![]() Northern Trust Economic Research Department

Northern Trust Economic Research Department

Northern Trust

Both my parents lived through the Great Depression. Their families were devastated; small businesses that had taken years to establish failed almost overnight. Long periods of unemployment followed, and living conditions deteriorated. It took a lot of time and a lot of industry to regain even a modicum of sufficiency.

The progeny of that generation were raised with a very simple attitude toward work: find a job, and then do whatever it takes to keep the job for as long as possible. Do what the boss tells you, no matter how menial. Personal or professional fulfillment through work was not part of the equation; the ideal was a long tenure with a single company, a steady income and a pension.

That sort of an experience is a rarity today. Employment over a working lifetime is now considerably more varied and itinerant. The latest expression of this is the rise of “gigs,” ad hoc job assignments that are arranged over the internet. Some have suggested that the “gig economy” is an innovation representing an inflection point in the evolution of world labor markets.

But gigs are not new, and they are following a trend, not blazing a new one. The relationship between firms and workers has been evolving to a more-transient arrangement for at least a generation, and gigs are merely the latest chapter in this long-running story. Flexible work systems can have benefits for both sides, but they can also raise challenging questions about the aims of employment.

A term once confined to entertainment bookings, gigs now cover a wide range of economic activity. The transit company Uber is the most prominent example, but similar platforms facilitate work arrangements across a variety of industries. Renting through AirBnB, selling wares on eBay or finding handy work through TaskRabbit is becoming much more common.

The “gig economy” is terribly difficult to measure. Claims about its size vary widely; the consensus is that employment of this kind remains very modest, but it appears to be growing rapidly. One estimate suggests that there are 2.5 million workers in the United States who are part of the sharing labor force. Very few earn all their income through this channel; most take on gigs to supplement something more permanent.

There are certainly reasons to be excited about online marketplaces for talent. Anything that better matches supply and demand in the labor market should reduce search times and the duration of unemployment. Work need not be bought and sold in standard 40-hour blocks, but rather can be solicited and offered in much more-granular ways. The added flexibility can be very attractive to both providers and users of labor.

There are certainly reasons to be excited about online marketplaces for talent. Anything that better matches supply and demand in the labor market should reduce search times and the duration of unemployment. Work need not be bought and sold in standard 40-hour blocks, but rather can be solicited and offered in much more-granular ways. The added flexibility can be very attractive to both providers and users of labor.

While some gigs focus on local markets (babysitting or grocery shopping), others open global opportunities (code writing, data analysis). In a study released last year, the McKinsey Global Institute suggested that the benefits of digital platforms for labor could produce a substantial increase in global output.

The newness of the gig economy, the sophistication of the websites supporting it, and the apparent popularity of the system among young people have made the gig economy a media darling. Millennials, with their desire for a portfolio of experiences and a high degree of work-life balance, would seem a perfect fit for the new model.

But the gig economy is far from novel. For many years, across many industries, firms have been converting permanent positions to contract arrangements. Security, information technology, and maintenance professionals who used to be on the main payroll are now sourced from firms that specialize in each area. Whereas the number of W-2 wage forms issued in the United States has stagnated, the number of 1099 forms (which capture income from contract arrangements) has risen.

Interestingly, though, the fraction of workers who identify themselves as self-employed has not changed all that much over the last 40 years, and if anything, has declined. This would seem consistent with the notion that gigs are a supplement to, not a replacement for, traditional working models.

To its admirers, the “gig economy” is a welcome innovation in the way work is organized. But to detractors, gigs are simply a fancy example of the long-running deterioration in worker security. Gigs and other piecework arrangements don’t come with health benefits, disability insurance, minimum wages or paid time off. (In fact, companies like Uber suggest that they are not employers, but merely a medium through which supply and demand for services meet.)

To its admirers, the “gig economy” is a welcome innovation in the way work is organized. But to detractors, gigs are simply a fancy example of the long-running deterioration in worker security. Gigs and other piecework arrangements don’t come with health benefits, disability insurance, minimum wages or paid time off. (In fact, companies like Uber suggest that they are not employers, but merely a medium through which supply and demand for services meet.)

It is much more difficult for workers not on permanent payrolls to qualify for credit or to become involved in a retirement savings program. Gig workers would be the first to feel the impact of economic slowing, with no access to unemployment benefits.

A paper released last month estimated that the percentage of American workers in “alternative” arrangements is now nearly 16%, up from 10% a decade ago. Gigs are just the leading edge of a much broader movement that challenges traditional perceptions of what work is and how it is organized.

There are certainly those who suggest that alternative work arrangements are liberating for many in the labor force. But there are others who see risks in too much freedom. Forty years’ tenure and a gold watch at retirement may no longer be attainable, but some level of employment security might be nice.

Nothing Sweet about Fudging Economic Data

Economic measurement is an inexact science. Even the best-constructed series are only simplified approximations of real-world activity. However, institutions all too often have been guilty of intentionally “cooking the books” for self-serving purposes. Officials in Argentina and Greece are two of the most egregious perpetrators in recent history.

Argentina’s problems began in 2006, when inflation began to rise during Cristina Fernández de Kirchner’s presidential campaign to succeed her husband. INDEC, the national statistics institute responsible for publishing the headline consumer price index, began receiving pressure to give up the names of companies surveyed and to manipulate the data. When INDEC economists refused, they were fired, and soon inflation figures began to improve.

Fernández won the election and for the following eight years, official inflation hovered around 10%, while calculations by private economists were more than double (earning them fines). The International Monetary Fund ultimately censured Argentina over its lack of progress in correcting the underreported inflation – the only country to ever receive such a rebuke. The publication of inflation figures has remained suspended since November 2015, and the administration of newly elected President Mauricio Macri has vowed to develop a more accurate price index by July 2016.

