Assessing the potential damage to the UK economy from Brexit is speculation. There are no guidelines. No one has ever tried to rewrite the rules of economic and political interaction for two modern industrial economies at one fell swoop.

The EU and the UK are attempting to codify in a few months a relationship that has evolved over 40 years with the Union and over hundreds of years between the UK and individual nations on the continent. There will necessarily be mistakes, omissions and bad decisions.

There are however several factors that, when considered dispassionately, render the judgment far more positive than is generally realized.

The most telling is the simple fact that the EU and the UK must remain each other’s main economic partners. The companies and individuals that have traded and travelled across the narrow seas will continue their relationships. A change in rules will not end affinities. England will still buy her wine on the continent and London will still be the largest financial and trading center in Europe.

These economic imperatives will drive businesses and governments on both sides of the new regulations to seek efficiencies similar to the ones enjoyed now. All the pressures exerted by companies and individuals in the UK and the EU on regulators will be to make the new rules accommodate existing business relations.

It will be in both side’s interest to have the regulations evolve quickly into standardized practice. The customs and financial bureaucracies that administer the current rules will enforce the new system. If customs services are not the popular image of reliable execution they are least experienced and familiar with the idea of trade facilitation.

With the EU and UK governments very aware of the electoral dangers of a botched separation supervision of the initial implementation should be strict and careful cooperation will be encouraged. Such attention will not eliminate problems but as neither Paris nor London wants pictures of endless truck lines and customs queues and reports of unavailable medicine, the press for performance on the bureaucracies will be high.

A second indicator that Brexit may be less troublesome is that the many predictions of the dire effects of Brexit have had little impact on the economic performance of the UK.

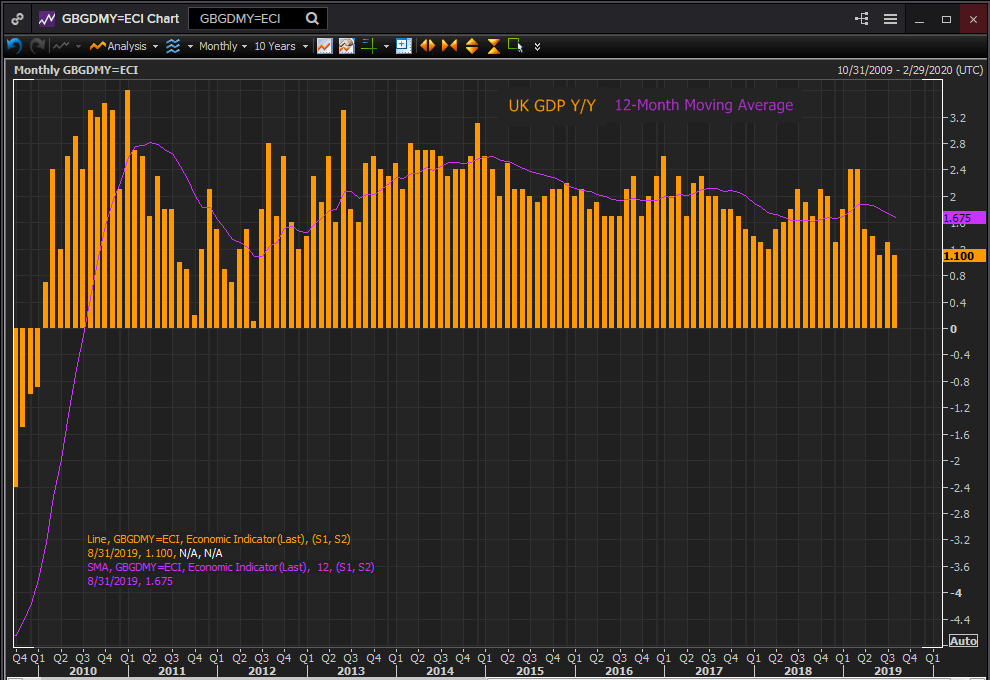

In the three years since the Brexit vote the British economy has held up remarkably well. Annual growth has declined from 1.958% in June 2016 to 1.625% in August 2019. That compares favorably with German GDP which has dropped from 1.8% in the second quarter of 2016 to 0.4% in the second quarter of this year.

