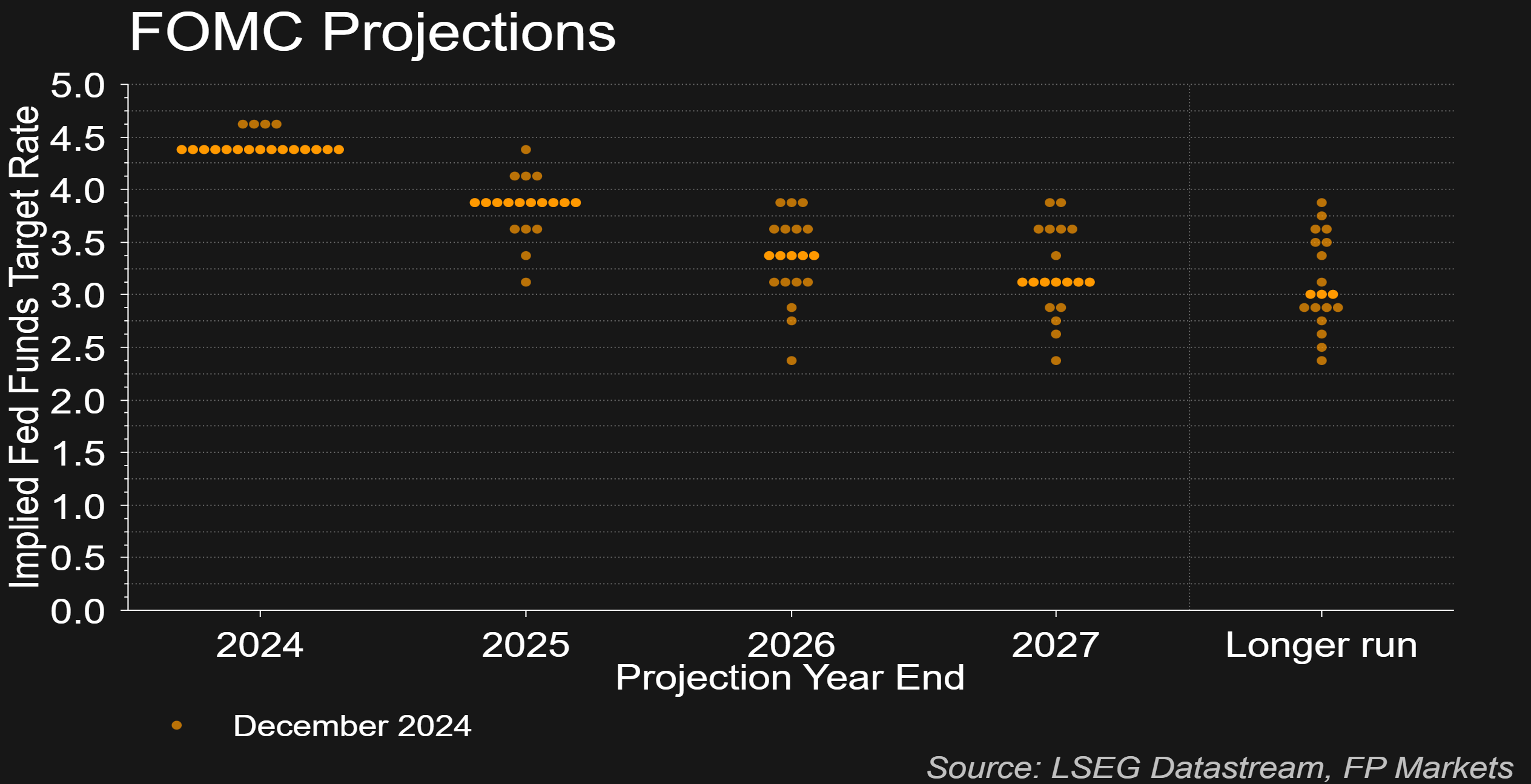

In a ‘hawkish cut’, the US Federal Reserve (Fed) reduced the target rate by 25 basis points (bps) to 4.25%-4.50% at the last meeting of the year. This was the third consecutive rate reduction, marking 100 bps of cuts for the year.

The Fed’s dot-plot projections (derived from the Summary of Economic Projections) were unquestionably hawkish, suggesting a slower pace of cuts for 2025 and 2026. FOMC participants actually revised the funds target rate lower to 50 bps in 2025 from 100 bps!

Economic projections also revealed that the Fed expects inflation to accelerate next year – PCE inflation (Personal Consumption Expenditures) is now anticipated to end 2025 at 2.5% compared to 2.1% in previous projections and 2.1% in 2026 (versus previous forecasts of 2.0%). Overall, the Fed is not expecting to see PCE data at the 2.0% inflation target until 2027.

Couple the above with uncertainty ahead of President-elect Trump's proposed policies in early 2025, along with the lone dissenter – Cleveland Fed President Beth Hammack – who called for the Fed to hold the target rate at current levels, a hold at the next meeting in January is likely a done deal (markets are currently assigning a 92% probability of a no-change decision). Markets are not expecting the Fed to push ahead with a 25 bp rate cut until June’s meeting.

The European Central Bank (ECB) also cut the Deposit rate by 100 bps to 3.0% over the course of 2024, its lowest rate since early 2023.