Greece’s manipulation of its fiscal results is another example. The Greek government recorded very high budget deficits, sometimes in excess of 10% of gross domestic product (GDP), until 1994. Greece sought membership in the euro area in the late ‘90s, and it submitted significantly altered numbers to the European Union were significantly altered to reach the 3% of GDP deficit needed to meet the Maastricht requirements. Greece was accepted as the 12th member of the euro area in 2000. A 2004 audit of Greek government finances revealed that the country indeed had not met the 3% deficit criteria at the time of admission to the euro area. In 2010, the European Commission again condemned Greece for falsifying its public finances and obstructing the collection of accurate statistics during 2008-09. The revelation angered the other euro area partners and led to debt downgrades and higher funding costs for the sovereign.

Argentina and Greece are not alone. China’s GDP and other economic data have long been suspected of being massaged to bolster party credibility and preserve social stability. Brazilian President Dilma Rousseff is currently embroiled in impeachment over allegations of manipulating fiscal data. In general, political opportunism precipitates data manipulation. However, politicians are more likely to persist in publishing fraudulent numbers when institutions are weak and power is concentrated in the hands of few.

As the world grows richer in information and more sophisticated in ways to analyze data, governments will have a harder time getting away with economic fraud. One fascinating example is the use of Benford’s Law. In his 1938 paper, American physicist Frank Benford observed a natural pattern among large sets of financial and economic data. Counterintuitively, numbers found in these types of data series naturally have a leading digit of “1” (as in the number 1,699) more often than “2” and far more often than “9”. This “natural” distribution is known as Benford’s Law.

Analysts can thus compare economic data series against Benford’s distribution to detect manipulation. Sure enough, a 2011 study published in the German Economic Review found that budgetary data reported by Greece showed the greatest deviation from Benford’s law among all euro states, particularly during 1999-2000 and 2008-09. The technique can also help flag price collusion in markets, like in the case of LIBOR-fixing scandals.

We certainly hope that economists and politicians take heed. Economic honesty truly is the best policy.

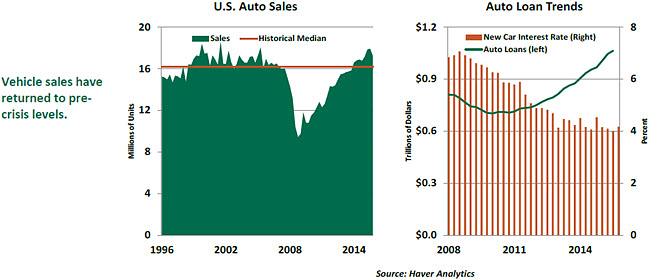

Auto Sales Should Hover Around Speed Limit

Auto sales move consumer spending trends in the United States, and by implication affect the economy’s overall performance. Recent auto sales data contain distinct swings that raise questions about the near-term outlook.

Cars sold at a 17.33 million pace in 2015, which nearly matches the 17.35 million high set in 2000. Purchases of autos fell to 16.5 million units in March, after a 17.4 million average in January and February. Seasonal factors partly influenced the March reading.

The U.S. labor market is in a favorable spot, which should continue to support auto purchases. Looking ahead, the current low auto loan rates will advance and trim purchases as the Fed tightens monetary policy.

The value of the dollar, gasoline prices, and consumer lending standards are other factors that drive auto sales. Further dollar weakening could change the composition of auto sales. The supply-demand situation of crude oil points to only a modest increase in gasoline prices in the months ahead. As a result, sales of larger vehicles are expected to continue at a higher share of overall purchases.

The Federal Reserve’s Senior Loan Officer Survey suggests that lending standards for autos are not problematic. Auto loans outstanding have risen roughly 45% during the nearly six years of expansion, reaching $1 trillion. About 2.6% of outstanding auto loans were delinquent at the end of 2015, up from a low of 1.9% in 2012. Concern exists about auto loans to less-creditworthy borrowers, but data indicate that these loans appear to have peaked in late-2015. With used car prices robust, the risk of widespread losses from auto loan defaults seems modest.

Pent-up demand fueled a part of auto sales in the current expansion. The recent auto sales trend exceeds the historical median, which suggests that demand for cars is likely to settle at a lower but still-elevated level.

The information herein is based on sources which The Northern Trust Company believes to be reliable, but we cannot warrant its accuracy or completeness. Such information is subject to change and is not intended to influence your investment decisions.

Recommended Content

Editors’ Picks

Australian Dollar extends losses as US Dollar improves due to increased risk aversion

The Australian Dollar depreciates for the fifth consecutive session on Friday. China's Third Plenum concluded on Thursday without concrete measures to revitalize the faltering economy. The US Dollar may struggle as soft labor data strengthens expectations of a Fed rate cut in September.

EUR/USD: US Dollar can turn bullish on upbeat growth and inflation data

The EUR/USD pair halted its latest run and is closing the last week unchanged, just below the 1.0900 mark. However, it reached a fresh multi-month high of 1.0947 mid-week, only turning south after the European Central Bank uneventful monetary policy announcement.

Gold: Buyers refrain from betting on further upside after record-setting rally

Gold retreated sharply after touching a new record-high last week. PCE inflation and GDP data from the US will be watched closely by market participants. The near-term technical outlook highlights a loss of bullish momentum.

ALT, WLD, ENA, ID set for $200 million token unlocks next week

The crypto market is set to experience another wave of token unlocks next week, with Altlayer, Worldcoin, Ethena, and Space ID set for a combined token unlock worth about $200 million.

US President Joe Biden stands down from reelection, endorses Kamala Harris

Following a long week of political turmoil, United States President Joe Biden announced on Sunday that he will end his reelection bid and will speak to the nation later this week in more detail about his decision.