I filled up my tank last weekend before heading off on a road trip. When the gauge stopped at $35, I thought the pump had malfunctioned. Normally, it ends with the message, “please take out home equity loan” or “first-born required to work our car wash for six weeks.”

I was pleased to learn that the tally was not a mistake. Gas prices have fallen to a point where extraordinary financial strategies are no longer needed to support ground travel. The questions are: how long will this beneficence last? And looking beyond my own self-interest, is this a good thing for the world economy? The answers will depend on the actions of those on the other side of the energy equation.

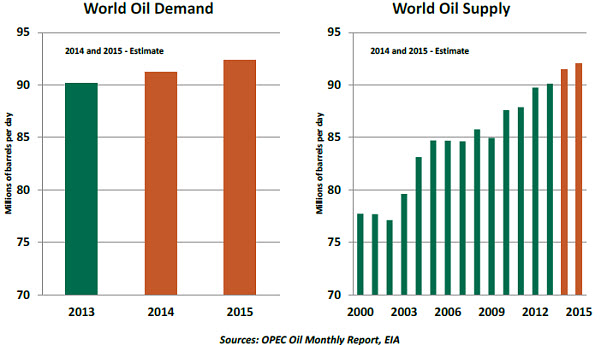

A complicated set of circumstances is responsible for the decline in oil prices, which fell below $80 per barrel this week. On one side of the market, very sluggish growth in the eurozone and moderation in the pace of Chinese manufacturing have diminished global demand. Estimates call for only very modest increases in oil consumption over the next two years.

On the supply side, the American energy resurgence leads the list of factors adding to output. Libya, which rid itself of Colonel Muammar Qaddafi three years ago, has placed its production back on line. The West has limited Iran’s sale of oil on world markets to force negotiations over its nuclear program. There has been some talk of relaxing these restrictions, which would bring several hundred thousand additional barrels to market every day.

A renewal of sectarian tension among Shias, Sunnis, Kurds and others has made it extremely difficult for the Organization for Petroleum Exporting Countries (OPEC) to restrict output. Regimes need to curry favor by providing benefits to their people, and the progress of the Islamic State (ISIS) has raised the need for defense spending.

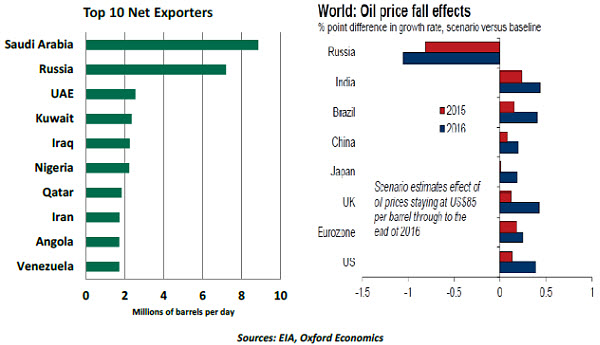

Saudi Arabia has traditionally served as the main enforcer within OPEC. It controls a third of the world’s reserves, and its share is among the highest quality. Saudi Arabia’s extraction costs are very modest. In the past, the Saudis have put pressure on others in the cartel by increasing output, driving prices down and thereby diminishing the profits derived from exceeding targets. The resulting financial pain leads miscreants to fall back into line.

Saudi Arabia has been especially displeased with Russia and Iran for supporting Syria and may seek retribution by using extraction as a weapon. Some also suspect that OPEC may be interested in taking some of the steam out of the American energy renaissance, which has reduced dependence on OPEC supply. But industry analysts suggest that most U.S. producers will remain profitable at $70 or $80 per barrel.  But there are two variables that Middle Eastern regimes focus on when it comes to energy prices. One is their extraction cost, which sets a breakeven point. But the other is the price required to generate sufficient revenue to ensure domestic tranquility and defend against outside insurgency. It is very difficult to mediate between the two.

But there are two variables that Middle Eastern regimes focus on when it comes to energy prices. One is their extraction cost, which sets a breakeven point. But the other is the price required to generate sufficient revenue to ensure domestic tranquility and defend against outside insurgency. It is very difficult to mediate between the two.

To date, it appears that Saudi Arabia has neither increased nor decreased its supplies to address price developments. There is a critical OPEC meeting late this month, at which time the group will attempt to reconcile its array of conflicting priorities.

The current situation is having an impact far from the Fertile Crescent. Producers in Latin America, where nationalized oil companies are common, rely substantially on energy exports to generate revenue. Venezuela, in particular, may face upheaval if crude prices remain low. Nigeria, battling its own insurgency and facing a potential credit rating downgrade, will also be challenged. Iran will face substantial budget shortfalls if oil prices fail to recover.