I added my thoughts on the December cut in a recent post:

‘Barring anything unforeseen, we will see further cuts in early 2025, albeit likely gradual, incremental 25 bp reductions. Markets are currently pricing in another 125 bps of cuts by the end of 2025, which would take the deposit rate to 1.75%. Markets are then forecasting that the central bank will remain on hold. However, some desks feel the focus has shifted to whether the central bank is doing enough to support the eurozone economy, which is lagging the US and the UK, and they believe the ECB needs to pick up the pace of rate cuts. Market participants, therefore, are expected to keep a close eye on potential indicators of economic challenges, particularly as concerns have heightened due to policy inaction in Germany and political stalemate in France. Such indicators could imply the likelihood of more substantial interest rate reductions in the coming year’.

In terms of where the ECB Staff’s latest projections stand, I also added the following:

‘On the GDP growth front, the eurozone economy is now expected to grow at a slower pace, by 0.7% in 2024 (down from 0.8% in previous projections), 1.1% in 2025 (from 1.3%) and 1.4% in 2026 (from 1.5%). Inflation is expected to average 2.4% this year (down from the previous projection of 2.5%). It is also forecast to further slow to 2.1% in 2025 (from 2.2%) and then cool to 1.9% in 2026 (unchanged from previous projections). For core inflation, 2024 and 2025 projections were unchanged at 2.9% and 2.3%, respectively, though 2026 was revised to 1.9% (down from 2.0% in the previous projection)’.

Analysts at Vanguard said: ‘We expect the European Central Bank to bring its policy rate below neutral in 2025, ending the year at 1.75%. Risks to this outlook skew to the downside. An intensification of trade tensions and a significant slowdown in global growth would each likely result in a more dovish monetary policy stance’.

The Bank of England (BoE) reduced its Bank Rate by 50 bps to 4.75% over two rate cuts during the year. The last meeting in December delivered a divided MPC (Monetary Policy Committee), with three (Deputy Governor Dave Ramsden and external members Swati Dhingra and Alan Taylor) out of nine members voting for a cut.

While the latest MPC vote is considered a dovish shift and an unexpected move (economists forecasted an 8-1 vote in favour of a hold), the rate statement’s language was cautious. BoE Governor Andrew Bailey also noted that the central bank could not commit to ‘when or by how much’ they will ease policy next year, given ‘heightened uncertainty in the economy’. Bailey also commented that a ‘gradual approach’ to reducing policy remains right.

Market pricing remained unchanged following the rate decision, with investors expecting 50 bps of cuts next year, with the first 25 bp cut not priced in until May.

The BoE’s latest Monetary Policy Report (released in November) forecasts GDP (Gross Domestic Product) will rise to 1.7% in Q4 25 (compared to the 0.9% forecast in August), with Q4 26 GDP expected to grow by 1.1% (lower than the 1.5% forecast in August).

On inflation, BoE economists forecast an increase to 2.7% in Q4 25 (compared to the 2.2% forecast in August) before easing to 2.2% in 2026 (versus August’s forecast of 2.2%).

In terms of the Bank Rate forecasts, Q4 25 projections show the rate will be 3.7% in both 2025 (revised lower from 4.1% in the August forecasts) and 2026 (unchanged from previous forecasts).

Economic outlook

Inflation

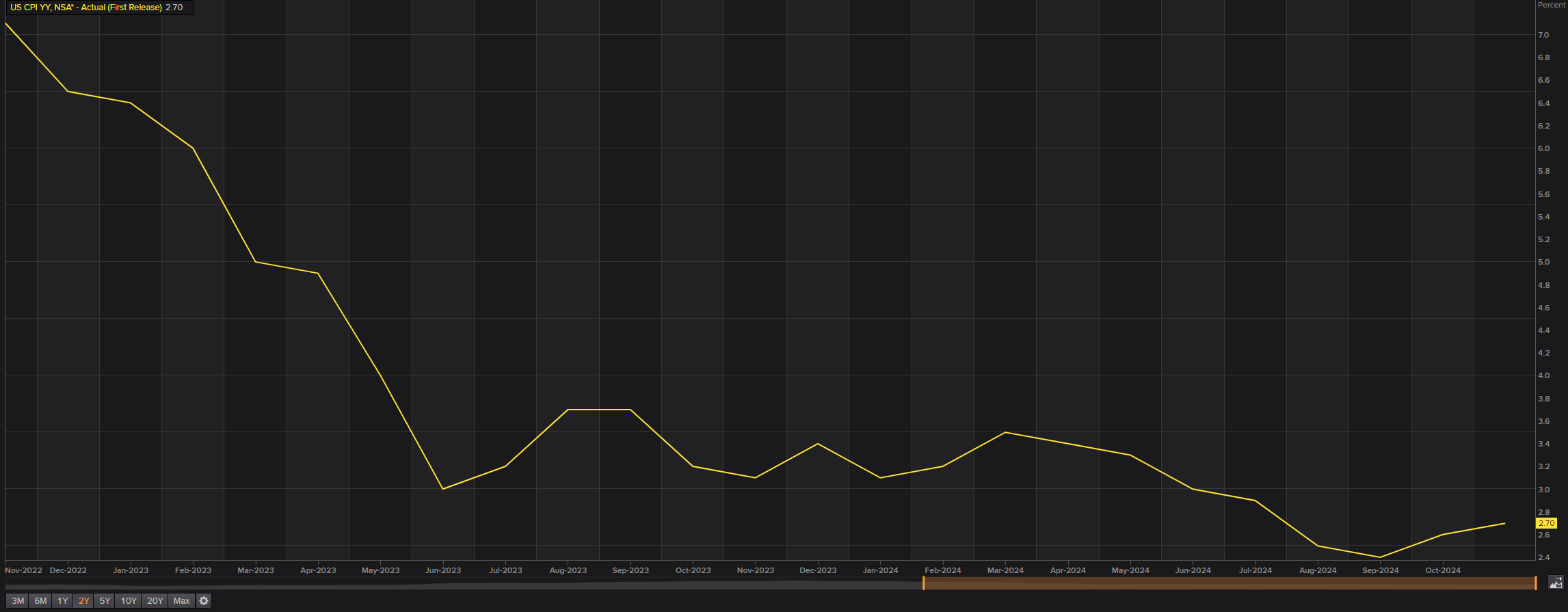

Inflation has been at the forefront for policymakers and investors this year, with developed economies reaching their central bank inflation targets or on the target's doorstep, which is usually 2.0%. Progress, however, will likely be slow in 2025 on a possible reemergence in price pressures upon us – specifics, of course, will differ from country to country.

