Options – Anchors and Offsets Part 2

|A couple of weeks ago, I began discussing the idea of Anchors and Offsets in option trading. We’ll continue with that today.

While the simplest use of options is just as lower-cost substitutes for stock, this only scratches the surface of what they can do. We can certainly buy Call options in place of buying a stock, or buy Put options in place of selling a stock short. But to get the real power of options, we need to combine them.

For example, on June 10-12 the SPY, a main bellwether for the global equity market, reacted to geopolitical concerns and disappointing data by dropping by about three points, or 1.5%. The chart is shown below:

{kind=link}

Let’s say we were still bullish on the equity market, and thought that this pullback was probably over. Moreover, we would be happy to own SPY if it dropped a little further into our demand zone from roughly $192-193.

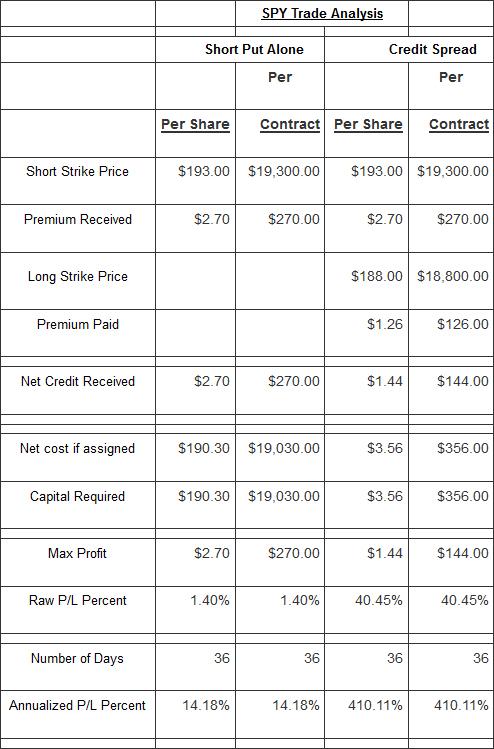

One possible move would be to sell the July $193 puts. These could be sold at the time for $2.70 per share ($270 per 100-share contract). We would receive the $270 right away. If SPY remained above $193, the options would expire and that $270 would be clear profit.

If SPY dropped below $193, and remained there at the expiration of the July options on July 18, then we would be obligated to buy the SPY stock at $193 per share ($19,300 for the 100 shares covered by the single put contract). Our net cost would be the $193 strike price, less the $2.70 we had received for selling the puts, or $190.30 per share. Let’s say we thought it very unlikely that SPY would be below $190.30, so we considered this a risk worth taking.

Let’s look at the stats on this trade:

{kind=link}

If we were right about SPY rallying from here, this trade would pay off at the rate of 14% (annualized). If SPY did not rally, at worst we would own the ETF at $190.30, a price we were happy with.

Fine. But could we improve on this? What were the undesirable characteristics of this position?

Here are three:

Unlimited risk. If SPY did drop below $190.30, we would have a loss, and that loss would be unlimited. Well, it would not exactly be unlimited. At most, if the value of SPY dropped to zero (an impossibility), we would lose $19,030. But this is close enough to infinity compared to our $270 maximum profit, that for practical purposes, our loss was unlimited. By convention, naked short put trades are referred to as having unlimited risk. We could mitigate this by planning to exit the trade (buy back the short puts) if SPY dropped below a certain level. But this would expose us to:

Extreme exposure to changes in Implied Volatility (IV). IV is the measure of how much people are willing to pay for time value. The Implied Volatility of SPY at the time was smack in the middle of its most recent 52-week range. IV could just as easily go up or down. If the price of SPY went down, the price of time value in its options (IV) would probably go up. If that happened, then our puts would become even more expensive, increasing our loss.

High capital requirement. In order to insure that we would have the money to buy the SPY if the puts were assigned, our broker would require that we earmark funds for that purpose. We would need to have $19,300 in cash in our account in order to sell that put for $270. (This would be a cash-secured put. Some people are able to sell puts naked, by putting up about 20% of this amount. If so, then they will get margin calls to put up more cash if the stock falls. We assume here that we are doing this trade on a fully cash-secured basis, No margin calls are possible, and the cash-secured short put can be done inside an IRA account.)

How could we reduce or eliminate these undesirable effects?

By turning the short put position into a credit spread position. We could do this by simultaneously purchasing another put at the $188 strike. These could be bought for $1.26 per share ($126 per contract). With the short $193 put as the anchor of our position, the long $188 put would be our offset unit. Here is how that would change things:

Unlimited risk. Not any more. Now our $188 put would protect us in the event of a very large drop. At worst, we might have to pay $5 per share (the difference between the $188 and $193 strikes) to get out of the position, no matter how far SPY dropped.

Extreme exposure to changes in Implied Volatility (IV). Much improved. Since we now owned the $188 put, if SPY’s IV went up, our long put would go up in value too. This would offset most of the damage from an IV increase.

High capital requirement. Hugely reduced. Since our maximum exposure was now $5 instead of $190, we would only be required to put up $5 per share. And that would be reduced by the $144 net credit generated (the $2.70 premium received for the short put, less the $1.26 paid for the long put). The net out of pocket would be just $3.56 per share, compared to $190.30. This would increase our cash-on-cash profit percentage immensely.

Here’s the comparison of the original short put position and the credit spread:

{kind=link}

In this trade, adding an offset to the anchor unit, transformed the trade from one with unlimited risk into a limited risk trade. At the same time, the profit percentage was improved a very great deal.

I hope this piques your interest in options, especially the power available by combining them. This is only one small example. There are many ways to construct very exciting positions. We’ll look at more in the future.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.