No one stands to lose more than the Russians if oil prices sustain their recent descent. Already in recession, the Russian economy could contract by a further 1% in each of the next two years. Pushed into an uncomfortable economic corner, President Vladimir Putin may respond with renewed aggression; reports of increased military activity in Ukraine this week were particularly discouraging.  On the happier side of the equation are countries reliant on energy imports. Leading this list are Japan and the eurozone, two markets whose economies have been struggling and which would welcome the relief that falling fuel prices would offer consumers. The offset is that inflation targets in both places will become more difficult to achieve.

On the happier side of the equation are countries reliant on energy imports. Leading this list are Japan and the eurozone, two markets whose economies have been struggling and which would welcome the relief that falling fuel prices would offer consumers. The offset is that inflation targets in both places will become more difficult to achieve.

The price of oil has historically been the source of significant economic realignment. That influence seems undiminished today, even though supply-and-demand patterns have changed dramatically over the past generation.

One thing that has not changed is that the Middle East holds the key to market developments. The politics and economics of the Fertile Crescent have been complicated for millennia. The presence of vast crude reserves in the region and the associated attention from Western powers have only served to make things even more difficult to diagnose.

Watching upcoming developments will be critical. And we’ll need to think beyond our own fuel tanks to fully appreciate their consequences.

Pressure for Economic Adjustment Mounts in Brazil

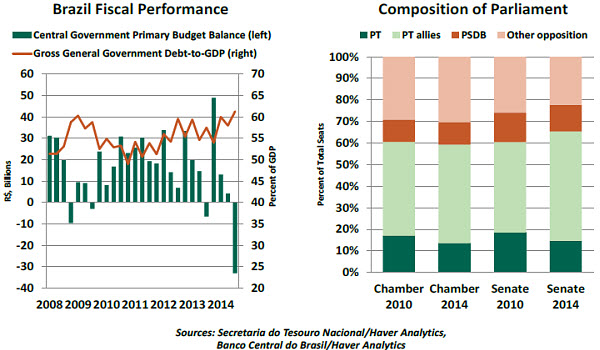

Brazil finds itself fresh off the most hotly contested election in its modern history. It saw two separate challengers nearly unseat incumbent President Dilma Rousseff and end the 12-year rule of the left-leaning Worker’s Party (PT). Finding order and progress is now the challenge facing the country.

Rousseff’s 51.6% to 48.4% margin victory is the narrowest in Brazil’s modern history. That her fragmented opposition rallied around Aecio Neves, whose privileged background turns off many voters, underscores the fact that Rousseff has much work to do as she prepares to begin her second term.

Brazil’s real gross domestic product (GDP) grew by 7.6% when Rousseff was elected in 2010; now, the economy is in recession. Under her mentor and predecessor Luis Inácio Lula da Silva, tight monetary policy kept inflation in check while strict adherence to budget targets instilled confidence in investors. Under Rousseff, expansive government spending has led to wider deficits and higher inflation. Increased intervention into the economy has damaged her reputation with investors.

Change is needed, and even the president’s allies are starting to acknowledge it. Culture Minister Marta Suplicy of the PT’s more-conservative wing captured the nation’s sentiment in her resignation letter to Rousseff earlier this week ahead of an expected cabinet shuffle:

“What all we Brazilians want now is that you should be enlightened in the choice of your new team, beginning with an experienced, independent and proven economics team, able to rescue confidence and credibility in your government and that, above all, will be committed to a new agenda of stability and growth for our country. This is what Brazil, today, anxiously awaits and hopes for.”

Since her victory, Rousseff has sent mixed signals. In her acceptance speech, she promised more dialogue and consensus with her opposition but failed to even mention her opponent Neves. Last week, she vowed to control inflation and trim public spending. Yet this week, Rousseff asked Congress to deduct all investments and tax exemptions from the key 2014 primary budget target (the balance of revenues and expenditures before debt payments), effectively lowering a goal that will be missed for the third straight year.

Yet there are some signs of hope. Last week, the government allowed state-owned oil giant Petrobras to raise its subsidized prices for gasoline and diesel fuel by 3% and 5%, respectively. Previously, the company was forced to sell at a loss as the government fought to keep inflation down ahead of elections.

Yet there are some signs of hope. Last week, the government allowed state-owned oil giant Petrobras to raise its subsidized prices for gasoline and diesel fuel by 3% and 5%, respectively. Previously, the company was forced to sell at a loss as the government fought to keep inflation down ahead of elections.