Upside risks to inflation are evident in the US, influenced in part by President Trump’s proposed policies, particularly tariffs and immigration. As a result, consumer spending, which has driven US economic growth since the pandemic, may face pressures as trade policies affect prices for imported goods, including clothing, automobiles, and steel.

While it is obvious that tariffs never ‘reduce’ the prices of goods, their effect on pricing can vary based on several elements. For instance, the availability of homegrown alternatives for imported goods plays a significant role. Consequently, how much tariffs influence prices will hinge on which products are subjected to these taxes and how high these will be set. In addition, the impact of deportations would, of course, affect labour supply and, by extension, prompt inflation as companies increase wages to attract staff, thus elevating the cost of producing goods and services, which could then be passed on to consumers.

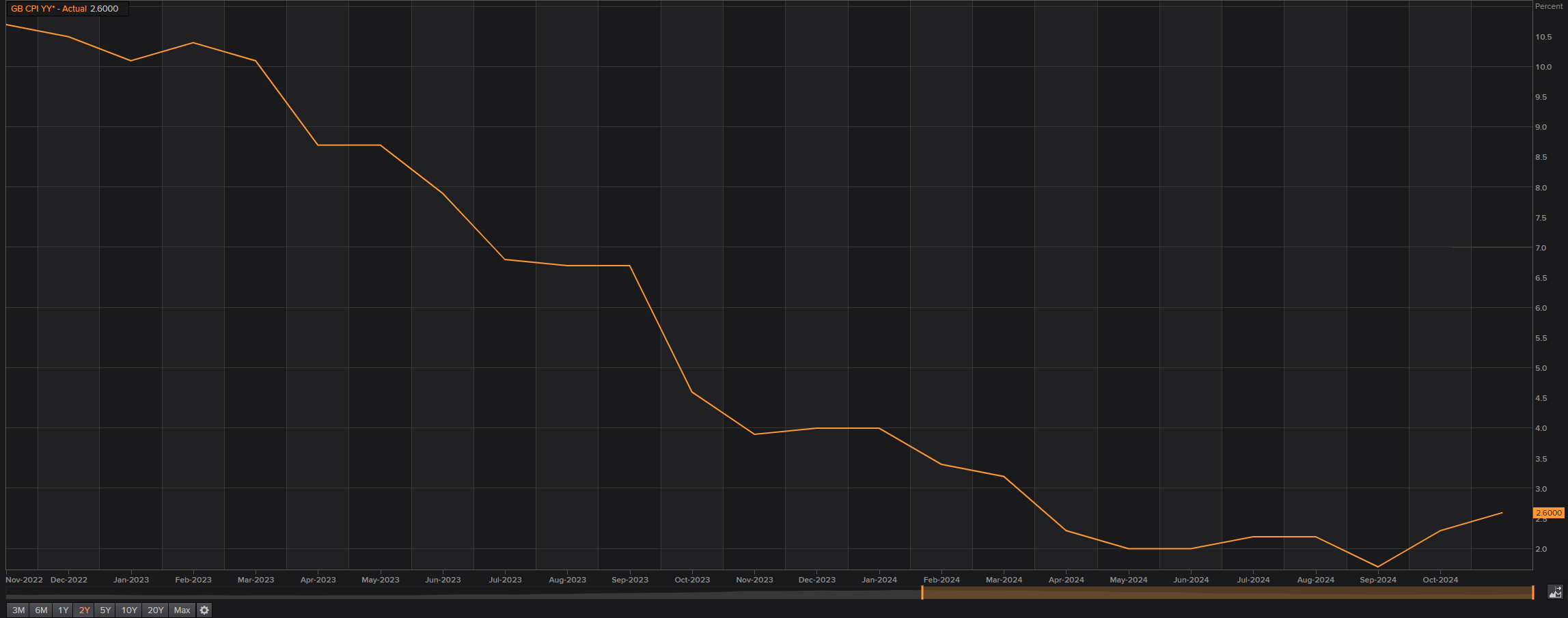

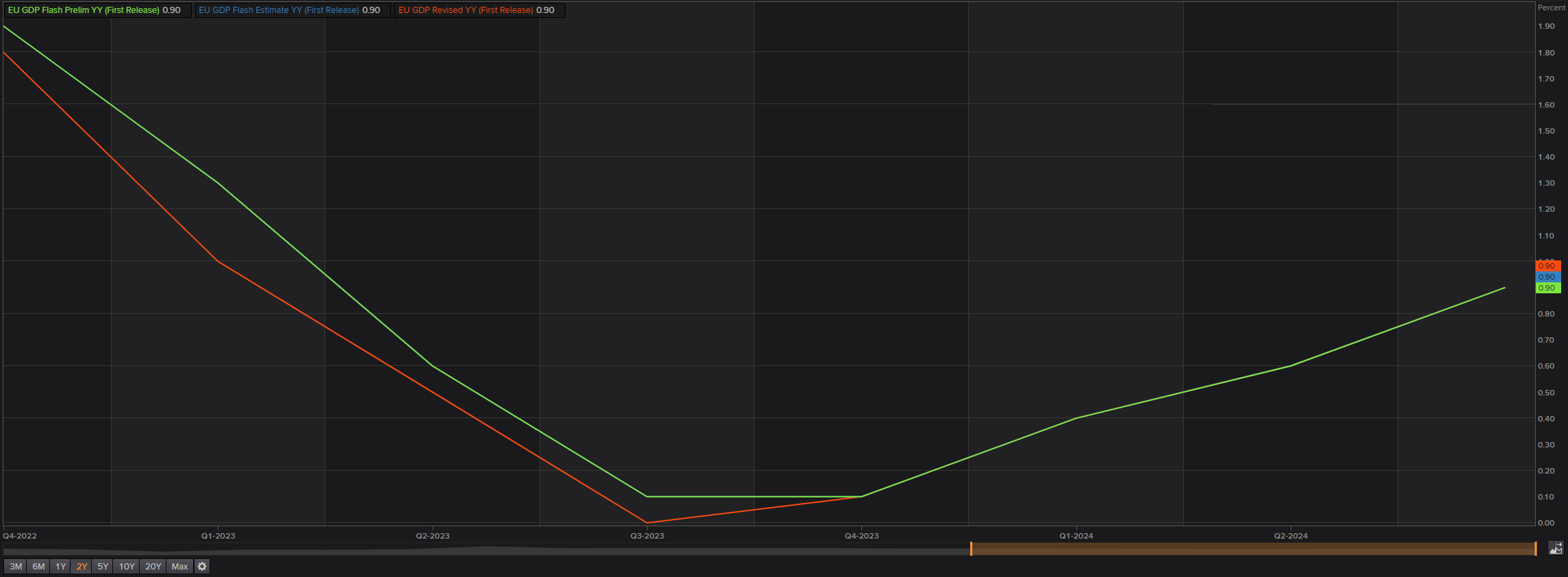

In the eurozone, inflation has been largely softening since topping around 10.6% in 2022, hovering around the ECB’s inflation target of 2.0% since early this year.

Economists at Vanguard noted that ‘amid weak growth, we expect both headline and core inflation to end 2025 below 2%’.