Reuters

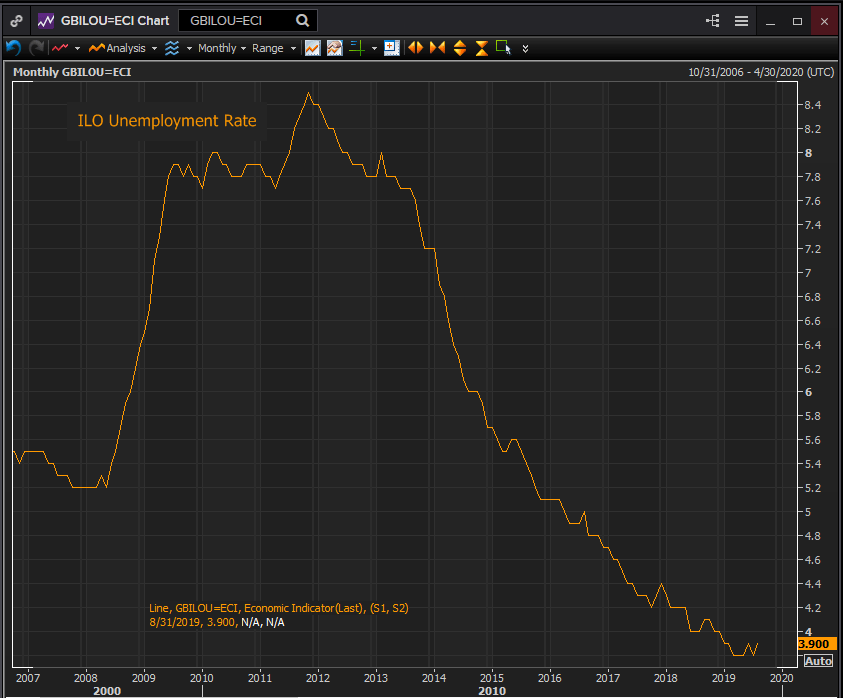

British unemployment has fallen from 4.9% in the month of the Brexit vote to 3.9% in August. Average annual earnings without bonus have increased from 2.6% in June 2016 to 3.8% in August. Retail sales have be stable across the period. The 3-month moving average was 0.25% in June 2016 and the same last month.

Reuters

Consumer impact has been limited to confidence. The GfK consumer sentiment index 3-month moving average has skidded from -1.667 in June 2016 to -12.333 in September 2019 with the lowest levels coming this year.

The largest effects have been in in the industrial sector where the 3-month moving average for production has slipped from 0.033 at the June vote to -0.133 in August 2019.

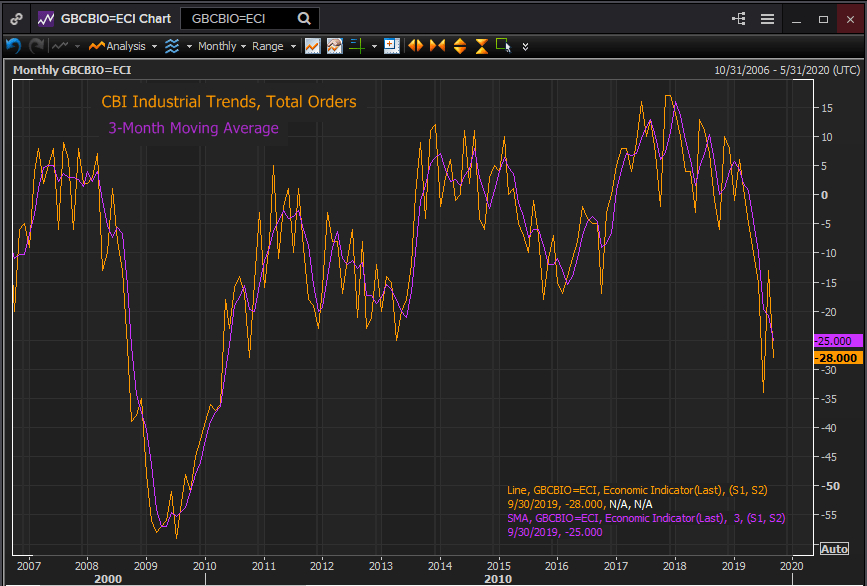

Industry trends have also been stricken. The Confederation of British Industry total orders index has collapsed from -7 in June 2016 to -25 in August. The Distributive Trades Volume of Sales index has gone from -0.667 that June to -27 in September of this year. For both of these gauges the steepest declines have come in the past year.

Reuters

While the activity of the British economy over the past three years hardly guarantees an uneventful exit it does show a degree of ease with the process, even if the industrial sector is showing signs of deeper concerns.

It is no doubt true that British industry as a whole would prefer to stay within the EU, but that does not mean it contemplates departure in the same apocalyptic tones as much of the press. The most likely response of many executives is probably the pragmatic one, if it has to be let’s make it work.

There is another aspect to Brexit that has received almost no notice. The exit will create economic activity. All of the effort that will be needed to recast businesses and their supply and distribution chains into the new regulatory modes and the search for material and market replacements, domestically and internationally, will generate economic growth.

Finally, the third sign that Brexit may be a more moderate choice than imagined has been the reaction of the credit markets.