Rousseff will need to do more to rebuild her credibility. Her biggest opportunity to do so will be in appointing a credible replacement for current Finance Minister Guido Mantega, who will leave the government before Rousseff’s next term begins on January 1.

The president’s relationship with Parliament will also determine her success (or failure). The Senate and House (Chamber) are highly fragmented, with 28 separate parties represented. Rousseff’s party holds just 15% and 14% of seats in the respective legislatures, making her highly dependent on cooperation from her allies.

If the government fails to heed the growing number of voices around her for change, Brazil risks losing its investment-grade ratings and stumbling through another four years of economic malaise. With the Olympics on the horizon in 2016, nothing short of a medal-winning performance will do.

Fed’s Inflation Target: Ceiling or Average?

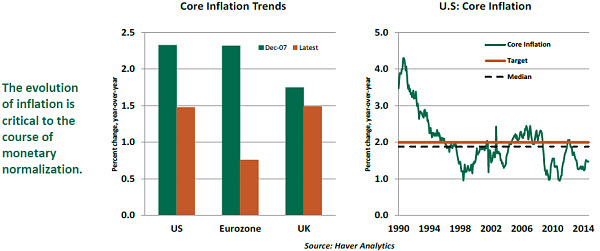

Inflation-targeting as a technique to manage inflation was introduced 25 years ago by the central bank of New Zealand. The Federal Reserve joined this club only in January 2012, when it announced a 2.0% goal for inflation. This framework is three years old, but its interpretation is still a subject of debate whose conclusion will have a critical influence on the path of U.S. interest rates.

Several advanced countries face a low-inflation environment today and stand well below their targets, despite substantial amounts of monetary stimulus. In the United States, the Fed’s preferred inflation measure has fallen short of the target for most of the last four years.

Low inflation keeps real wages high and discourages firms from increasing their payrolls. Therefore, there is concern that if inflation is held to 2.0%, policy may not produce the desired outcome for the labor markets. Short-term rates are at their zero lower bound, so slightly higher inflation would have the effect of easing monetary policy.

It is with this is in mind that President Charles Evans of the Federal Reserve Bank of Chicago has expressed willingness to tolerate inflation above 2.0%, but with a 2.5% cap, until it is certain that raising interest rates would not damage the expansion. Noting that inflation has been allowed to undershoot its target for so long, Evans has suggested that a brief period above the target should not be viewed as a significant violation.

Evans has also observed that a short period of overshooting the current target would be less costly than acting prematurely. There is a confidence in his views that inflation can be dealt with as it arises, as opposed to pre-emptively. President Dennis Lockhart of the Atlanta Fed and President John Williams of the San Francisco Fed largely share this view. It is worthwhile to note that these three Fed officials will be voting members of the Federal Open Market Committee in 2015.

Inflation goals have already moved from ceilings to targets, to reach from either direction. At present, some want to take things further and consider them as averages to achieve over some length of time. Should this view prevail, we’ll have lower for quite a bit longer.

Recommended Content

Editors’ Picks

EUR/USD stabilizes above 1.1350 on Easter Friday

EUR/USD enters a consolidation phase above 1.1350 on Friday as the trading action remains subdued, with major markets remaining closed in observance of the Easter Holiday. On Thursday, the European Central Bank (ECB) announced it cut key rates by 25 bps, as expected.

GBP/USD fluctuates below 1.3300, looks to post weekly gains

After setting a new multi-month high near 1.3300 earlier in the week, GBP/USD trades in a narrow band at around 1.32700 on Friday and remains on track to end the week in positive territory. Markets turn quiet on Friday as trading conditions thin out on Easter Holiday.

Gold ends week with impressive gains above $3,300

Gold retreated slightly from the all-time high it touched at $3,357 early Thursday but still gained more than 2% for the week after settling at $3,327. The uncertainty surrounding US-China trade relations caused markets to adopt a cautious stance, boosting safe-haven demand for Gold.

How SEC-Ripple case and ETF prospects could shape XRP’s future

Ripple consolidated above the pivotal $2.00 level while trading at $2.05 at the time of writing on Friday, reflecting neutral sentiment across the crypto market.

Future-proofing portfolios: A playbook for tariff and recession risks

It does seem like we will be talking tariffs for a while. And if tariffs stay — in some shape or form — even after negotiations, we’ll likely be talking about recession too. Higher input costs, persistent inflation, and tighter monetary policy are already weighing on global growth.

The Best brokers to trade EUR/USD

SPONSORED Discover the top brokers for trading EUR/USD in 2025. Our list features brokers with competitive spreads, fast execution, and powerful platforms. Whether you're a beginner or an expert, find the right partner to navigate the dynamic Forex market.