UK disinflation – prices rising at a slower rate – has been well and truly underway, following a peak of 11.1% in late 2022. However, price pressures rose for a second consecutive month in November to 2.6%. This comes amid a stagnating economy and follows the Chancellor of the Exchequer Rachel Reeves’ Budget – which involves plans for a significant overhaul in public spending.

In its Economic and Fiscal Outlook (released on October 2024), the Office for Budget Responsibility (OBR) forecasts inflation to increase next year, partly due to the ‘direct and indirect impact of Budget measures’. The OBR added: ‘Inflation then slowly returns to the 2 per cent target by the forecast horizon as the effect of these measures fades and the positive output gap closes’.

Other desks believe UK inflation will also increase in 2025; analysts at Deutsche Bank expect higher inflation on the back of elevated energy prices, with Pantheon Macroeconomics expecting inflation to stand at 3.0% in April next year.

GDP growth

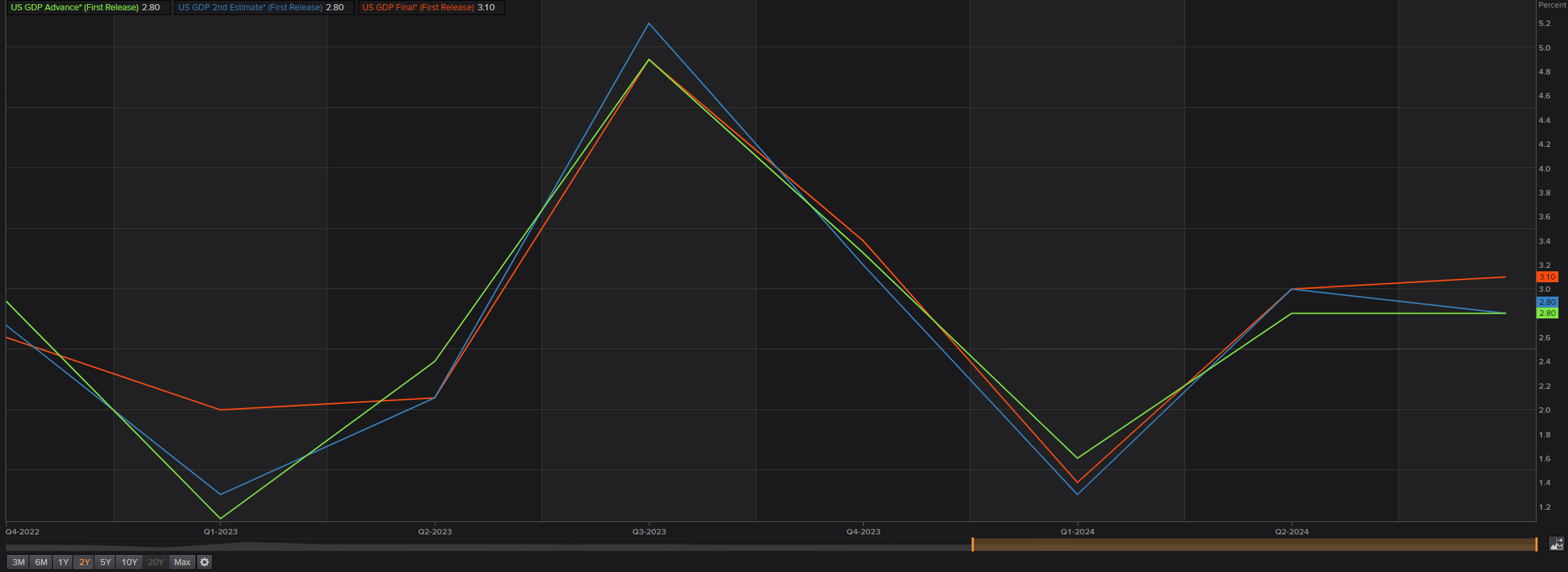

On the growth front, it is no secret that US GDP is leading the pack among developed economies, defying expectations for a marked slowdown. This is despite surging inflation and the most aggressive central bank hiking cycle in a generation.