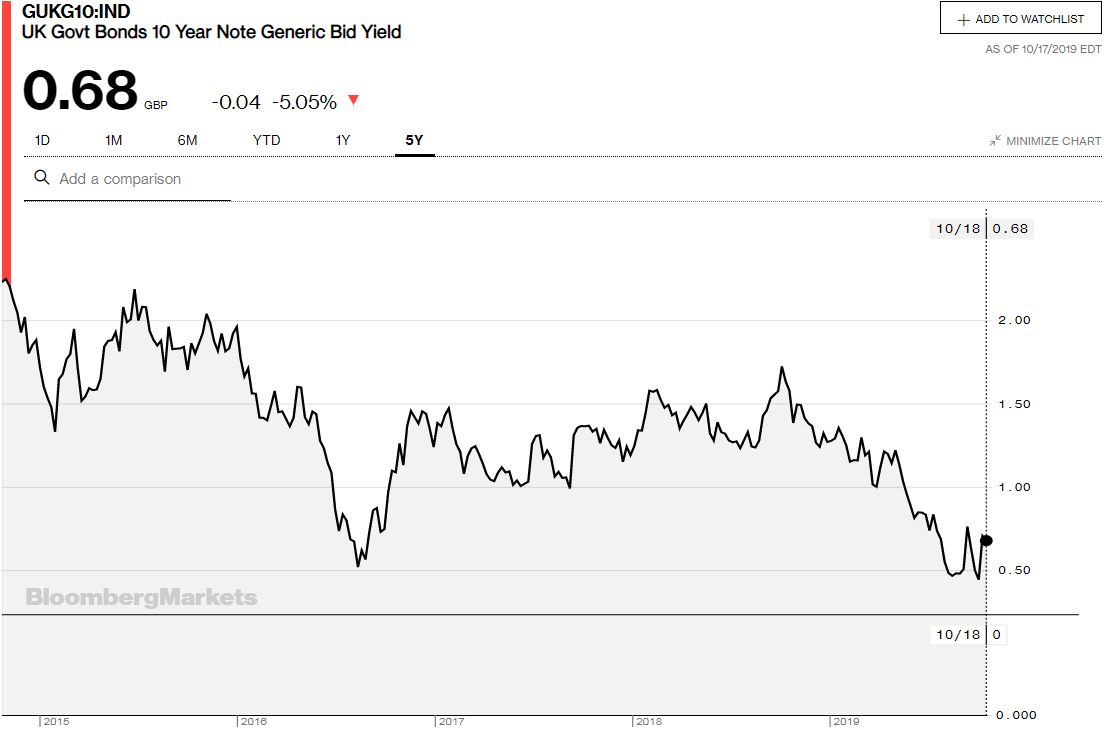

The yield on the 10-year generic Gilt was 1.09% on June 24, 2016. It is currently 0.68%, off 41 basis points. The German 10-year Bund has lost 41 points to -0.41% in the same time frame and the French equivalent has shed 50 points to -0.11%.

Over the three year period of Brexit the credit markets have not exacted any penalty for the pending exit of the UK. The disparity in yields largely reflects the past and current efforts by the ECB to support the monetary union economies with low rates enacted by bonds purchases.

It must be said that the equity markets have a different opinion. The 17% gain in the FTSE from the referendum is among the lowest in Europe. The German Dax and the French CAC rose 30% and 38% in the same period. The US S&P 500 is up 47% and the Dow has soared 55%.

The unique situation of the British exit from the European Union has generated different reactions in markets and constituencies.

The UK economy seems to be the least troubled in Europe with stronger growth, lower unemployment and better consumption figures than its major competitors on the continent. Credit markets appear unmoved demanding no premium from British debt. Equities are the most concerned shaving 10% and 18% from the FTSE return in comparison to the German and French gains over the time of Brexit.

Perhaps the most optimistic sign is necessity. The UK trade, financial and economic relationship with the continent is permanent. It is not too much to think that it will continue to benefit both parties.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

AUD/USD posts gain, yet dive below 0.6500 amid Aussie CPI, ahead of US GDP

The Aussie Dollar finished Wednesday’s session with decent gains of 0.15% against the US Dollar, yet it retreated from weekly highs of 0.6529, which it hit after a hotter-than-expected inflation report. As the Asian session begins, the AUD/USD trades around 0.6495.

USD/JPY finds its highest bids since 1990, approaches 156.00

USD/JPY broke into its highest chart territory since June of 1990 on Wednesday, peaking near 155.40 for the first time in 34 years as the Japanese Yen continues to tumble across the broad FX market.

Gold stays firm amid higher US yields as traders await US GDP data

Gold recovers from recent losses, buoyed by market interest despite a stronger US Dollar and higher US Treasury yields. De-escalation of Middle East tensions contributed to increased market stability, denting the appetite for Gold buying.

Ethereum suffers slight pullback, Hong Kong spot ETH ETFs to begin trading on April 30

Ethereum suffered a brief decline on Wednesday afternoon despite increased accumulation from whales. This follows Ethereum restaking protocol Renzo restaked ETH crashing from its 1:1 peg with ETH and increased activities surrounding spot Ethereum ETFs.

Dow Jones Industrial Average hesitates on Wednesday as markets wait for key US data

The DJIA stumbled on Wednesday, falling from recent highs near 38,550.00 as investors ease off of Tuesday’s risk appetite. The index recovered as US data continues to vex financial markets that remain overwhelmingly focused on rate cuts from the US Fed.