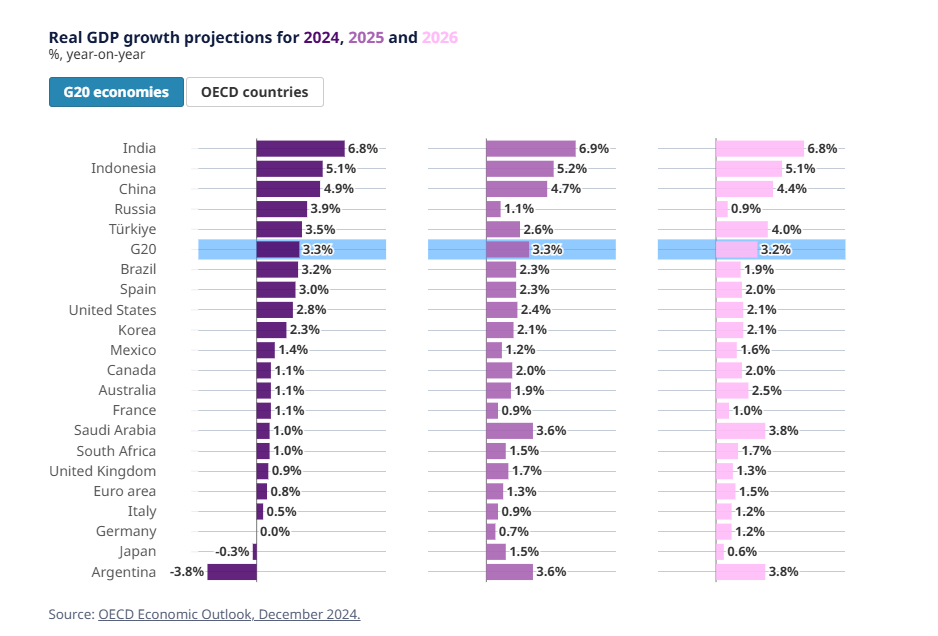

According to the Organisation for Economic Co-operation and Development (OECD), US GDP is expected to continue running at an annualised pace of 2.8% by the end of this year before cooling off to 2.4% in 2025 and 2.1% in 2026, bolstered by consumer spending and productivity growth. Recession fears have ceased for the time being, and the soft-landing narrative is certainly something many are looking at closely.

In the eurozone, OECD forecasts that this year is expected to conclude at an annualised pace of 0.8% growth and is projected to grow by 1.3% in 2025 and 1.5% in 2026. Despite this, 2025 could be another challenging year for eurozone economic activity, with some desks pointing to continuing struggles. This will be exacerbated by the expectation of US tariffs being inbound.

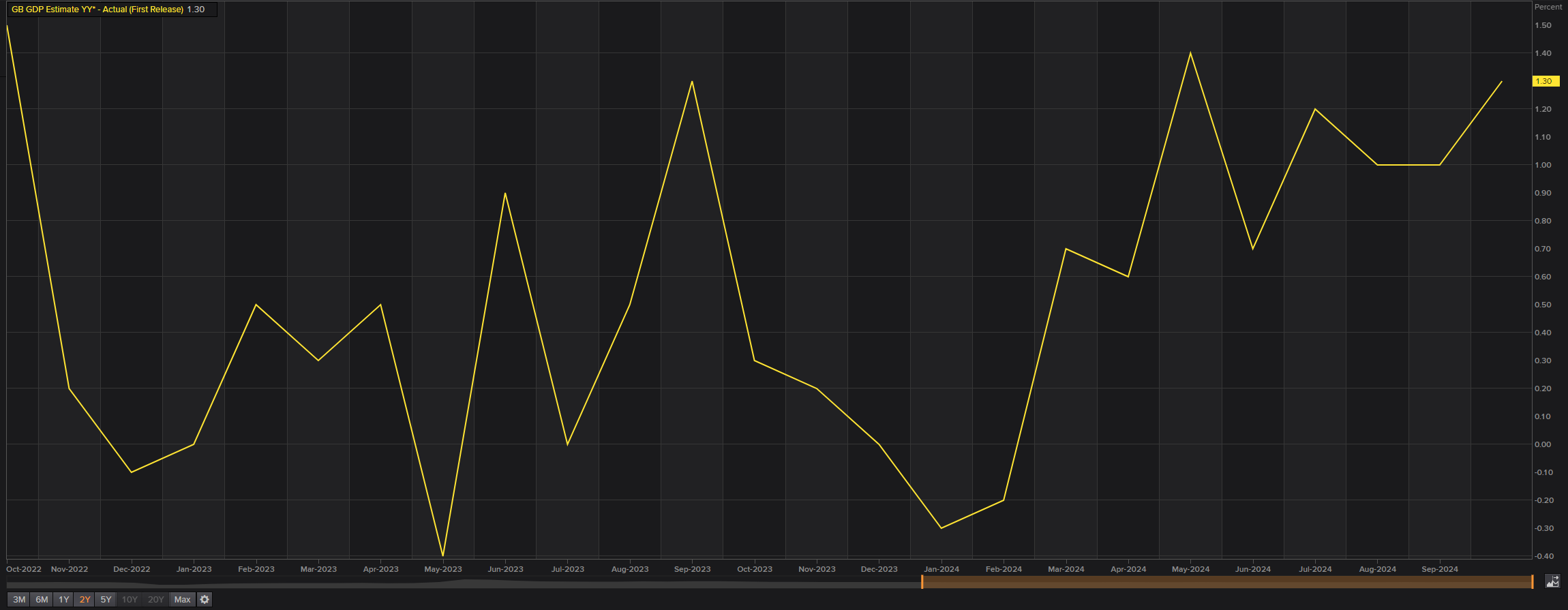

As per the OECD forecasts, GDP in the UK will grow by 0.9% by the end of 2024 and increase by 1.7% in 2025 and 1.3% in 2026. Following a successive monthly contraction in GDP by 0.1% for October, the economy had grown for only one of the five months (to October), which might mean the economy shrank for the fourth quarter.

Jobs

The latest Jobs report for the US showed that the economy rebounded in November and added 227,000 new payrolls, following October’s reading of 12,000 (upwardly revised to 36,000 in November), which was influenced by weather effects and strikes. On average, the US economy added approximately 180,000 jobs per month in 2024. Unemployment rose higher than expected in November to 4.2%, up from 4.1% in October’s print. However, the longer-term unemployment rate remains low according to historical standards. Regarding wage growth, MM (month on month) and YY (year on year) figures matched October’s data at 0.4% and 4.0%, respectively, and were slightly higher than expected on both fronts. Overall, the US labour market is clearly showing signs of cooling.

Analysts at Silvercrest Asset Management Group noted:

‘We expect job gains to continue because of the still-elevated number of jobs offered. The Job Openings and Labor Turnover Survey measures this figure. In the latest report, as of October, there were 7.74 million job openings in the United States. While this number has dropped significantly from the pandemic-disrupted reading of 12 million, it is above the 6–7 million level typical in the late 2010s’.

In the eurozone, the October jobs report indicated that the unemployment rate stood at a remarkable 6.3%, reflecting historic lows. This suggests that the expected economic slowdown and indications of decreased hiring have not yet influenced the stability of the job market. I also feel that given where wages in the eurozone currently stand – we recently saw an all-time high of 5.5% this year – this could also help underpin inflationary pressures.

Economists at Vanguard noted: ‘With a pronounced slowdown in Germany and broader growth pressures, we foresee the unemployment rate rising to the high-6% range through 2025’. This sentiment is shared by analysts at Goldman Sachs, commenting, ‘Given our subdued growth outlook, we expect the unemployment rate to rise next year, reaching 6.7% by early 2026. We see wage growth slowing to 3.2% by Q4 25, as pay catch-up completes and the labour market softens’.

Over in the UK, the biggest takeaway from the latest jobs report out of the UK was that wage growth was hotter than expected in the three months to October 2024. Both regular pay and pay, including bonuses, were equally up 5.2% from 4.9% and 4.4%, respectively. This will help underpin the case for the BoE to keep rates higher for longer next year.

We still have the issue of credibility with the ONS data from the UK, particularly with the unemployment rate, which remained unchanged at 4.3%. Although it is clear from the data that the UK job market continues to cool, it remains resilient despite the economic challenges it has been encountering.

Given the latest data, I feel all eyes are on the wages, and the BoE will be looking for softness in these numbers before cutting again. As noted, markets are not expecting the central bank to cut again before Q2 25.

The ‘Trump era’

In a landslide election win for Donald Trump on 5 November this year, investors will buckle up and zero in on proposed policies in early 2025. After the election result, major US equity indices rallied, with the S&P 500 pencilling in its largest one-day gain in around two years. The USD and US Treasury yields were also higher on the day.

What I expect from Trump early next year are immediate tariff increases on imports from China and policy enactment to lower immigration. The 2017 tax cuts are anticipated to be fully extended instead of expiring and with modest additional tax cuts also expected.

Trump may not have entered the White House yet, but he ensures his voice is heard. In late November, a couple of days before the Thanksgiving holiday, Trump voiced the possibility of 25% tariffs on Mexico and Canada and an additional 10% tariff on imports of goods coming in from China, which are three of the major trading partners of the US. At the beginning of this month, Trump then upped the ante, threatening 100% tariffs on BRICS countries should they attempt to establish a rival currency. Via his social media platform, Truth Social, he added the following:

‘The idea that the BRICS Countries are trying to move away from the Dollar while we stand by and watch is OVER. We require a commitment from these Countries that they will neither create a new BRICS Currency nor back any other Currency to replace the mighty U.S. Dollar, or they will face 100% Tariffs and should expect to say goodbye to selling into the wonderful U.S. Economy. They can go find another “sucker!” There is no chance that the BRICS will replace the U.S. Dollar in International Trade, and any Country that tries should wave goodbye to America’.

I recently posted some thoughts on this:

‘I don’t believe I need to emphasise that if Trump were to follow through with these threats and implement 100% tariffs – something I consider highly unlikely – it would raise the cost of goods from those countries and potentially ramp up inflation in the US. However, it's important to note that Trump had previously used tariff threats as a negotiation tactic, and a compromise is likely to be achieved.

Unquestionably, these latest tariff threats are huge numbers, and this underpinned a dollar bid and weighed on BRICS currencies’.

The timing of Trump’s policies will likely play a significant role as we move into January. If he prioritises tariffs and immigration measures early on in his administration, the resulting increase in costs for sellers could lead to higher prices for consumers. This, in turn, might contribute to inflationary pressures and negatively affect consumer spending. Additionally, new tariffs and stricter immigration laws could potentially hinder economic growth in the US. The overall effects of these anticipated policies will largely hinge on how and when they are implemented.

Currency market in 2025?

The US dollar has room to run, in my opinion, and I will be closely watching the mighty greenback in Q1 25. Trump’s election win and his administration’s proposed pro-growth policies are expected to elevate inflation. This, along with the investors (and the Fed) expecting a slower pace of rate cuts next year, is bullish for the USD.

The US Dollar Index – a geometric average weighted value of the USD versus six major currencies – offers a clear picture of the USD. Since 2023, buyers and sellers have been squaring off between support coming in from 100.51 and resistance at 106.11 on the monthly timeframe. What is important is the recent breach of said resistance is on track to register its highest monthly close since late 2022, prompting the possibility of follow-through upside towards resistance at 109.33.

Looking across the page to the daily timeframe, the USD recently punctured the upper boundary of a pennant pattern (drawn from the year-to-date high of 108.07 and a low of 106.13), following a rebound from trendline resistance-turned-support, extended from the high of 107.35. Given this and the monthly timeframe showing room to reach 109.33, the USD is technically bullish for now, at least until the aforementioned monthly resistance.

Chart created by TradingView

Europe’s single currency will likely take a hit in 2025, following year-to-date losses of nearly 5% versus the USD. The ECB is expected to cut rates at a faster pace than most other central banks next year, particularly the Fed.

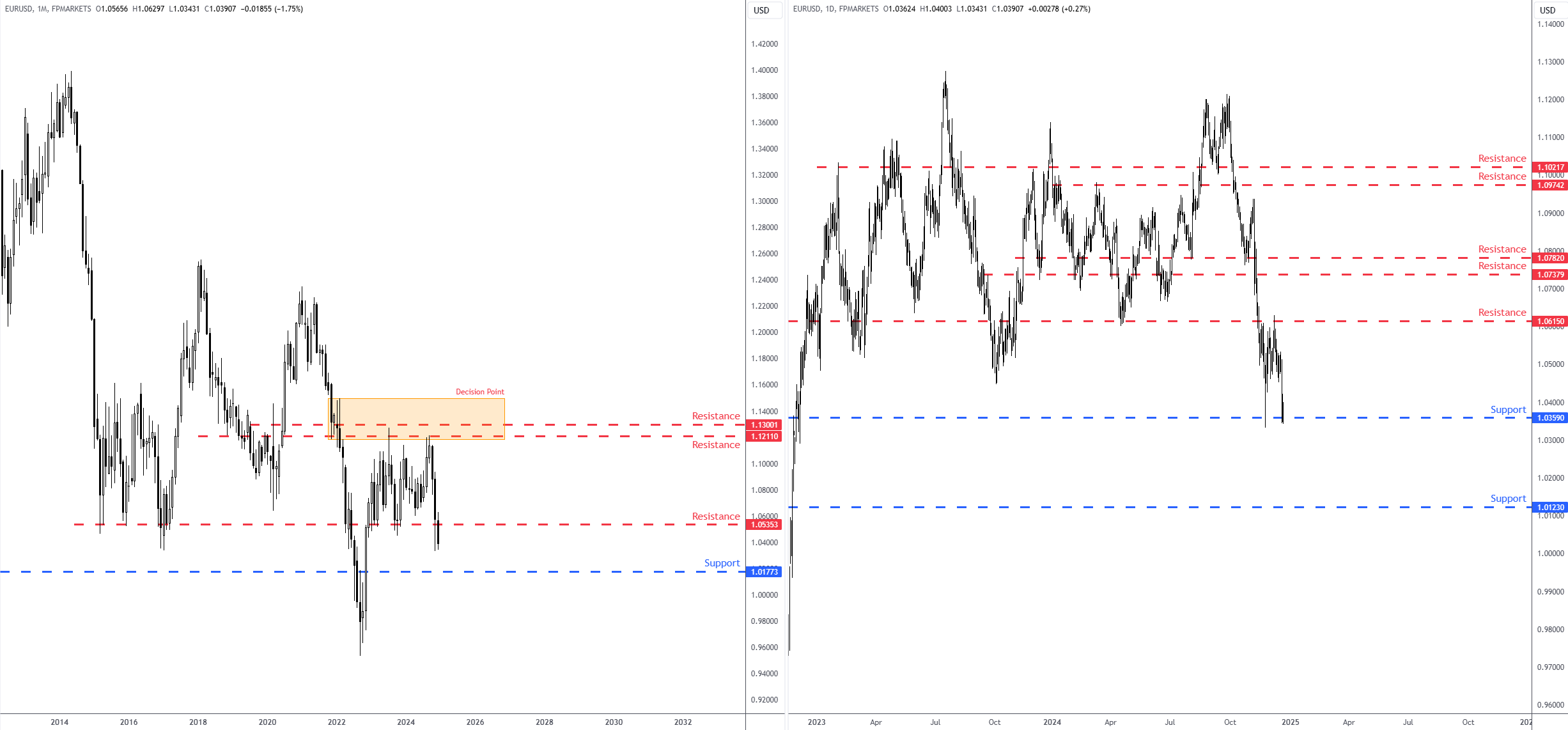

From the monthly chart of the EUR/USD (euro versus the USD), you will note that the currency pair is on track to notch up a third straight month of losses, down nearly 2.0% month to date. Technically, price recently rejected clear resistance between US$1.1300 and US$1.1211 (levels which happen to be encased within a decision point area at US$1.1497 and US$1.1186), and pushed through bids at support from US1.0535 to pave the way towards another possible support at US$1.0177.

On the daily chart, resistance was key in December at US$1.0615, with support entering the fight also making another show at US$1.0359. While I believe there is now a chance (given the lack of liquidity) that the pair will range between said resistance and support levels in early 2025, a breakout to the downside is likely on the table, in line with the downside bias since the double-top pattern formed around US$1.1195. The next downside target on the daily chart can be seen as far south as support, coming in at US$1.0123.

Chart created by TradingView

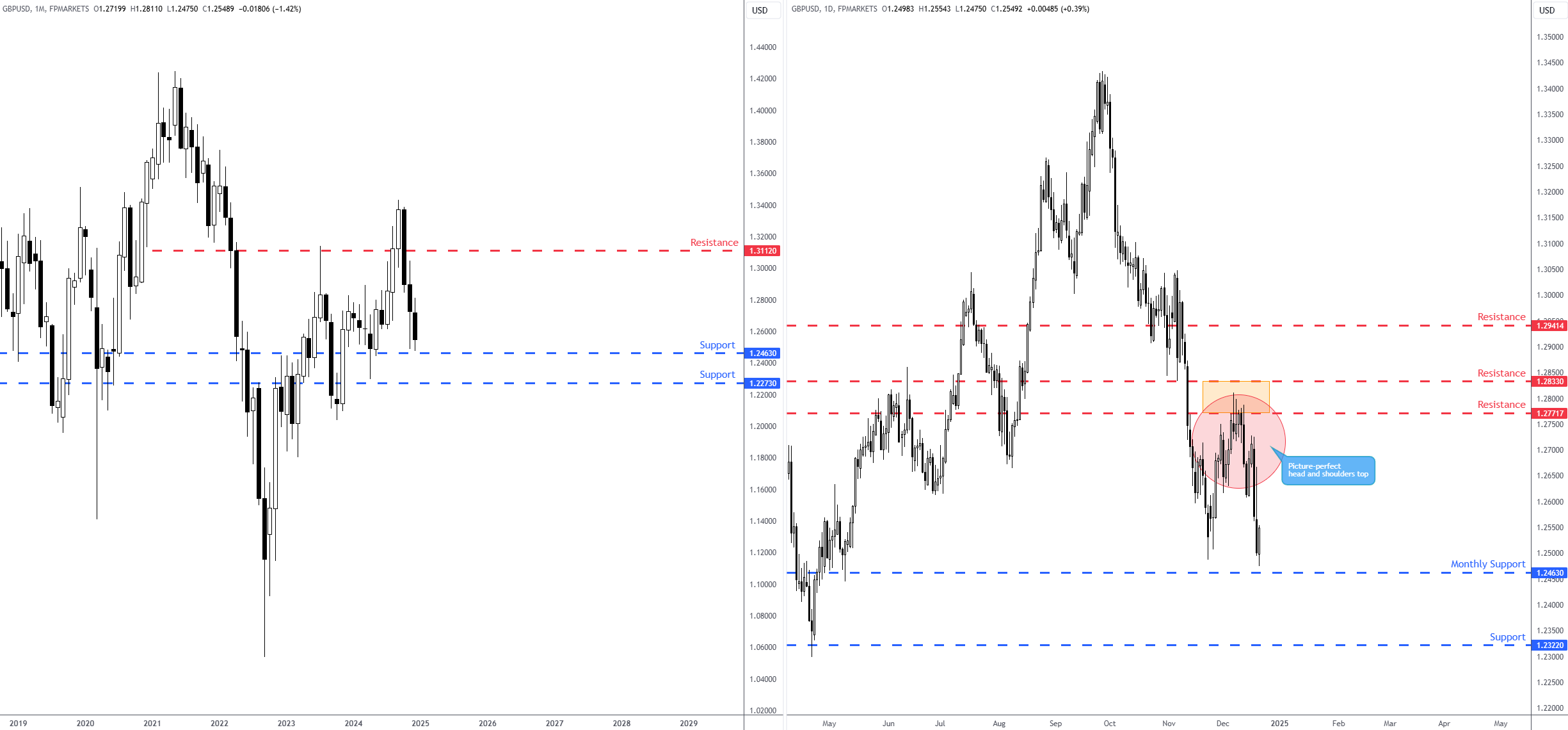

I expect the GBP to be more resilient than the euro versus the USD this year, based on elevated inflationary pressures and the BoE’s gradual approach to easing policy.

December is on track to end down 1.5% on the doorstep of monthly support from US$1.2463, marking a third consecutive month of downside for the GBP/USD currency pair. Overall, the trend is still favouring buyers in the long term, and therefore, the noted support (and possibly neighbouring support at US$1.2273) could be an area dip-buyers watch closely in early 2025.

On the daily timeframe, you will note the recent head and shoulders top completion from resistance between US$1.2833 and US$1.2772, landing the GBP/USD within a stone’s throw from the monthly support coming in at US$1.2463. For me, it is all about this monthly support level: a rejection of the base, along with some form of reversal signal on the daily timeframe, would be in line with the monthly chart’s uptrend. However, drawing beneath the monthly support would perhaps unearth a bearish scenario (in line with the bearish trend on the daily chart) towards daily support from US$1.2322, closely followed by monthly support mentioned above at US$1.2273.

Chart created by TradingView

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,